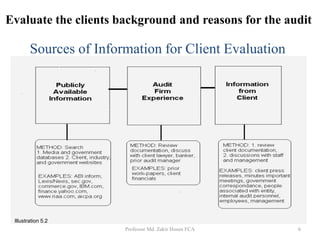

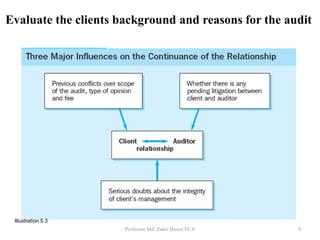

The document discusses the client acceptance phase of an audit engagement. It outlines the objectives of client acceptance as examining potential clients to determine if there are any reasons for rejection or if the client should be convinced to hire the auditor. It also discusses deciding whether to accept new or continuing clients. The procedures for client acceptance include evaluating the client's background, determining if ethical requirements can be met, assessing if other professionals are needed, communicating with prior auditors, preparing a client proposal, selecting an audit team, and obtaining an engagement letter.