Auditing A Practical Approach Canadian 2nd Edition Moroney Solutions Manual

Auditing A Practical Approach Canadian 2nd Edition Moroney Solutions Manual

Auditing A Practical Approach Canadian 2nd Edition Moroney Solutions Manual

Auditing A Practical Approach Canadian 2nd Edition Moroney Solutions Manual

Auditing A Practical Approach Canadian 2nd Edition Moroney Solutions Manual

1.

Visit https://testbankdeal.com todownload the full version and

explore more testbank or solutions manual

Auditing A Practical Approach Canadian 2nd Edition

Moroney Solutions Manual

_____ Click the link below to download _____

https://testbankdeal.com/product/auditing-a-practical-

approach-canadian-2nd-edition-moroney-solutions-manual/

Explore and download more testbank or solutions manual at testbankdeal.com

2.

Here are somerecommended products that we believe you will be

interested in. You can click the link to download.

Auditing A Practical Approach Canadian 2nd Edition Moroney

Test Bank

https://testbankdeal.com/product/auditing-a-practical-approach-

canadian-2nd-edition-moroney-test-bank/

Auditing A Practical Approach 3rd Edition Moroney

Solutions Manual

https://testbankdeal.com/product/auditing-a-practical-approach-3rd-

edition-moroney-solutions-manual/

Auditing A Practical Approach 1st Edition Moroney

Solutions Manual

https://testbankdeal.com/product/auditing-a-practical-approach-1st-

edition-moroney-solutions-manual/

Essentials of Comparative Politics 4th Edition ONeil Test

Bank

https://testbankdeal.com/product/essentials-of-comparative-

politics-4th-edition-oneil-test-bank/

3.

Methods Doing SocialResearch 4th Edition Jackson Test

Bank

https://testbankdeal.com/product/methods-doing-social-research-4th-

edition-jackson-test-bank/

Earth Portrait of a Planet 6th Edition Marshak Solutions

Manual

https://testbankdeal.com/product/earth-portrait-of-a-planet-6th-

edition-marshak-solutions-manual/

Financial Accounting A Critical Approach CANADIAN Canadian

4th Edition John Friedlan Test Bank

https://testbankdeal.com/product/financial-accounting-a-critical-

approach-canadian-canadian-4th-edition-john-friedlan-test-bank/

Essentials of Modern Business Statistics with Microsoft

Excel 5th Edition Anderson Test Bank

https://testbankdeal.com/product/essentials-of-modern-business-

statistics-with-microsoft-excel-5th-edition-anderson-test-bank/

Introduction to Clinical Psychology 4th Edition Hunsley

Test Bank

https://testbankdeal.com/product/introduction-to-clinical-

psychology-4th-edition-hunsley-test-bank/

4.

Handbook of Informaticsfor Nurses and Healthcare

Professionals 5th Edition Hebda Test Bank

https://testbankdeal.com/product/handbook-of-informatics-for-nurses-

and-healthcare-professionals-5th-edition-hebda-test-bank/

5.

Solutions Manual

to accompany

Auditing:APractical

Approach

Chapter 6 – Sampling and overview of the risk response phase of the audit

SOLUTIONS TO REVIEW QUESTIONS

REVIEW QUESTION 6.1

Sampling risk relates to the chance that the sample is not representative of the

population. If the sample is representative of the population, both the sample results

and the results from testing the entire population would lead to the same conclusion.

Overreliance on an ineffective system of internal controls occurs when the sample

results indicate that internal controls are effective, but they are not. In this case the

auditor concludes, based on testing the sample, that the control risk is lower than it

really is. The auditor will not perform more testing and will rely on the controls. The

auditor faces the risk that they will not detect a material misstatement and provide an

inappropriate audit opinion.

Under-reliance on an effective system of internal controls occurs when the sample

results indicate that internal controls are not effective, but they really are. In this case,

the auditor concludes that the control risk is higher than it really is, and performs more

testing or decides not to rely on the internal controls. The auditor will eventually realize

that the controls are better than first thought, but additional time and money will be

spent on testing which was not necessary.

Both overreliance and under-reliance are problems for the auditor. The first exposes the

auditor to a higher audit risk than they planned, and the second exposes the auditor to

greater expense. The implications for the auditor depend on the extent of the problem

(i.e., whether the over or under reliance was extreme) and chance. For example, just

6.

because internal controlsare not as effective as they appear doesn’t mean that a

material or pervasive error will definitely occur in the client’s financial statements.

REVIEW QUESTION 6.2

Non-sampling risk is the risk that the auditor reaches an inappropriate conclusion for

any reason not related to sampling risk. For example, the auditor could misinterpret the

evidence or draw the wrong conclusion from the results because they didn’t understand

them. The auditor could have chosen the wrong type of test, or applied the test to

transactions from the wrong period. The auditor could have been given incorrect

information by management to conceal a fraud, which they didn’t detect using other

techniques. When testing controls, the auditor could choose to test a control that was

not critical to the integrity of the data. When gathering substantive evidence, the auditor

could make a mistake when recalculating a subtotal of a subsidiary ledger, or compare

the subtotal with the control account at the wrong date.

REVIEW QUESTION 6.2 (Continued)

Non-sampling risk is determined by the auditor’s expertise, experience and understanding of

the client. It differs from sampling risk which is created by using sampling from a population,

rather than examining every item. Even when examining every item in a population, an

auditor still faces non-sampling risk.

REVIEW QUESTION 6.3

Non-statistical sampling does not involve random selection and probability theory to

evaluate the results.

Non-statistical sampling is easier to use than statistical sampling and generally lower cost. The

auditor selects a sample that they believe is appropriate, and is used when the auditor

believes the account is low risk and the auditor has access to adequate corroborating

evidence from other sources.

Main methods are:

• Haphazard selection: selection of a sample by an auditor without using a methodical

technique. The auditor could introduce human bias (e.g., select items that are easier

to reach).

• Block selection: select items that are grouped together. Bias can be introduced where

the items are sorted in a sequence (e.g., date order).

• Judgemental selection: auditor uses judgement to select items that they believe

should be included in the testing (e.g., just after a new computer system is installed).

REVIEW QUESTION 6.4

7.

(1) If theauditor believes that the control is likely to be more effective, the auditor will seek to

rely on that control and reduce substantive testing. This means that the auditor will need

greater assurance and gather more appropriate audit evidence that the control does work

effectively. Greater assurance is provided by increasing the sample size.

(2) The acceptable, or tolerable, rate of deviation refers to the number of deviations (or

control errors) that the auditor will accept or tolerate. If the auditor is prepared to accept

more deviations, less audit evidence is required, and thus a smaller sample size is

required.

(3) The expected rate of deviation is the actual level of deviations that the auditor expects to

find in the population from the control, not the level that the auditor is prepared to tolerate.

If the auditor expects a higher rate of deviation than in the past, for example because the

client has changed its systems, the auditor will need to gather more evidence on which to

base their conclusion. This means that the sample size will be increased.

REVIEW QUESTION 6.4 (Continued)

(4) The auditor’s confidence in the test results is greater when there is more evidence

on which to base their conclusions. This means that if the desired level of

assurance, or confidence, that the tolerable rate of deviation is not exceeded by the

actual rate of deviation in the population is higher, the sample size must be larger.

(5) The number of units in the population has only a negligible effect on the sample size.

