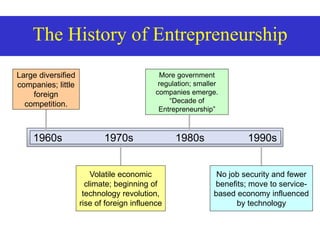

This document provides an overview of entrepreneurship and key related concepts. It discusses how entrepreneurs contribute to the economy by turning demand into supply, providing venture capital, jobs, and promoting societal changes. Entrepreneurship involves recognizing opportunities, testing them in the market, and gathering resources to start a business. The entrepreneurial start-up process has five components - the entrepreneur, opportunity, resources, organization, and management. Historical perspectives on entrepreneurship from the 1960s to 1990s are also presented.