1. Ashikur Rahman Tushar (1220665)

Ratio Analyzed on the basis of Annual Report 2012 & 2013.

Ratio Analysis and Overview of the Financial Performance of

BEXIMCO Pharmaceuticals Ltd.

Based on the Annual Auditor’s Report 2012 and 2013.

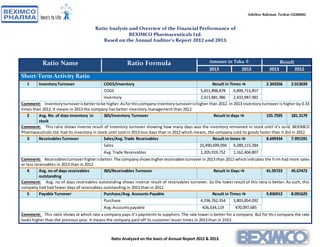

Ratio Name Ratio Formula Amount in Taka Result

2013 2012 2013 2012

Short-Term Activity Ratio

1 InventoryTurnover COGS/Inventory Result in Times 2.343356 2.013039

COGS 5,651,898,878 4,899,713,857

Inventory 2,411,881,986 2,433,987,981

Comment: Inventoryturnoverisbettertobe higher.Asforthiscompanyinventoryturnoverishigher than 2012. In 2013 inventory turnover is higher by 0.33

times than 2012. It means in 2013 the company has better inventory management than 2012.

2 Avg. No. of days Inventory in

stock

365/Inventory Turnover Result in days 155.7595 181.3179

Comment: This ratio shows inverse result of Inventory turnover showing how many days was the inventory remained in stock until it’s sold. BEXIMCO

Pharmaceuticals Ltd. had its inventory in stock until sold in 2013 less days than in 2012 which means, the company sold its goods faster than it did in 2012.

3 ReceivablesTurnover Sales/Avg.Trade Receivables Result in times 8.699334 7.991291

Sales 10,490,699,094 9,289,115,284

Avg.Trade Receivables 1,205,919,752 1,162,404,807

Comment: Receivablesturnoverhigherisbetter.The companyshowshigherreceivablesturnover in 2013 than 2012 whichindicates the firm had more sales

or less receivables in 2013 than in 2012.

4 Avg. no of days receivables

outstanding

365/Receivables Turnover Result in Days 41.95723 45.67472

Comment: Avg. no of days receivables outstanding shows inverse result of receivables turnover. So the lower result of this ratio is better. As such, this

company had had fewer days of receivables outstanding in 2013 than in 2012.

5 Payable Turnover Purchase/Avg. Accounts Payable Result in Times 9.836912 8.091625

Purchase 4,196,762,354 3,803,854,092

Avg.Accountspayable 426,634,119 470,097,685

Comment: This ratio shows at which rate a company pays it’s payments to suppliers. The rate lower is better for a company. But for this company the rate

looks higher than the previous year. It means the company paid off its customer lesser times in 2013 than in 2012.

2. Ashikur Rahman Tushar (1220665)

Ratio Analyzed on the basis of Annual Report 2012 & 2013.

6 Avg. no of days Payables

outstanding

365/Payables turnover Result in Days 37.10514 45.10837

Comment: Avg.no of days payables outstanding of lower indicates better payables performance the company possess. It means the company had been in

debt fewer days to its suppliers or more capable of paying its suppliers in time. This company indicates it has lower no. of days of payables outstanding.

7 WorkingCapital Turnover Sales/Avg.Working Capital Resultin Times 1.480257 1.80987

Sales 10,490,699,094 9,289,115,284

Avg.WorkingCapital 7,087,079,642 5,132,477,184

Comment: This turnover ratio measures how much operating capital needed to maintain a given level of sales. For this company working capital turnover

declinedthatmeansoperatingcapital forthiscompanydeclinedforthe salesitincurred.Soitmeansthe firmdidn’thave bettersaleshigher working capital in

2013 than the year 2012.

Long-Term Activity Ratio

8 FixedAssetTurnover Sales/Avg.FixedAsset Result in Times 0.600159 0.566672

Sales

10,490,699,094 9,289,115,284

Avg.fixedasset

17,479,859,057 16,392,388,639

Comment: Fixed asset turnover measures the amount of sales generated by the investment in or by acquiring the fixed asset. For this company sales

generated 0.04 times higher than the previous year which is good by the way.

9 Total Asset turnover Sales/Avg.Total Asset Result in Times 0.403019 0.377763

Sales 10,490,699,094 9,289,115,284

Avg.Total Asset 26,030,281,197 24,589,810,592

Comment:This turnoverratiorepresentsthe amountsalesgenerate bythe total assetorhowmuch of the total asset contributed to sales. The higher it is the

betteritis forthe company. In case of this company the turnover ratio rose by 0.03 times than the previous year which is good but the turnover result is not

sufficient enough for the company.