If the sampling is representative, a larger population should have little effect on the

ability of the auditor to draw a conclusion.

REVIEW QUESTION 6.5

Stratification occurs when the auditor divides the population into groups and then

selects items from each group. An example of when this would be appropriate is where

an entity has both cash and credit sales. As credit sales are generally riskier that cash

sales, sales could be divided into the two groups before a sample is selected.

REVIEW QUESTION 6.6

The auditor must consider whether an error is likely to be unique, and thus not likely to

be repeated throughout the population being tested. The auditor would also consider

whether the population was stratified before sampling. If neither of these circumstances

applies, the auditor would project the error to the population of sales invoices.

If the sample error is $25,300, it would not be appropriate to conclude that sales are

misstated by the same amount because this error was discovered in a sample of sales

8.

invoices. In thiscase, we are not told the total of sales invoices in the sample or the

total of sales invoices in the population, so an estimate of the projected error cannot be

made. However, to make the estimate the auditor would consider the size of the error in

relation to the sample size (sample error / sample size), and then the sample error rate

in relation to the population size (by multiplying sample error/sample size by the

population size).

REVIEW QUESTION 6.7

Tests of controls are audit procedures designed to evaluate the operating effectiveness

of controls in preventing, detecting and correcting, material misstatements at the

assertion level.

Substantive procedures are audit procedures designed to detect material misstatement

at the assertion level.

REVIEW QUESTION 6.7 (Continued)

Therefore, the difference between the two types of audit procedures is whether they

provide evidence about the effectiveness of the control systems at preventing or

detecting material misstatements from entering the accounts, or about the existence of

material misstatements in the accounts.

The results of the tests of controls indicate how likely it is that material misstatements

exist in the accounts. If it is unlikely that these misstatement exist (i.e., control risk is

low), then the auditor has gained some assurance from the control tests about the fair

presentation of the financial statements. The auditor then needs to gather only a limited

amount of evidence from substantive tests and can use less expensive and less

extensive substantive procedures. If it is likely that misstatements exist in the accounts

(i.e., control risk is high), then the auditor has only limited assurance from the control

tests about the fair presentation of the financial statements. The auditor must gain more

assurance from substantive tests and therefore is required to use more effective and

extensive substantive procedures. The auditor makes decisions about the nature,

timing, and extent of substantive procedures to achieve the required level of quality and

quantity of evidence from substantive testing.

REVIEW QUESTION 6.8

Analytical procedures can be used at various stages of the audit. CAS 315 Identifying

and Assessing the Risks of Material Misstatement Through Understanding the Entity

and Its Environment requires an auditor to obtain an understanding of the entity’s

internal controls, and design appropriate responses to the assessed risk of material

misstatement. The auditor could perform substantive procedures or tests of controls

concurrently with risk assessment procedures when it is efficient to do so. Paras A7-A9

9.

of CAS 315discuss the use of analytical procedures to help identify risks, such as those

revealed by unusual transactions or events and amounts, ratios or trends. For example,

the auditor could use the client’s interim trial balance to analyze relationships between

data such as cost of sales and sales, between non-financial data such as employee

numbers and financial data such as payroll expense, to identify areas or risk that would

require further testing.

CAS 330 The Auditor’s Responses to Assessed Risks requires the auditor to gather

sufficient appropriate audit evidence through designing and implementing the

appropriate responses to the assessed risk of material misstatement. For example, an

auditor could use a combination of procedures to gather evidence about the

effectiveness of controls. The auditor could make enquiries of management to obtain

explanations about the results of analytical procedures which indicate there is unusual

variance between budgeted and actual amounts.

REVIEW QUESTION 6.8 (Continued)

CAS 520 Analytical Procedures explains how analytical procedures are used as

substantive tests. It notes that substantive analytical procedures are generally more

applicable to large volumes of transactions that tend to be predictable over time (para

A6). These types of transactions could include expenses such as insurance, rent, power

related to asset values, building size, and production activity, respectively.

REVIEW QUESTION 6.9

Stratification is the process of dividing a population into groups of sampling units with

similar characteristics. This helps reduce the sample size as once items with similar

characteristics are segregated, fewer items in this strata need to be tested. This is

because by grouping items with similar characteristics, then items are homogeneous

and there is little benefit in increasing the sample size to confirm earlier findings.

An example of where this is appropriate is for accounts receivable where the auditor

may segregate high dollar items or items that are long overdue.

.

REVIEW QUESTION 6.10

High risk clients are more likely to have material misstatements in their accounts.

Auditors are not as able to rely on these client’s internal controls to detect or prevent

material misstatements. If an auditor gathers evidence which shows that the internal

control systems work effectively, there is a low risk that material misstatements will

occur between the date of the testing and the year end. However, if the evidence shows

that the internal control systems do not work effectively (i.e., a high risk client), there is a

10.

high risk thatmaterial misstatements will occur between the date of the testing and the

year end. This means that the auditor must gather evidence up to the year-end and just

after year-end for high risk clients.

11.

SOLUTIONS TO PROFESSIONALAPPLICATION QUESTIONS

PROFESSIONAL APPLICATION 6.1 – Sampling methods

(a)

Bob is conducting substantive testing of sales invoices. In order to gather evidence

about existence, Bob would need to sample the entries in the sales journal and then

vouch to the underlying documents. This would also allow evidence to be gathered

about the details of the sales transactions that is relevant to the accuracy, classification

and cut-off assertions.

In order to gather evidence about completeness of the accounting records, Bob would

sample the invoices, and then trace the details of the transactions to the sales journal.

This would also provide evidence relevant to the accuracy, classification and cut-off

assertions. In this case, Bob has to be careful about which invoices he samples. The

conditions in which the boxes of sales invoices are stored appear to be unsatisfactory.

He will have difficulty identifying the boxes of sales invoices relevant to the current year.

He will also have to be careful not just to sample the invoices that are in boxes near the

door or otherwise easy to access, because this would introduce bias to his sampling

and potentially invalidate his conclusions.

(b)

As noted above, there is an issue about identifying and accessing the sales invoices

because of the unsatisfactory conditions in the storage shed. Other information relevant

to sampling is the difficulties in the administration department. There have been periods

of staff shortages. The auditor should consider stratifying the sample and making sure

that they sample from the periods where staff conditions were different. This would

provide evidence about the effectiveness of controls under different conditions. The

auditor would consider the patterns in customer complaints – do they relate to specific

periods, or specific types of sales? Do the complaints suggest greater risk would apply

to different parts of the year? Overall, controls over sales invoices appear to be poor

and substantive testing should be extensive.

PROFESSIONAL APPLICATION 6.2 – Types of audit sampling and sampling risk

1. D – Non-sampling risk

2. C – Sampling risk

3. A – Statistical sampling

12.

PROFESSIONAL APPLICATION 6.3– Benefits of statistical sampling

Statistical sampling enables the auditor to use the most efficient sample size and to quantify

the sampling risk for the purpose of reaching a statistical conclusion about the population.

The major advantages of statistical sampling versus non-statistical sampling are that it

helps the auditor:

1. Design an efficient sample,

2. Measure the sufficiency of evidence obtained, and

3. Quantify sampling risk.

Disadvantages of statistical sampling to be overcome include the additional costs of:

1. Training auditors in the proper use of sampling techniques,

2. Designing and conducting the sampling application, and

3. The potential lack of consistent application across audit teams due to the

complexity of the underlying concepts.

