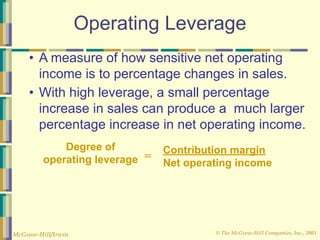

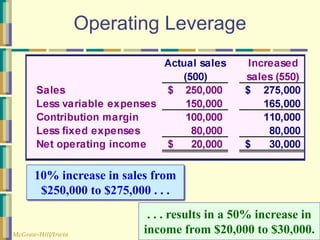

This document provides an overview of cost-volume-profit (CVP) analysis concepts including:

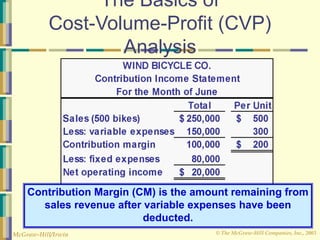

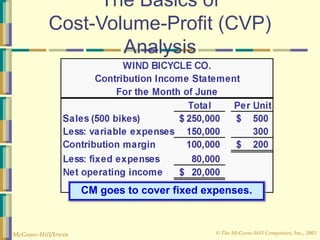

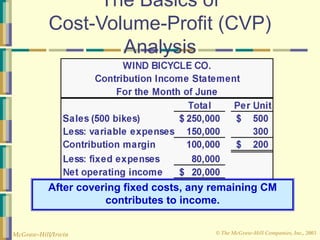

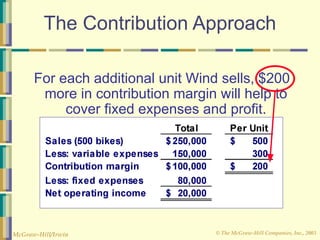

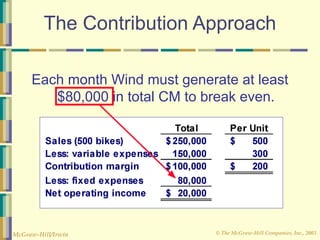

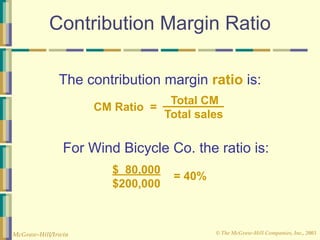

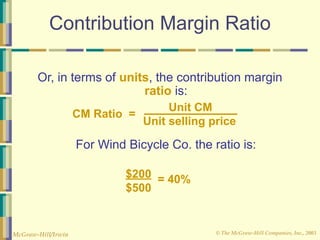

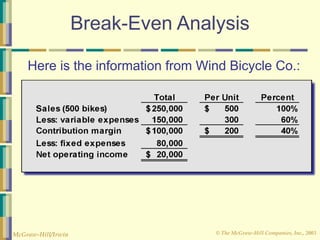

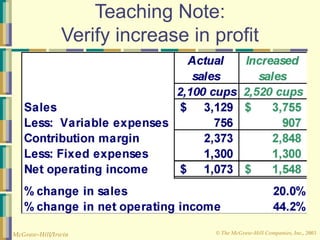

- Contribution margin is sales revenue minus variable expenses and goes towards covering fixed expenses.

