Download to read offline

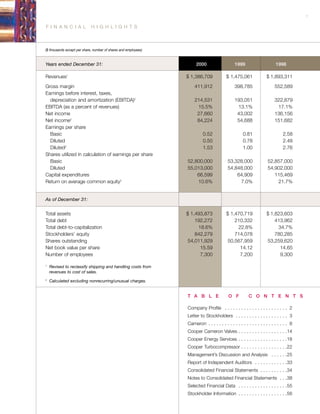

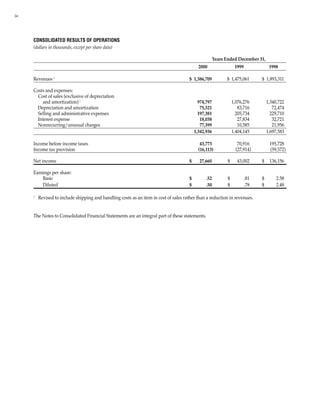

Cooper Cameron's annual report for 2000 provides financial highlights and discusses business performance. Key points include: - Revenues for 2000 were $1.39 billion, down from 1999 but excluding a business that was sold. Earnings before interest, taxes, depreciation and amortization (EBITDA) increased 11% to $214.5 million. - The company began a Six Sigma program to improve manufacturing and service results across divisions, with over 50 projects already underway. - Nonrecurring restructuring charges of over $77 million were recorded, mostly related to closing old facilities. Restructuring is expected to be completed by mid-2001. - The balance sheet remains strong with debt reduced to