Fortunately, this audit includes an auditor with training in statistical sampling, which will

mitigate these disadvantages.

PROFESSIONAL APPLICATION 6.4 – Sample selection in practice

(a)

Using a random number generator in Excel or on your calculator, any number between

1-12 may be selected. This corresponds to the appropriate month. For example, if the

random number generator produces the following items 5, 12, 6, and 4 – then May,

December, June, and April will be tested.

(b)

Haphazard selection — Pick any 4 months.

(c)

Block selection — Pick any starting point within the sample, and then pick four

consecutive months.

PROFESSIONAL APPLICATION 6.5 – Potential impact of sampling risk

No, Alexei cannot safely conclude that no additional work is needed, as he has not

considered sampling risk. He has only sampled 30 transactions, which amounted to less

than 1% of the sales balance. Because this is a small sample, the risk that the sample is

not representative of the population is significant. If the true misstatement rate in the

remainder of the population is higher, total misstatement could easily exceed the

tolerable error of misstatement.

13.

PROFESSIONAL APPLICATION 6.5(Continued)

The approach that should be taken is to project the misstatement (i.e., calculate the best

estimate of total misstatement in the population) and incorporate an amount in consideration

of sampling risk. There is an inverse relationship between sample size and sampling risk.

Without statistical methods, judgments about sampling risk are difficult to make. Thus,

sampling risk must be considered.

PROFESSIONAL APPLICATION 6.6 – Sample size selection

Patrizia should select a larger sample size in Case B as all the factors point to more sampling

risk in Case B.

PROFESSIONAL APPLICATION 6.7 – Sampling and non-sampling risk for control testing

(a)

Fred is gathering evidence over cash payment controls. This means that the population

definition must relate to the controls over cash payment transactions. Fred would need to

gain an understanding of controls over cash payments and identify the controls for each type

of potential misstatement, or ‘what could go wrong’ (WCGW). Fred would then sample from

the instances of each control, as required. For example, the cash payments are authorized

by a senior accountant in order to prevent unauthorized payments being made. Fred would

need to consider all authorizations as a population from which to sample. All cash payments

are based on a set of documents assembled and checked by the accounts staff; Fred would

need to regard all these sets of documents as a population and would sample a number of

sets of documents to test if the documents were assembled correctly and checked as

required. Fred would also sample from the processed cash payment transactions and test the

documents and authorizations on which the transactions are based. In this case, the

population is the processed cash payments.

(b)

Sampling risk refers to the possibility of drawing an incorrect conclusion about the population

based on the sample results. There is a possibility that the sample is not representative of the

population, and the sample deviation rate (departure from controls in the sample items) differs

significantly from the population deviation rate (departure from controls in the population).

Sampling risk could lead to the auditor concluding that the population contains more control

deviations than it actually does. In this case, the sample deviation rate is higher than the

population deviation rate. In this case the auditor would under-rely on the controls and

conduct further testing which was not necessary.

14.

PROFESSIONAL APPLICATION 6.7(Continued)

Sampling risk could lead to the auditor concluding that the population contains fewer control

deviations than it actually does. In this case, the sample deviation rate is higher than the

population deviation rate. In this case the auditor would over-rely on the controls and

conclude that the control is working effectively. The auditor would not conduct further testing

and has a higher risk of providing an inappropriate audit opinion.

(c)

Non-sampling risks always exist. The non-sampling risk is the risk that the auditor will make

an inappropriate conclusion based on anything other than sampling risk. That is, the auditor

misinterprets the evidence or misapplies the audit techniques. For example, in this case, the

auditor could fail to detect that cheques were countersigned by the chief accountant by being

careless when reviewing the documents. The auditor could fail to understand the significance

of certain cash payment entries being authorized for maintenance on items which were not

owned by the client (i.e., the maintenance was for a staff member’s private assets). The

auditor could fail to ask the chief accountant about their annual leave (vacation) and the

arrangements for counter-signing cheques whilst away.

PROFESSIONAL APPLICATION 6.8 – Determining sample size for control testing

• The number of accounts payable has increased by 50% since last year. An increase in

the population has a negligible effect on sample size.

• Bunns and Major has changed some of its suppliers. This changes the conditions

affecting accounts payable because the change has been from large corporate

wholesalers to direct dealing with manufacturers. There is a possibility that the two

groups of suppliers would have different levels of quality control over their supplier

statements. The auditor would need to consider if there was a decrease (increase) in

quality, and if so, increase (decrease) the sample size because there is potentially a

greater (lower) degree of error in the supplier statements (an increase/decrease in

the expected rate of deviation of the population to be tested).

• Belief that controls in accounts payable are likely to be operating more effectively than

in previous years because of additional staff, expecting a reduction in control

deviations. An expected reduction in control deviation leads to a lower sample size.

• A lower tolerable rate of deviation because of increased importance of accounts

payable to solvency analysis would lead to an increased sample size for control testing.

• An increased reliance on controls to justify less substantive testing means that the

sample size for control testing will increase (an increase in the extent to which the

auditor’s risk assessment takes into account relevant controls leads to increase in

sample size).

15.