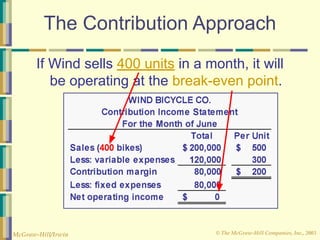

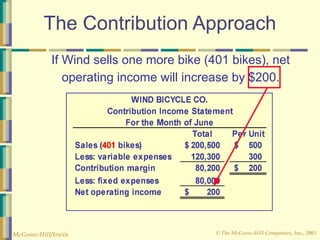

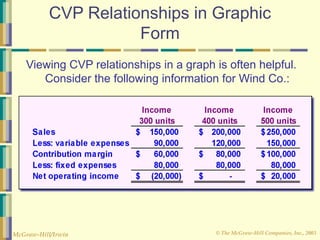

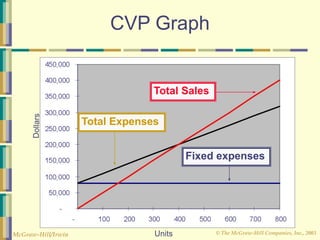

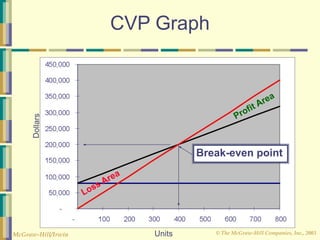

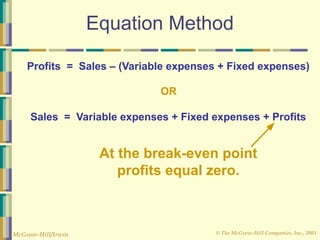

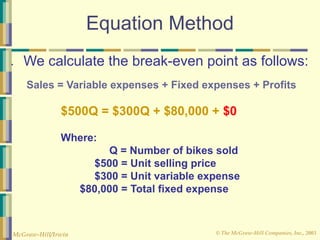

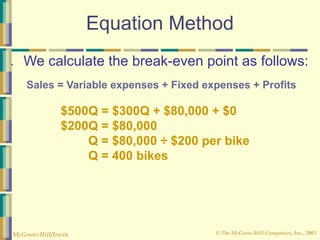

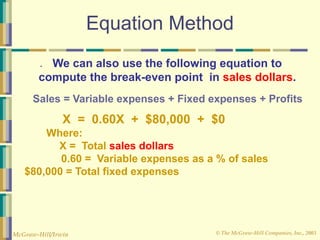

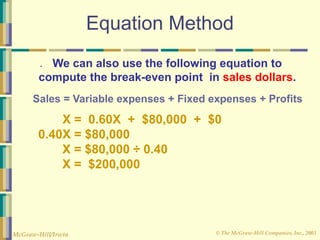

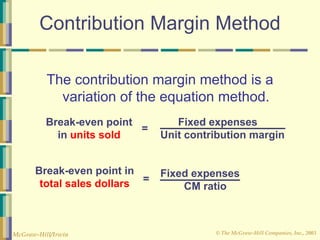

- Break-even analysis can be done graphically, using equations, or the contribution margin method to determine the sales volume needed for profits to equal zero.

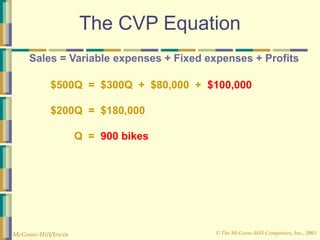

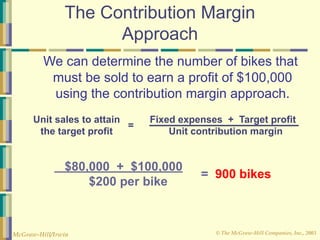

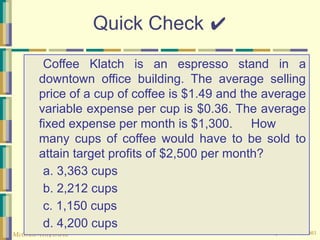

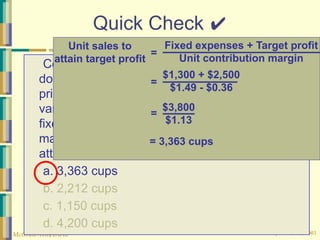

- Target profit analysis uses CVP equations or the contribution margin approach to determine the sales volume needed to achieve a desired profit level.

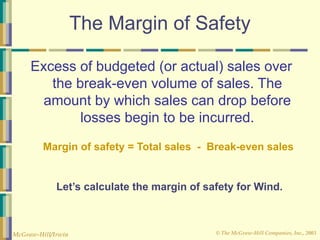

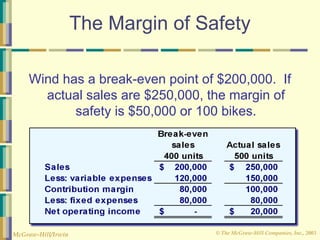

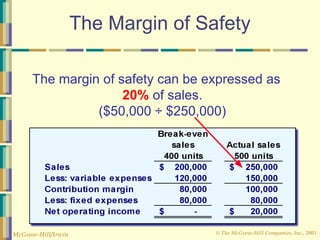

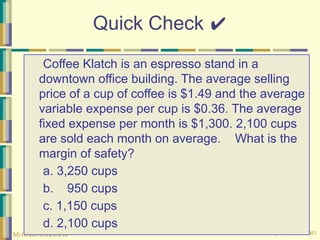

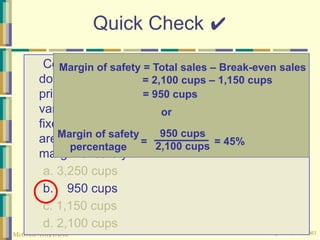

- Margin of safety is the excess of actual or budgeted sales over break-even sales, indicating how much sales can decrease before losses are incurred.