Working Capital Ratios and Defensive Interval

10 Current Ratio Current Asset/CurrentLiabilities Result in Ratio 2.031548:1 2.674574:1

CurrentAsset 8,903,422,328 8,197,421,953

CurrentLiabilities 4,382,581,278 3,064,944,769

Comment: This ratio measure how much current asset a company holds against the current liabilities or cash resources in current assets . The

higher the result the better it is for the company. The industry standard for this ratio is 2:1. For this company, the ratio fell down in 2013 by 0.64

times which is not good and it has result above the industry standard which also means that it had underutilized current assets.

3. Ashikur Rahman Tushar (1220665)

Ratio Analyzed on the basis of Annual Report 2012 & 2013.

11 Quick Ratio (Cash + Marketable Securities+ Acc.

Receivables)/CurrentLiabilities

Result in Ratio 0.421023:1 0.559678:1

Cash 595,732,966 552,978,676

Marketable Securities 0 0

AccountsReceivables 1,249,434,697 1,162,404,807

CurrentLiabilities 4,382,581,278 3,064,944,769

Comment: Quick ratio defines the liquid assets that can be quickly converted to cash. It reflects the amount of liquid asset it holds for every Tk. 1

worth of current liabilities. The industry standard is 1:1 for this ratio. According to the result this means the company had not enough liquid assets

against the current liabilities and the ratio also declined which also shows lack of better liquidity.

12 Cash Ratio (Cash + Marketable Securities)/CurrentLiabilities Result in Percentage 13.59% 18.04%

Cash 595,732,966 552,978,676

Marketable Securities 0 0

CurrentLiabilities 4,382,581,278 3,064,944,769

Comment: Thisratio isthe most conservative measure of cashresources.Thisratiodeclinedinrespectof the previousyearforthiscompany whichmeansthe

company had less cash resources than the previous year.

13 Cash Flow from Operations

Ratio

Cash Flow from Operations/CurrentLiabilities Result in Percentage 48.61% 60.60%

Cash FlowfromOperations 2,130,330,758 1,857,380,070

CurrentLiabilities 4,382,581,278 3,064,944,769

Comment: Cash flow from operations declined by 11.99% in a year which shows BEXIMCO Pharmaceuticals company had less cash flow from operations in

2013 than in 2012.

14 Defensive Interval 365 × {(Cash + Marketable Securities+ Acc.

Receivables) ÷ProjectedExpenditure}

Result in Days 82.47012 88.41889

Cash 595,732,966 552,978,676

Marketable Securities 0 0

AccountsReceivables 1,249,434,697 1,162,404,807

ProjectedExpenditure 8,166,426,324 7,081,235,724

Comment: This ratio measures how much time a firm needs to generate liquid assets to support projected expenditure. The lower result is better for this

ratio. The time to generate liquid assets is less in 2013 with respect o 2012 which is better for the company.

Capitalization Table and Debt Ratio

15 Debt to Capital Total Debt/Total Capital Result in Percentage 21.47% 19.03%

4. Ashikur Rahman Tushar (1220665)

Ratio Analyzed on the basis of Annual Report 2012 & 2013.

Total Debt 5,407,473,943 4,325,496,985

Total Capital (Total Debt+ Total Equity) 24,458,122,850 22,068,946,116

Comment: This ratio measures how much amount of the total capital a company has in its capital structure as debt. The lower percentage is better for this

ratio.Because the lowerthe debtthe lessriskyacompany is. But for the companythe percentage of its debt in the capital increased by the year which is not

good for a company.

16 Debt to Equity Total Debt/Total Equity Result in Percentage 27.34% 23.50%

Total Debt 5,407,473,943 4,325,496,985

Total Equity 19,775,552,465 18,408,161,859

Comment: Thisratio reflectshowmuchdebta companyhasagainstits equity.Itmeansfor Tk. 1 worth of equity how much debt a firm has. The lower result

of this ratio is better. But for this company this ratio increased by almost b4% by one year.

Interest Coverage Ratio

17 TimesInterestEarned Ratio EBIT/Interest Expense Result in Percentage 3.65% 3.42%

EBIT 2,324,272,770 2,207,879,560

InterestExpense 636,587,090 645,406,575

Comment: Thisratio measures the interestcoverage ratioorearningsavailable tocoverinterestexpense.The lower ratio is better. But for this company the

ratio shows an increment which is not good.

18 Cash Flow from Operationsto

Debt

Cash Flow from Operations/Debt

Result in Percentage 0.3940 0.4294

Cash FlowfromOperations 2,130,330,758 1,857,380,070

Total Debt 5,407,473,943 4,325,496,985

Comment: It measuresthe coverage of principal requirementbythe currentcash flow.The resultgreaterthan 1 is better for a company. Though the result is

greater than standard in 2013 but ratio declined which is not good.