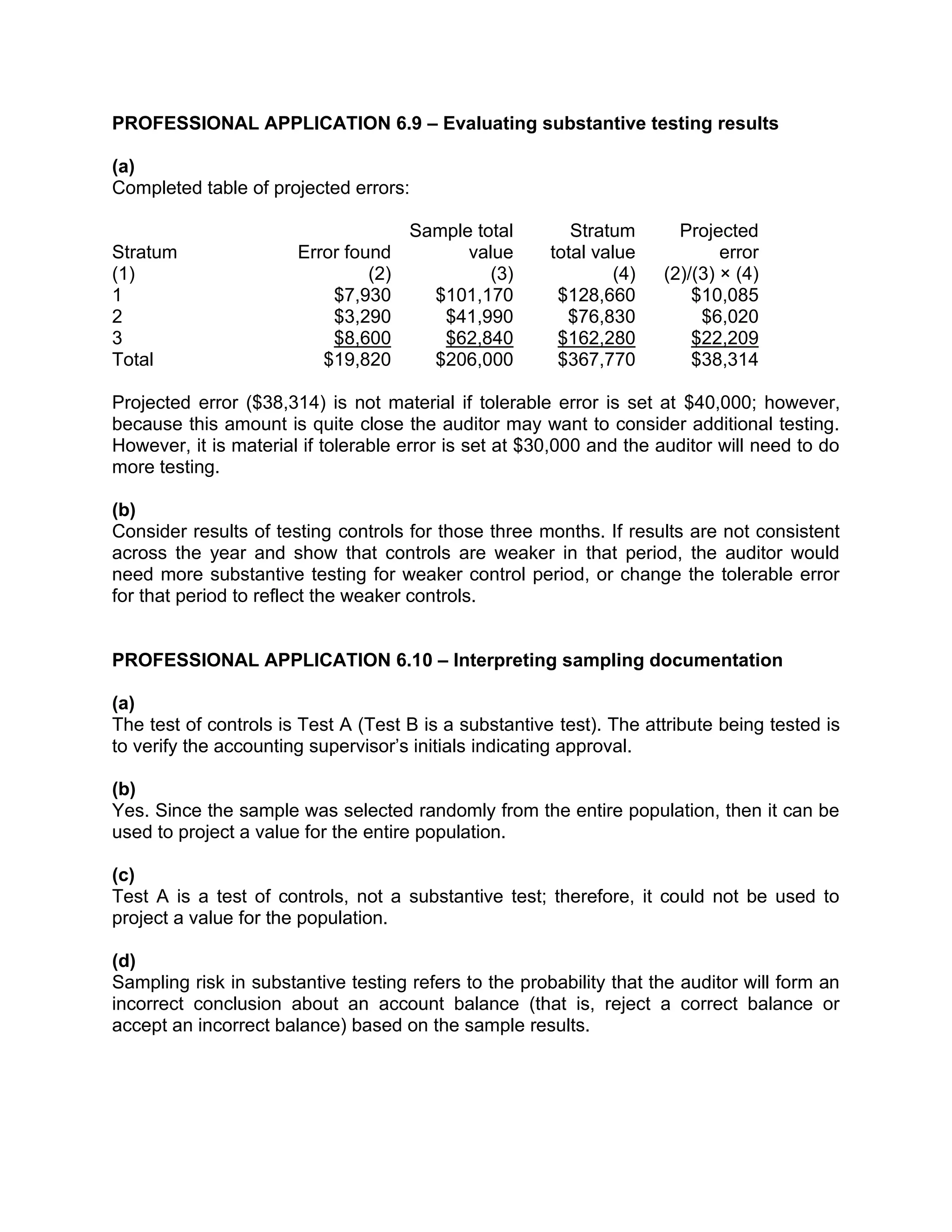

PROFESSIONAL APPLICATION 6.9– Evaluating substantive testing results

(a)

Completed table of projected errors:

Stratum

(1)

Error found

(2)

Sample total

value

(3)

Stratum

total value

(4)

Projected

error

(2)/(3) × (4)

1 $7,930 $101,170 $128,660 $10,085

2 $3,290 $41,990 $76,830 $6,020

3 $8,600 $62,840 $162,280 $22,209

Total $19,820 $206,000 $367,770 $38,314

Projected error ($38,314) is not material if tolerable error is set at $40,000; however,

because this amount is quite close the auditor may want to consider additional testing.

However, it is material if tolerable error is set at $30,000 and the auditor will need to do

more testing.

(b)

Consider results of testing controls for those three months. If results are not consistent

across the year and show that controls are weaker in that period, the auditor would

need more substantive testing for weaker control period, or change the tolerable error

for that period to reflect the weaker controls.

PROFESSIONAL APPLICATION 6.10 – Interpreting sampling documentation

(a)

The test of controls is Test A (Test B is a substantive test). The attribute being tested is

to verify the accounting supervisor’s initials indicating approval.

(b)

Yes. Since the sample was selected randomly from the entire population, then it can be

used to project a value for the entire population.

(c)

Test A is a test of controls, not a substantive test; therefore, it could not be used to

project a value for the population.

(d)

Sampling risk in substantive testing refers to the probability that the auditor will form an

incorrect conclusion about an account balance (that is, reject a correct balance or

accept an incorrect balance) based on the sample results.

16.

PROFESSIONAL APPLICATION 6.11– Results of control testing 1

(a) A tolerable deviation rate (or tolerable rate of deviation) is the rate of deviation

from prescribed controls set by the auditor in which the auditor seeks to obtain an

appropriate level of assurance that the rate of deviation set by the auditor not to

exceed the actual tolerable rate of deviation (see Para 5j CAS 530 Audit

Sampling) This is the maximum error an auditor is willing to accept within the

population tested and still conclude that controls are effective.

If the auditor intends to rely on a control to prevent and detect a material

misstatement, a lower tolerable deviation rate will be set and the sample size will

be increased to provide the auditor with the sufficient evidence required to

demonstrate that the control is effective. However, if the auditor expects to place

relatively more reliance on substantive procedures and reduce the reliance on

the internal control, the tolerable rate of deviation is increased and the sample

size is reduced when testing the control.

(b) ‘Exceptions’ are instances where the controls did not work as planned. In this

case the exception is one instance of part-time staff being paid an incorrect

hourly rate. This is the evidence that the controls on ensuring that correct hourly

rates of pay are used in calculating wages did not work effectively.

(c) Generally, an increase in the number of deviations, or control errors, increases

the confidence required from substantive testing. Greater confidence can come

from different types of tests (for example, tests of details rather than analytical

procedures), timing (covering a greater portion of the financial period, and/or

closer to balance date), and extent (increasing the sample size).

PROFESSIONAL APPLICATION 6.12 – Sampling methods and risk 3 4 5

The population for the tests of depreciation expense is the depreciable items included in

PPE. This includes both new items and existing items. The auditor should ensure that

disposals are removed from the asset register before the sample is taken.

Sampling PPE for the tests of depreciation expense should reflect the changed

conditions and the materiality of PPE to the balance sheet. The changed conditions

relate to the large investment in a new manufacturing process and the associated

increases in PPE acquisitions. The sampled items should include new acquisitions of

PPE (because these have not been tested before for depreciation), plus the larger items

(because the depreciation expense would likely be higher for these items).

Other considerations include the location of items (does FH have different branches?),

and types of equipment (are some pieces of equipment harder to value and make

estimates about useful life and depreciation rates?), and history (does management

made predictable types of misjudgements about useful life?).

17.

PROFESSIONAL APPLICATION 6.12(Continued)

The auditor could formally stratify the sample to select samples of new items and old

items, and different value items, or select a large enough sample to be reasonably sure

that the sample includes all types of items that are likely to be most at risk.

A random sample (either with or without stratification) would allow the auditor to make

conclusions using probability theory. The auditor could supplement the formal

conclusions based on a random sample with evidence obtained from samples of items

considered ‘important’ in the auditor’s judgement. This judgement would relate to the

consideration of which items are more likely to be depreciated inappropriately.

The assertions most at risk are the accuracy of depreciation expense and the valuation

and allocation for PPE (shown as cost less accumulated depreciation).

PROFESSIONAL APPLICATION 6.13 – Projecting errors for PPE

In order to project the error in the sample of $48,500 back to the population we use

information on the sample total value ($1,145,000) and the population total value

($11,345,000). The projection shows: projected error = errors found ÷ sample total value

× stratum total value = $48,500 / $1,145,000 × $11,345,000 = $480,552.

This means that PPE items with a value of $480,552 have inappropriate depreciation

rates. This error equates to approximately 4% of gross PPE, which is usually not

considered material. In this case, the auditor would conclude that the valuation and

allocation assertion for PPE was not violated.

Although we are not given the depreciation rate, the effect on profit before tax is likely to

be less than 4% (i.e., assuming 10% depreciation, the error in the expense is $48,055

which is 2.5% of profit before tax).

However, given that PPE is considered to be one of the most material balances, the

auditor might consider further testing or asking management to adjust the depreciation.

18.

