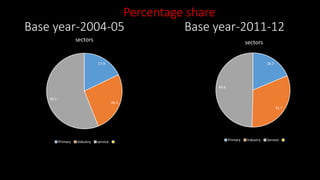

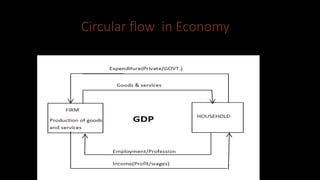

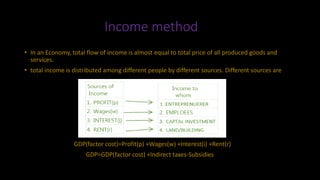

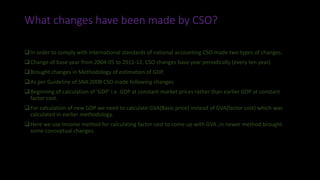

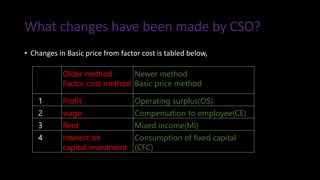

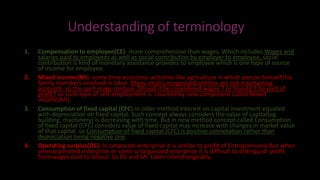

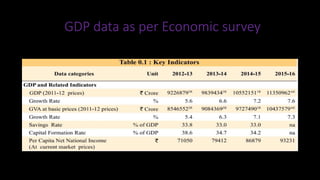

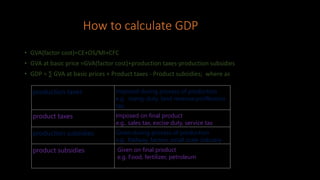

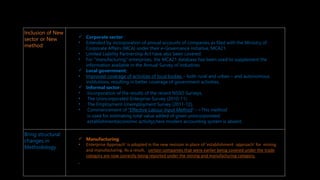

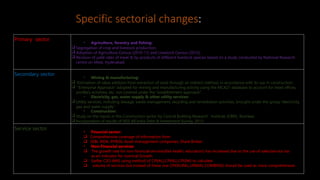

The document discusses changes in the methodology and calculation of Gross Domestic Product (GDP) in India, noting the shift from the base year 2004-05 to 2011-12. It highlights the three methods for calculating GDP: the income method, the expenditure method, and the production method, along with recent updates to comply with international accounting standards. It also describes changes in terminology and the incorporation of new sectors for better accuracy in GDP estimation.