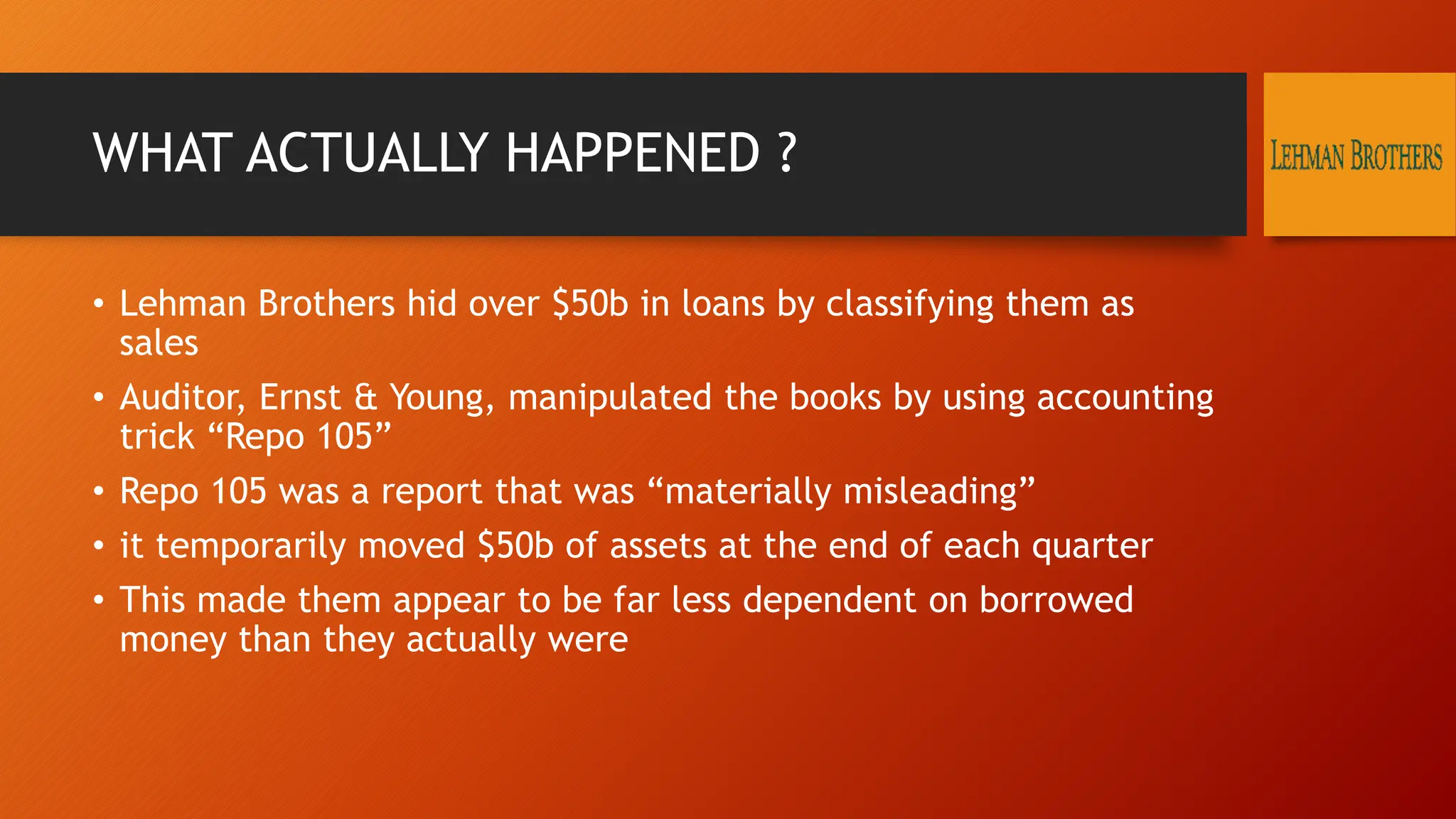

Lehman Brothers filed for bankruptcy in 2008 due to excessive risk taking and losses related to the subprime mortgage crisis. To hide their troubled financial position, Lehman executives and their auditor, Ernst & Young, used an accounting maneuver called Repo 105 to temporarily move $50 billion in assets off their balance sheet at the end of each quarter. This made the bank appear healthier than it really was. When the financial markets deteriorated, Lehman was unable to mask its true risks and liquidity problems any longer. Its bankruptcy highlighted the need for greater transparency, accountability, risk management and ethical leadership in the financial industry.

![Http _hist6rest.files.wordpress.com_2008_03_historia-de-la-restauracion-2[1]](https://cdn.slidesharecdn.com/ss_thumbnails/httphist6rest-files-wordpress-com200803historia-de-la-restauracion-21-120923180742-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)