PROFESSIONAL APPLICATION 6.14– Substantive testing and assertions

(a)

The sales team are remunerated in two ways; a base salary plus a bonus based on the

dollar values of sales. The bonus payment increases if the sales person increases

recorded sales. An inappropriate way of increasing sales is to record sales during the

year for samples given to customers, or to record sales to existing customers at year-

end when not ordered and then to reverse immediately after year-end, or to record a

sale prematurely (for example, before shipment to customer). When the sample is

returned following the year-end the sale is reversed or adjusted with a sales return or

allowance. Another way of increasing sales is to falsify sales by recording a sale to a

fictitious customer. The account balance is eventually written off for non-payment of the

account. The sales and accounts receivable account balances are at risk because of

these practices. The assertions at risk are occurrence and existence for the sales

transaction and accounts receivable balance. In addition, the valuation and allocation

assertion for accounts receivable is at risk because the balance does not represent the

amount that is reasonably expected to be received from customers.

(b)

The substantive test described in the question is to take a sample of payments received

by the hospital (i.e., cash receipts) and trace back to the general ledger and customer

account balance. Performing this test will provide evidence about the

existence/occurrence assertion for the accounts receivable and sales balances, and the

valuation and allocation assertion for accounts receivable. If the client receives cash for

the credit of an accounts receivable this is reliable evidence that the recorded sale did

occur and that the balance of accounts receivable was fairly stated at the year-end.

The reference to the bonus structure is to reinforce the risk to the occurrence assertion

for sales and the valuation and allocation assertion for accounts receivable.

PROFESSIONAL APPLICATION 6.15 – Substantive testing versus control testing

(a)

Test 1: This is a substantive test. The test gathers evidence about the balance of trade

creditors at year end and the total of purchases. In particular, the test is gathering

evidence about the date the goods were received and the date the entry is posted.

Test 2: This is a test of controls. The test is gathering evidence about the process of

reviewing and authorising the pricing and discount terms.

(b)

Test 1: Cut-off assertion for purchases, valuation and allocation assertion for trade

creditors. The dates are being verified to ensure the transactions are recorded in the

correct financial period.

19.

PROFESSIONAL APPLICATION 6.15(Continued)

Test 2: Controls over pricing and discounts are relevant to the valuation and allocation

assertion for trade creditors, and the accuracy assertion for purchases.

(c)

Test 1: The test does not address the issue of completeness for trade creditors or fully

address the cut-off assertion for purchases. The key risk for creditors is understatement. By

taking a sample from the list of trade creditors the auditor is not able to detect unrecorded

liabilities. The conclusion is not appropriate.

Test 2: The initial test reveals that 3 out of 20 invoices had not been authorized and incorrect

discounts were recorded. The follow-up shows no pattern. The conclusion refers to the

amount of the discount. This is not appropriate for a test of controls. The issue is whether the

rate of deviation in the control is tolerable. If the deviation rate in the sample is tolerable when

projected to the population, especially given the additional testing, then the auditor could

conclude that there is no significant deviation in the control. The auditor cannot conclude the

valuation of suppliers is fair based on the control tests alone.

(d)

Further procedure for test 1: The auditor should examine suppliers’ invoices and goods

received relating to the period following year-end. These documents could reveal an

unrecorded liability, that is, goods recorded as received after the year-end that were actually

received by the client prior to the year-end.

Further procedure for test 2: As outlined in part (c), the conclusion about the deviation in

controls should be considered in light of the tolerable deviation rate. The substantive testing

needs to be designed given the control risk as revealed by the control tests. Further

procedures would include selecting a sample of suppliers invoices, given the control risk, and

testing of pricing and discounts.

PROFESSIONAL APPLICATION 6.16 – Control testing in previous year

The junior auditor’s suggestion is not appropriate because the auditor needs to have

sufficient appropriate evidence about the effectiveness of controls in the current year. Any

change in either the controls or the conditions would make last year’s evidence not applicable

to the current period. At aminimum, there should be evidence that the conditions remained

the same and that the controls had not altered. The auditor also considers whether the

controls can provide sufficient control in the current circumstances. Even if there had been no

changes since last period, the auditor should still evaluate the effectiveness of the controls

and draw a conclusion on the degree to which the controls can be relied upon.

In this particular case, the controls were assessed with respect to their ability to ensure

compliance with the regulations. It is likely that additional work is required for the controls to

be assessed for effectiveness at preventing or detecting material misstatements at the

assertion level because this is a different objective.

20.

PROFESSIONAL APPLICATION 6.17– Auditing low-value assets

Substantive testing of the furniture at MICA would include:

• Inspection of documents relating to purchase and disposal of items and tracing to

the fixed asset continuity schedule (completeness for additions, valuation and

allocation, existence of items that have been disposed of)

• Inspection of documents relating to purchase of assets (or financing of assets)

for evidence of ownership (rights and obligations) and date of acquisition (cut-off

of additions)

• Vouching of new entries in asset continuity to underlying supplier invoices,

receiving documents, transfer documents (existence, cut-off)

• Inspection of physical assets recorded in the continuity schedule (existence)

• Recalculation of depreciation expense and review of expense relative to asset

values (accuracy, valuation and allocation)

• Review of repairs and maintenance account to ensure that items relate to repairs

and not purchase ofcapital items (classification, completeness)

• Observing staff in central asset purchasing department performing their duties

when updating the asset register (existence, completeness)

• Enquiries of management about asset purchasing decisions (existence, rights

and obligations)

PROFESSIONAL APPLICATION 6.18 – Testing accounts receivable

(a)

Emma will be testing the controls over accounts receivable to support her preliminary

assessment that the control risk is low. Evidence of low control risk allows Emma to

reduce the reliance on substantive testing for accounts receivable. She will be seeking

evidence that the controls over transactions and balances in the accounts receivable

area are effective and consistent. Effective controls mean the entity has a low risk of

violating the assertions: occurrence, completeness, accuracy, cut-off, classification,

existence, rights and obligations, and valuation and allocation.

(b)

If Emma is successful in obtaining evidence that controls are effective and consistent,

she will reduce the reliance on substantive testing. This means that she can use less

effective substantive techniques (e.g., rely more on observation and enquiry and less on

inspection of documents), vary the timing (e.g., conduct more interim testing and less

balance date testing), and reduce the extent of testing (e.g., inspect fewer documents).

PROFESSIONAL APPLICATION 6.18 (Continued)

21.

Emma could usethese common procedures to test the controls:

1. Inspection of documents for evidence of authorization (e.g., of prices, extending

credit to new customers, sales returns)

2. Inspection of documents for evidence that details included have been checked by

appropriate client personnel (e.g., that variations to prices have been authorized

by the sales director, etc.)

3. Observation of client personnel performing various tasks (e.g., opening mail,

reconciling receipts with customer statements)

4. Enquiry of client personnel about how they perform their tasks (e.g., following up

on outstanding accounts, making adjustments to client accounts)

5. Re-performing control procedures to test their effectiveness (e.g., bank

reconciliations, customer statement reconciliations)

22.

Case Study —Cloud 9

(a)

As discussed elsewhere in the solutions, opening a retail store creates new risks for

inventory and receivables (if sales are made on credit). For example, the risk of theft

increases. The store also introduces exposure to the risks associated with leasing

premises and equipment. Sales through a store are directly affected by matters

impacting on consumers, e.g., weather conditions, transport, etc., that are absorbed by

retailers when Cloud 9 makes wholesale sales. There would be additional issues

around cash because cash would be held in the premises and staff would be required to

deposit cash to the bank at the end of each day.

(b)

Recall that Audit Risk = Inherent Risk × Control Risk × Detection Risk. Audit risk (AR),

the risk of giving an inappropriate audit opinion, is a function of the client’s inherent risk

(IR), control risk (CR) and the auditor’s detection risk (DR). The business change would

increase inherent risk, thereby increasing audit risk.