Profitability Ratio

19 GrossMargin GrossProfit/Sales Result in Percentage 46.12% 47.25%

Gross Profit 4,838,800,216 4,389,401,427

Sales 10,490,699,094 9,289,115,284

Comment: This ratio shows how much percentage of gross profit generated from sales after incurring the cost of goods that had been sold. The higher the

result of this ratio is better. But the percentage declined for the company in 2013.

20 OperatingMargin/Margin

Before Interestand Tax/Return

on Sales

EBIT/Sales Result in Percentage 22.16% 23.77%

5. Ashikur Rahman Tushar (1220665)

Ratio Analyzed on the basis of Annual Report 2012 & 2013.

EBIT 2,324,272,770 2,207,879,560

Sales 10,490,699,094 9,289,115,284

Comment: It showsthe percentage of profit generated from sales after performing operating expenses. The higher the percentage the better it is. But the

percentage of operating profit also declined for the company in 2013 which is not good.

21 Pretax Margin Earnings Before Tax/Sales Result in Percentage 19.96% 20.56%

EarningsBefore Tax 2,093,594,171 1,909,829,236

Sales 10,490,699,094 9,289,115,284

Comment: It reflectsthe percentage of incomefromsalesbeforetaxes.The higherpercentageis betterforthe company. But pretax margin also declined for

the company.

22 Profit Margin NetIncome/Sales Result in Percentage 13.40% 14.20%

NetIncome 1,406,104,399 1,319,389,328

Sales 10,490,699,094 9,289,115,284

Comment: This ratio shows the percentage of net income on sales after incurring all the expenses. The higher percentage is better for the company. But

profit margin also declined for the company.

Return on Investment

23.1 Return on Asset(ROA) EBIT/Avg. Total Asset Result in Percentage 8.93% 8.98%

EBIT 2,324,272,770 2,207,879,560

Avg.Total Asset 26,030,281,197 24,589,810,592

Comment: It showsthe percentage of income generatedbyutilizingtotal assets. The higherpercentageisbetterforthe company.Butthe percentage is very

low and it also decline in 2013.

23.2 DU Pont ROA Total Asset Turnover × Return on Sales Result in Percentage 8.93% 8.98%

Comment: It is anothermeasure of calculatingROA whichiscalled‘Disaggregationof ROA’.Ithassame attributesasROA and for this ratio the result is same

as ROA.

24 Return on Total Capital (ROTC) EBIT/Avg. Total Capital Result in Percentage 9.70% 9.71%

EBIT 2,324,272,770 2,207,879,560

Avg.Total Capital 23,958,342,626 22,733,658,844

Comment: Itshowsthe percentage of income generatedbyfinancing.The higherpercentage isbetter for the company. But the percentage is very low and it

decreased in 2013 by 01%. Though the decrement is not so much but 01% decrement holds much enough of the amount in tk. which really matters.

6. Ashikur Rahman Tushar (1220665)

Ratio Analyzed on the basis of Annual Report 2012 & 2013.

25 Return On Equity (ROE) NetIncome/Avg. Stockholders’Equity Result in Percentage 7.36% 7.17%

NetIncome 1,406,104,399 1,319,389,328

Avg.Stockholders’Equity 19,091,857,162 18,408,161,859

Comment: Thisratio measuresthe percentage of income generatedbyequityfinancing. Higherpercentageof this ratio is better for this company. The radio

for this company increased in 2013 which is good.

26.1 DU Pont ROE ROA × (Asset÷ Equity) Result in Percentage 12.40% 12.00%

ROA 0.0893 0.0898

Asset 27,470,751,802 24,589,810,592

Equity 19,775,552,465 18,408,161,859

Comment: It is another measure of calculating ROE which is called ‘Disaggregation of ROE’. It has same meaning as ROE and this ROE measures shows the

percentage increased which is better. Different ROE measures can show different results.

26.2 DU Pont ROE ROA + [(ROA - Costof Debt) × (Debt/Equity) Result in Percentage 11.17% 10.96%

Total Debt 5,407,473,943 4,325,496,985

Equity 19,775,552,465 18,408,161,859

Cost of Debt 0.73 0.30

Equity 19,775,552,465 18,408,161,859

Comment: It is another measure of calculating DU Pont ROE. This ratio increased in 2013 than it was in 2012 which shows better performance of the

company.

