Duty Drawback (DBK)Scheme

Duty DBK is trusted and time tested scheme to promote exports - rebates incidence of

customs & Cex duties – WTO compliant scheme ensure exports are Zero rated & don’t carry

burden of specified taxes

Various Schemes like EOU, SEZ, DFIA, AA, EPCG enables import of goods without payment of

customs duty – suppliers who are unable to avail these scheme can avail Duty Drawback Scheme-

DBK nothing but remission of duty statutorily

Types of Duty Drawback

(a) All Industry Rate – AIR – (b) Brand Rate ( C) DBK on re-export of imported goods – Sec.74

Sec.74- Duty drawback when imported goods are re-exported - Sec.75- imported materials used in

manufacture of goods which are exported

3.

DBK Scheme –Features

AIR Scheme – Features

Simple mechanism based on the shipping bill declaration, without requiring additional

documentation

Involves end-to-end electronic processing of Duty Drawback;

Disbursal of Duty Drawback directly to exporters’ accounts – scrutiny, sanction and

payment at EDI locations is carried out through the EDI system - directly to the exporter’s

bank account

no need for producing separate documentary evidence regarding realisation of export

proceeds.

4.

AIR Scheme

All IndustryRate – AIR

Fixed by Directorate of Drawback. DoR, MoF – Generally notified every year

After 1.10.2017 DBK only on customs duty portion (no duty drawback on GST portion)

Fixed for broad categories of products - - Tariff Item & Description of goods aligned with Customs

Tariff for Four Digits – based on HSN classification- scheduled covers about 2620 entries – rates

are ad valorem/specific rate – inclusive of drawback for packing materials - fixed on FOB

value (when based on value) Rate Per unit (in case based on weight)

Rates based on weighted average of imported/indigenous inputs – no relation to actual

consumption or actual duty incidence suffered

5.

AIR Scheme

Notfn.No. 7/2020 Cus NT dated 28th

Jan 2020 - Unit/Drawback rate/Cap Per unit - Cellular

Mobile Phone- 851701 – Piece – 4% - value cap 350/- -Bananas 0803 – 0.15%

AIR shall not exceed 33% of market price of exported goods (Rule 9 DBK Rules 2017)

Value cap – to avoid misuse in overvaluation of export goods

AIR not applicable to following – goods manufactured in customs bonder warehouse –

manufactured under AA/DFIA – goods imported under DFIA – exports by EOU/SEZ

6.

Brand Rate –Features

Provides for a rebate of actual duty incidence suffered by an export product.

a specific Duty Drawback rate can be applied for by the exporter if the export product does not

have an AIR or the available AIR neutralises less than 80% of the duties paid on

materials used in the manufacture of export goods.

Brand Rates are fixed by the local Commissioners of Customs having jurisdiction over

the place of export - Pending the fixation of Brand Rate - AIR where available, can be

availed upfront by the exporter; Provisional Brand Rate can be allowed by the

Commissioner of Customs on the exporter’s request

Brand Rate of Duty Drawback is disbursed electronically directly to exporter’s

account in a manner similar to the disbursal of AIR of Duty Drawback.

AIR possible only for standard products – not suitable for specific products

7.

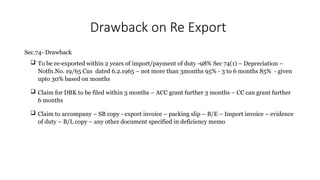

Drawback on Re-Export

DutyDrawback on re-export of imported goods:

Duty Drawback of up to 98% of import duty paid can be claimed on such exports.- Proof of duty

paid on importation and identification of the export goods are essential.

Sec.74- Drawback

Granted in terms of Re-export of Imported Goods (Drawback of Customs Duties) Rules, 1995.-

(a) goods are identified to the satisfaction of ACC (b) entered for re-export within two

years from date of payment of duty on importation

Where the goods are not put into use, 98% Drawback is admissible. Otherwise drawback is

granted based on period of use – depreciation value as notified S.74(2)

8.

Drawback on ReExport

Sec.74- Drawback

To be re-exported within 2 years of import/payment of duty -98% Sec 74(1) – Depreciation –

Notfn.No. 19/65 Cus dated 6.2.1965 – not more than 3months 95% - 3 to 6 months 85% - given

upto 30% based on months

Claim for DBK to be filed within 3 months – ACC grant further 3 months – CC can grant further

6 months

Claim to accompany – SB copy - export invoice – packing slip – B/E – Import invoice – evidence

of duty – B/L copy – any other document specified in deficiency memo

9.

Drawback- Other aspects

repatriation of export proceeds not pre-requisite – if proceeds not received within the period stipulated by RBI

– DBK will be recovered as per Rules - special checks, in cases of first time exporters, exporters who

have taken large amounts of drawback suddenly, sensitive destinations, sensitive products etc.,

to ensure there is no misuse of the drawback facility.

Penal Provisions

Fraudulently avails or attempts to avail drawback in connection with export of goods (S.135 (1) (d)) – In

case of offence relating to fraudulently availing/attempting to avail drawback amount exceeding fifty lakh

rupees punishable with imprisonment for a term which may extend to seven years and with fine

• Appeal Provisions

Against order of authority below CC (A) – to file appeal before CC (A) – S.128 of CA 1962 - No

appeal before CESTAT – Proviso (c ) to S. 129A (1) of CA 62 – appeal will lie before Central Govt –

Revision by Central Govt – Sec.129DD – Addl Secretary

10.

Drawback- Recovery

Sec.75A (2)where any drawback has been paid erroneously or becomes recoverable under the Act,

the claimant shall within 2 months from date of demand pay the DBK along with interest u/s 28AA

On reading of Section 75A(2) of the Customs Act, it is clear that when the claimant is liable to pay the excess

amount of drawback he is liable to pay interest as well. The section provides for payment of interest

automatically along with excess drawback. No notice need be issued separately as the payment of interest

become automatic, once it is held that excess drawback has to be repaid. (CPS Textiles Vs Jt Secretary

2010 (255) E.L.T. 228 (Mad.)

Rule 17 of Cus & Cex DBK Rules 2017 – any amount of DBK/Interest paid erroneously –claimant on

demand by proper officer repay the amount – shall also be recovered under Sec.142 of CA 1962 ( s.142 –

recovery of sums due to Govt – deduct from any money due- detaining & selling goods – auction of

movable/immovable properties )