(c)

Inventory will be affected by the need to hold inventory in the store to meet daily sales.

There will be a larger volume of smaller sales made (consumer sales would be smaller

than wholesale sales). There will be movements of inventory from the warehouse to the

store. There could be issues with sales returns as customers return items that do not fit,

etc., and risk of damage to inventory held in the store.

(d)

Assertions that are likely affected by the opening of the store include: occurrence of

sales, existence of inventory (theft issues), valuation of inventory (risk of obsolescence,

damage of goods in store).

(e)

The population would include: inventory items held in the store and warehouse –

sample for inventory; sales made – sample for testing validity or occurrence of sales;

cash receipts made by the store – testing for completeness of cash. The sampling

approach would be to select key items for testing – large sales transactions, inventory

items that make up the largest part of the inventory balance (e.g., high value items), and

take representative samples of the other items. The auditor would be concerned with

completeness of cash receipts and would test controls over cash at the store. Control

testing of inventory would focus on movements of inventory, either from the warehouse

to wholesale customers or to the store, and goods in transit controls. Further details are

provided in chapter 7 solutions.

23.

Research Question 6.1– McKesson & Robbins fraud research

The solution to this research question will depend on the sources selected by the

student and the information gathered.

However, some background on the scandal follows and is intended only as a brief primer.

McKesson & Robbins scandal (1938)

"The McKesson & Robbins, Inc. scandal of 1938 was one of the major financial

scandals of the 20th century. The company McKesson & Robbins, Inc. (now McKesson

Corporation) had been taken over in 1925 by Phillip Musica, who had previously used

Adelphia Pharmaceutical Manufacturing Company as a front for bootlegging operations.

Musica, a twice-convicted felon, used assumed names to conceal his true identity in

taking control of the two companies: Frank D. Costa at Adelphia Pharmaceutical and F.

Donald Coster at McKesson & Robbins. Although he was successful in expanding the

company’s legitimate business operations, Musica recruited three of his brothers, also

working under assumed names, one outside the company and two inside it, to generate

bogus sales documentation and to pay commissions to a shell distribution company

under their control. Eventually, McKesson & Robbins treasurer Julian Thompson

discovered the distribution company was bogus. It was eventually determined that about

$20 million of the $87 million in assets on the company’s balance sheet were phony.

In December 1938, the Securities and Exchange Commission (SEC) opened an

investigation and Musica was arrested. Only after he was booked, fingerprinted and

released on bond did the authorities realize that “Coster” was in reality Musica. His bond

was revoked and he committed suicide before he could be rearrested.

The McKesson & Robbins scandal led to major corporate governance and auditing

reforms. The SEC required that public companies have audit committees of “outside”

directors and that the appointment of auditors be approved by the shareholders. The

American Institute of Accountants (now the American Institute of Certified Public

Accountants) adopted audit standards requiring that auditors verify accounts receivable

and inventory."

(Sources: "http://en.wikipedia.org/wiki/McKesson_%26_Robbins_scandal_(1938)",

retrieved October 2011;and "http://www.americanfraud.com/mckesson.aspx", retrieved

October 2011).

all the actsand proceedings of the governor. The legislative power

was vested in the governor and a council of seven persons, who

were to be appointed by the governor at first, and hold their office

for two years; afterwards they were to be elected by the people. All

the laws of Mexico, and the municipal officers existing in the territory

before the conquest, were continued until altered by the governor

and council.

On the 15th of August, 1846, Commodore Stockton adopted a tariff

of duties on all goods imported from foreign parts, of fifteen per

cent. ad valorem, and a tonnage duty of fifty cents per ton on all

foreign vessels. On the 15th of September, when the elections were

held, Walter Colton, the chaplain of the frigate Congress, was

elected Alcalde of Monterey. In the mean time, a newspaper called

the "Californian," had been established by Messrs. Colton and

Semple. This was the first newspaper issued in California.

Early in September, Commodore Stockton withdrew his forces from

Los Angeles, and proceeded with his squadron to San Francisco.

Scarcely had he arrived when he received intelligence that all the

country below Monterey was in arms and the Mexican flag again

hoisted. The Californians invested the "City of the Angels," on the

23d of September. That place was guarded by thirty riflemen under

Captain Gillespie, and the Californians investing it numbered 300.

Finding himself overpowered, Captain Gillespie capitulated on the

30th, and thence retired with all the foreigners aboard of a sloop-of-

war, and sailed for Monterey. Lieutenant Talbot, who commanded

only nine men at Santa Barbara, refused to surrender, and marched

out with his men, arms in hand. The frigate Savannah was sent to

relieve Los Angeles, but she did not arrive till after the above events

had occurred. Her crew, numbering 320 men, landed at San Pedro

and marched to meet the Californians. About half way between San

Pedro and Los Angeles, about fifteen miles from their ship, the

sailors found the enemy drawn up on a plain. The Californians were

mounted on fine horses, and with artillery, had every advantage.

27.

The sailors wereforced to retreat with a loss of five killed and six

wounded.

Commodore Stockton came down in the Congress to San Pedro, and

then marched for the "City of the Angels," the men dragging six of

the ship's guns. At the Rancho Sepulvida, a large force of the

Californians was posted. Commodore Stockton sent one hundred

men forward to receive the fire of the enemy and then fall back

upon the main body without returning it. The main body was formed

in a triangle, with the guns hid by the men. By the retreat of the

advance party, the enemy were decoyed close to the main force,

when the wings were extended and a deadly fire opened upon the

astonished Californians. More than a hundred were killed, the same

number wounded, and their whole force routed. About a hundred

prisoners were taken, many of whom were at the time on parole and

had signed an obligation not to take up arms during the war.

Commodore Stockton soon mounted his men and prepared for

operations on shore. Skirmishes followed, and were continually

occurring until January, 1847, when a decisive action occurred.

General Kearny had arrived in California, after a long and painful

march overland, and his co-operation was of great service to

Stockton. The Americans left San Diego on the 29th of December, to

march to Los Angeles. The Californians determined to meet them on

their route, and decide the fate of the country in a general battle.

The American force amounted to six hundred men, and was

composed of detachments from the ships Congress, Savannah,

Portsmouth and Cyane, aided by General Kearny, with sixty men on

foot, from the first regiment of United States dragoons, and Captain

Gillespie with sixty mounted riflemen. The troops marched one

hundred and ten miles in ten days, and, on the 8th of January, they

found the Californians in a strong position on the high bank of the

San Gabriel river, with six hundred mounted men and four pieces of

artillery, prepared to dispute the passage of the river. The Americans

waded through the water, dragging their guns with them, exposed to

a galling fire from the enemy, without returning a shot. When they

28.

reached the oppositeshore, the Californians charged upon them, but

were driven back. They then charged up the bank and succeeded in

driving the Californians from their post. Stockton, with his force,

continued his march, and the next day, in crossing the plains of

Mesa, the enemy made another attempt to save their capital. They

were concealed with their artillery in a ravine, until the Americans

came within gun-shot, when they opened a brisk fire upon their right

flank, and at the same time charged both their front and rear. But

the guns of the Californians were soon silenced, and the charge

repelled. The Californians then fled, and the next morning the

Americans entered Los Angeles without opposition. The loss of the

Americans in killed and wounded did not exceed twenty, while that

of their opponents reached between seventy and eighty.