26.3 DU Pont ROE [ ROA - (InterestCost ÷ Asset)]× (Asset÷ Equity) Result in Percentage 9.19% 8.49%

Interestcost 636,587,090 645,406,575

Asset 27,470,751,802 24,589,810,592

Equity 19,775,552,465 18,408,161,859

Comment: It is another measure of calculating DU Pont ROE. This ratio increased in 2013 than it was in 2012 which shows better performance of the

company.

27 Return on Common Equity

(ROCE)

(NetIncome-PreferredDividends)/Avg.Common

Equity

Result in Percentage 42.94% 43.31%

NetIncome 1,406,104,399 1,319,389,328

PreferredDividend 0 0

Avg.CommonEquity 3,274,869,785 3,046,390,500

Comment: Thisratio reflectsthe percentageof netincome generatedbyequityfinancingaftergivingpreferreddividends,A firm with preferred stockholders

takesthisratio incounterto measure ROE. Higherresultof this ratio is better for the company. But for this company the ratio declined which is not showing

7. Ashikur Rahman Tushar (1220665)

Ratio Analyzed on the basis of Annual Report 2012 & 2013.

better performance. The firm must have given more preferred dividends or had less income for the year 2013.

28 Financial Leverage Effect (FLE) OperatingIncome/NetIncome Result in Percentage 1.65299 1.67341

OperatingIncome 2,324,272,770 2,207,879,560

NetIncome 1,406,104,399 1,319,389,328

Comment: This ratio measures the sensitivity of a company’s earnings per share (EPS) to fluctuations in its operating income, as a result of changes in its

capital structure. The ratio shows that the higher the degree of financial leverage, the more volatile is EPS. So the lesser it is the better it is for a firm. The

leverage effect declined in 2013 from 2012 by 0.02 times.

29 Basic EPS (NetIncome - PreferredDividend) ÷ Weighted

avg. Common shares outstanding

Result in Taka 4.01 3.77

NetIncome 1,406,104,399 1,319,389,328

PreferredDividend 0 0

Weightedavg.no.of commonshares 350,334,907 350,334,907

Comment: It showthe amount of earning a common shareholder is going to get for a share after distributing preferred dividends. It is good to have higher

EPS. The EPS for this company rose in 2013 by Tk. 0.24 than the previous year.

30 DividendPayout Ratio Dividend/NetIncome Result Ratio 0.00003:1 0.00026:1

Dividend 47,581 340,504

NetIncome 1,406,104,399 1,319,389,328

Comment: Dividend is not mandatory for accompany to declare. But it is good for the common shareholders to have dividends. To increase the amount of

investment in the company stocks by the common shareholders a company must have better dividend payout ratio. The di vidend payout ratio for this

company is very low which is not at all a very considerable.

8. Ashikur Rahman Tushar (1220665)

Ratio Analyzed on the basis of Annual Report 2012 & 2013.

Overview of the Financial Performance of BEXIMCO Pharmaceuticals Ltd

BEXIMCO Pharmaceuticals Ltd. is a renowned pharmaceutical company in Bangladesh. It is a very large pharmaceuticals company with a millions

of revenues and shareholders. It is has been established decades ago. From the beginning until now it has been very active with their

performance and it had high-low performance like every company has for a period of days, months or years. For past few years it has been in top

three in the ranking of pharmaceuticals industries.

But if we look at the past two years (2012 and 2013) performance of this company may be we would have a recent idea about this company’s

financial performance. I have calculated all the ratios for the BEXIMCO Pharmaceuticals Ltd and now let’s have an overview of its financial

performance according to ratio category.

Short Term Activity Ratio: After calculating all the short term activity ratios we can see the company had a positive performance in 2013

than 2012 with its short term activity ratio. All the ratios within it had positive trend.

Long Term Activity Ratio: BEXIMCO Pharma also shows a better performance and a positive trend with its long term activity ratios.

Working Capital Ratios and Defensive Interval: BEXIMCO Pharma didn’t have better performance with its working capital according to

this ratio. Because the ratios within it shows negative trend except defensive interval ratio.

Capitalization Table and Debt Ratio: This ratio reflects a negative trend of the company’s capitalization ratio. The company had more debt

to its equity and capital in 2013 than in 2012.

Interest Coverage Ratio: In this ratio category the company had negative performance or trend.

Profitability Ratio: The profitability ratios of this company is good enough by figure but not with the trend. The profitability also shows

decrease in percentage of profits in 2013 than in 2012.

Return on Investment: Return on investment of the company indicates that it didn’t have better ROA, ROTC but had better ROE, ROCE. It

reflects the company had average performance with its return on investment.

So after analyzing all the ratios we can comment that BEXIMCO Pharmaceuticals Ltd. didn’t have better performance in 2013 comparing the year

2012.