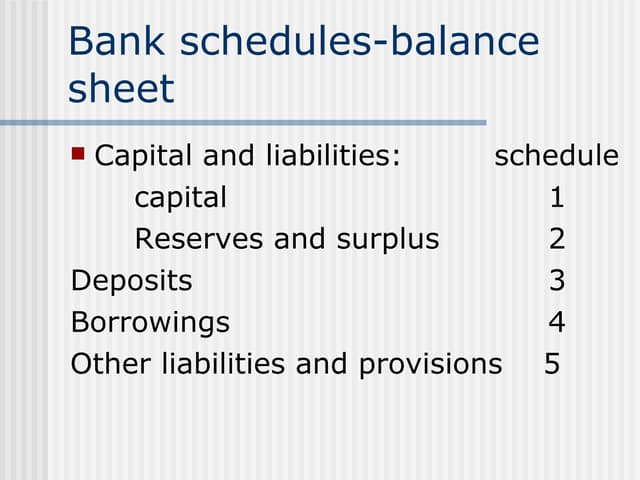

The document discusses various banking and accounting procedures. It covers topics such as checking accounts, electronic funds transfers, payroll procedures, financial statements, budgeting, and inventory management. It also addresses international currency exchange and the importance of ethics in accounting.

![Accounting entries[1]](https://cdn.slidesharecdn.com/ss_thumbnails/accountingentries1-130712041544-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)