These two battles decided the contest in California. General Flores,

governor and commandant-general of the Californians, as he styled

himself, immediately after the Americans entered Los Angeles, made

his escape and his troops dispersed. The territory became again

tranquil, and the civil government was soon in operation again in the

places where it had been interrupted by the revolt. Commodore

Stockton and General Kearny having a misunderstanding about their

respective powers, Colonel Fremont exercised the duties of governor

and commander-in-chief of California, declining to obey the orders of

General Kearny.

The account of the adventures and skirmishes with which the small

force of United States troops under General Kearny met, while on

their march to San Diego, in Upper California, is one of the most

interesting to which the contest gave birth. The party, which

consisted of one hundred men when it started from Santa Fé,

reached Warner's rancho, the frontier settlement in California, on the

Sonoma route, on the 2d of December, 1846. They continued their

march, and on the 5th were met by a small party of volunteers,

under Captain Gillespie, sent out by Commodore Stockton to meet

them, and inform them of the revolt of the Californians. The party

encamped for the night at Stokes's rancho, about forty miles from

29.

San Diego. Informationwas received that an armed party of

Californians was at San Pasqual, three leagues from Stokes's rancho.

A party of dragoons was sent out to reconnoitre, and they returned

by two o'clock on the morning of the 6th. Their information

determined General Kearny to attack the Californians before

daylight, and arrangements were accordingly made. Captain Johnson

was given the command of an advance party of twelve dragoons,

mounted upon the best horses in possession of the party. Then

followed fifty dragoons, under Captain Moore, mounted mostly on

the tired mules they had ridden from Santa Fé—a distance of 1050

miles. Next came about twenty volunteers, under Captain Gibson.

Then followed two mountain howitzers, with dragoons to manage

them, under charge of Lieutenant Davidson. The remainder of the

dragoons and volunteers were placed under command of Major

Swords, with orders to follow on the trail with the baggage.

As the day of December 6th dawned, the enemy at San Pasqual

were seen to be already in the saddle, and Captain Johnson, with his

advance guard, made a furious charge upon them; he being

supported by the dragoons, the Californians at length gave way.

They had kept up a continual fire from the first appearance of the

dragoons, and had done considerable execution. Captain Johnson

was shot dead in his first charge. The enemy were pursued by

Captain Moore and his dragoons, and they retreated about half a

mile, when seeing an interval between the small advance party of

Captain Moore and the main force coming to his support, they rallied

their whole force, and charged with their lances. For five minutes

they held the ground, doing considerable execution, until the arrival

of the rest of the American party, when they broke and fled. The

troops of Kearny lost two captains, a lieutenant, two sergeants, two

corporals, and twelve privates. Among the wounded were General

Kearny, Lieutenant Warner, Captains Gillespie and Gibson, one

sergeant, one bugleman, and nine privates. The Californians carried

off all their wounded and dead except six.

30.

On the 7ththe march was resumed, and, near San Bernardo,

Kearny's advance encountered and defeated a small party of the

Californians who had taken post on a hill. At San Bernardo, the

troops remained till the morning of the 11th, when they were joined

by a party of sailors and marines, under Lieutenant Gray. They then

proceeded upon their march, and on the 12th, arrived at San Diego;

having thus completed a march of eleven hundred miles through an

enemy's country, with but one hundred men. The force of General

Kearny having joined that of Commodore Stockton, the expedition

against Los Angeles, of which we have given an account in this

chapter, was successfully consummated, and tranquillity restored in

California. General Kearny and Commodore Stockton returned to the

United States in January, 1847, leaving Colonel Fremont to exercise

the office of governor and military commandant of California. No

further events of an importance worth recording occurred till the

treaty of peace between the United States and Mexico.

31.

CHAPTER VI.

DISCOVERY OFTHE GOLD PLACERS.

By the treaty concluded between the United States and Mexico, in

1847, the territory of Upper California became the property of the

United States. Little thought the Mexican government of the value of

the land they were ceding, further than its commercial importance;

and, doubtless, little thought the buyers of the territory, that its soil

was pregnant with a wealth untold, and that its rivers flowed over

golden beds.

This territory, now belonging to the American Union, embraces an

area of 448,961 square miles. It extends along the Pacific coast,

from about the thirty-second parallel of north latitude, a distance of

near seven hundred miles, to the forty-second parallel, the southern

boundary of Oregon. On the east, it is bounded by New Mexico.

During the long period which transpired between its discovery and

its cession to the United States, this vast tract of country was

frequently visited by men of science, from all parts of the world.

Repeated examinations were made by learned and enterprising

officers and civilians; but none of them discovered the important

fact, that the mountain torrents of the Sierra Nevada were

constantly pouring down their golden sands into the valleys of the

Sacramento and San Joaquin. The glittering particles twinkled

beneath their feet, in the ravines which they explored, or glistened

in the watercourses which they forded, yet they passed them by

unheeded. Not a legend or tradition was heard among the white

settlers, or the aborigines, that attracted their curiosity. A nation's

ransom lay within their grasp, but, strange to say, it escaped their

notice—it flashed and sparkled all in vain.[1]

32.

The Russian AmericanCompany had a large establishment at Ross

and Bodega, ninety miles north of San Francisco, founded in the

year 1812; and factories were also established in the territory by the

Hudson Bay Company. Their agents and employes ransacked the

whole country west of the Sierra Nevada, or Snowy Mountain, in

search of game. In 1838, Captain Sutter, formerly an officer in the

Swiss Guards of Charles X., King of France, emigrated from the state

of Missouri to Upper California, and obtained from the Mexican

government a conditional grant of thirty leagues square of land,

bounded on the west by the Sacramento river. Having purchased the

stock, arms, and ammunition of the Russian establishment, he

erected a dwelling and fortification on the left bank of the

Sacramento, about fifty miles from its mouth, and near what was

termed, in allusion to the new settlers, the American Fork. This

formed the nucleus of a thriving settlement, to which Captain Sutter

gave the name of New Helvetia. It is situated at the head of

navigation for vessels on the Sacramento, in latitude 38° 33' 45"

north, and longitude 121° 20' 05" west. During a residence of ten

years in the immediate vicinity of the recently discovered placéras,

or gold regions, Captain Sutter was neither the wiser nor the richer

for the brilliant treasures that lay scattered around him.[2]

In the year 1841, careful examinations of the Bay of San Francisco,

and of the Sacramento River and its tributaries, were made by

Lieutenant Wilkes, the commander of the Exploring Expedition; and

a party under Lieutenant Emmons, of the navy, proceeded up the

valley of the Willamette, crossed the intervening highlands, and

descended the Sacramento. In 1843-4, similar examinations were

made by Captain, afterwards Lieutenant-Colonel Fremont, of the

Topographical Engineers, and in 1846, by Major Emory, of the same

corps. None of these officers made any discoveries of minerals,

although they were led to conjecture, as private individuals who had

visited the country had done, from its volcanic formation and

peculiar geological features, that they might be found to exist in

considerable quantities.[3]

33.

