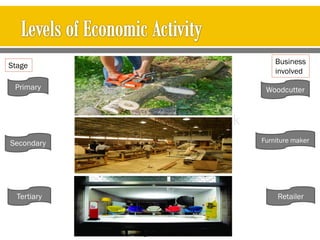

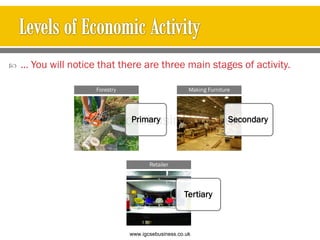

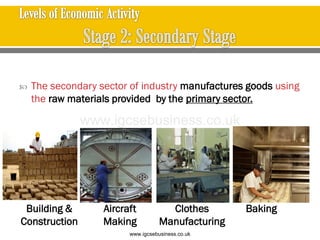

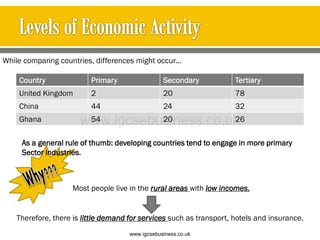

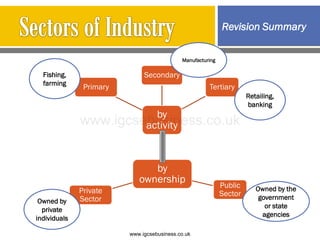

The document discusses the three sectors of industry: primary, secondary, and tertiary. The primary sector involves extraction of natural resources, such as farming, fishing, and forestry. The secondary sector involves manufacturing goods from raw materials provided by the primary sector, such as aircraft making and clothes manufacturing. The tertiary sector provides services to both consumers and businesses, including transportation, banking, hotels, and hairdressing. Developing countries tend to engage more in primary industries while developed countries employ more people in secondary and tertiary sectors. Most countries have mixed economies with both private and public sectors.