As is oftenthe case, chance at length accomplished what science

had failed to do. In the winter of 1847-8, a Mr. Marshall commenced

the construction of a saw-mill for Captain Sutter, on the north branch

of the American Fork, and about fifty miles above New Helvetia, in a

region abounding with pine timber. The dam and race were

completed, but on attempting to put the mill in motion, it was

ascertained that the tail-race was too narrow to permit the water to

escape with perfect freedom. A strong current was then passed in,

to wash it wider and deeper, by which a large bed of mud and gravel

was thrown up at the foot of the race. Some days after this

occurrence, Mr. Marshall observed a number of brilliant particles on

this deposit of mud, which attracted his attention. On examining

them, he became satisfied that they were gold, and communicated

the fact to Captain Sutter. It was agreed between them, that the

circumstance should not be made public for the present; but, like

the secret of Midas, it could not be concealed. The Mormon

emigrants, of whom Mr. Marshall was one, were soon made

acquainted with the discovery, and in a few weeks all California was

agitated with the startling information.

Business of every kind was neglected, and the ripened grain was left

in the fields unharvested. Nearly the whole population of Upper

California became infected with the mania, and flocked to the mines.

Whalers and merchant vessels entering the ports were abandoned

by their crews, and the American soldiers and sailors deserted in

scores. Upon the disbandment of Colonel Stevenson's regiment,

most of the men made their way to the mineral regions. Within three

months after the discovery, it was computed that there were near

four thousand persons, including Indians, who were mostly

employed by the whites, engaged in washing for gold. Various

modes were adopted to separate the metal from the sand and gravel

—some making use of tin pans, others of close-woven Indian

baskets, and others still, of a rude machine called the cradle, six or

eight feet long, and mounted on rockers, with a coarse grate, or

sieve, at one end, but open at the other. The washings were mainly

confined to the low wet grounds, and the margins of the streams—

34.

the earth beingrarely disturbed more than eighteen inches below

the surface. The value of the gold dust obtained by each man, per

day, is said to have ranged from ten to fifty dollars, and sometimes

even to have far exceeded that. The natural consequence of this

state of things was, that the price of labor, and, indeed, of every

thing, rose immediately from ten to twenty fold.[4]

As may readily be conjectured, every stream and ravine in the valley

of the Sacramento was soon explored. Gold was found on every one

of its tributaries; but the richest earth was discovered near the Rio

de los Plumas, or Feather River,[5] and its branches, the Yuba and

Bear rivers, and on Weber's creek, a tributary of the American Fork.

Explorations were also made in the valley of the San Joaquin, which

resulted in the discovery of gold on the Cosumnes and other

streams, and in the ravines of the Coast Range, west of the valley,

as far down as Ciudad de los Angeles.

In addition to the gold mines, other important discoveries were

made in Upper California. A rich vein of quicksilver was opened at

New Almaden, near Santa Clara, which, with imperfect machinery,—

the heat by which the metal is made to exude from the rock being

applied by a very rude process,—yielded over thirty per cent. This

mine—one of the principal advantages to be derived from which will

be, that the working of the silver mines scattered through the

territory must now become profitable—is superior to those of

Almaden, in Old Spain, and second only to those of Idria, near

Trieste, the richest in the world.

Lead mines were likewise discovered in the neighborhood of

Sonoma, and vast beds of iron ore near the American Fork, yielding

from eighty-five to ninety per cent. Copper, platina, tin, sulphur, zinc,

and cobalt, were discovered every where; coal was found to exist in

large quantities in the Cascade range of Oregon, of which the Sierra

Nevada is a continuation; and in the vicinity of all this mineral

wealth, there are immense quarries of marble and granite, for

building purposes.

35.

Colonel Mason hadsucceeded Colonel Fremont in the post of

governor of California and military commandant. A regiment of New

York troops, under the command of Colonel Stevenson, had been

ordered to California before the conclusion of the treaty of peace,

and formed the principal part of the military force in the territory.

Colonel Mason expressed the opinion, in his official despatch, that

"there is more gold in the country drained by the Sacramento and

San Joaquin rivers, than will pay the cost of the [late] war with

Mexico a hundred times over." Should this even prove to be an

exaggeration, there can be little reason to doubt, when we take into

consideration all the mineral resources of the country, that the

territory of California is by far the richest acquisition made by this

government since its organization.

The appearance of the mines, at the period of Governor Mason's

visit, three months after the discovery, he thus graphically describes:

"At the urgent solicitation of many gentlemen, I delayed there [at

Sutter's Fort] to participate in the first public celebration of our

national anniversary at that fort, but on the 5th resumed the

journey, and proceeded twenty-five miles up the American Fork to a

point on it now known as the Lower Mines, or Mormon Diggins. The

hill-sides were thickly strewn with canvas tents and bush arbors; a

store was erected, and several boarding shanties in operation. The

day was intensely hot, yet about two hundred men were at work in

the full glare of the sun, washing for gold—some with tin pans, some

with close-woven Indian baskets, but the greater part had a rude

machine, known as the cradle. This is on rockers, six or eight feet

long, open at the foot, and at its head has a coarse grate, or sieve;

the bottom is rounded, with small cleats nailed across. Four men are

required to work this machine; one digs the ground in the bank close

by the stream; another carries it to the cradle and empties it on the

grate; a third gives a violent rocking motion to the machine; while a

fourth dashes on water from the stream itself.

36.

"The sieve keepsthe coarse stones from entering the cradle, the

current of water washes off the earthy matter, and the gravel is

gradually carried out at the foot of the machine, leaving the gold

mixed with a heavy, fine black sand above the first cleats. The sand

and gold, mixed together, are then drawn off through auger holes

into a pan below, are dried in the sun, and afterward separated by

blowing off the sand. A party of four men thus employed at the

lower mines, averaged $100 a day. The Indians, and those who have

nothing but pans or willow baskets, gradually wash out the earth

and separate the gravel by hand, leaving nothing but the gold mixed

with sand, which is separated in the manner before described. The

gold in the lower mines is in fine bright scales, of which I send

several specimens.

"From the mill [where the gold was first discovered], Mr. Marshall

guided me up the mountain on the opposite or north bank of the

south fork, where, in the bed of small streams or ravines, now dry, a

great deal of coarse gold has been found. I there saw several parties

at work, all of whom were doing very well; a great many specimens

were shown me, some as heavy as four or five ounces in weight,

and I send three pieces, labeled No. 5, presented by a Mr. Spence.

You will perceive that some of the specimens accompanying this,

hold mechanically pieces of quartz; that the surface is rough, and

evidently moulded in the crevice of a rock. This gold cannot have

been carried far by water, but must have remained near where it

was first deposited from the rock that once bound it. I inquired of

many people if they had encountered the metal in its matrix, but in

every instance they said they had not; but that the gold was

invariably mixed with washed gravel, or lodged in the crevices of

other rocks. All bore testimony that they had found gold in greater

or less quantities in the numerous small gullies or ravines that occur

in that mountainous region.

"On the 7th of July I left the mill, and crossed to a stream emptying

into the American Fork, three or four miles below the saw-mill. I

struck this stream (now known as Weber's creek) at the washings of

37.

Sunol and Co.They had about thirty Indians employed, whom they

payed in merchandise. They were getting gold of a character similar

to that found in the main fork, and doubtless in sufficient quantities

to satisfy them. I send you a small specimen, presented by this

company, of their gold. From this point, we proceeded up the stream

about eight miles, where we found a great many people and Indians

—some engaged in the bed of the stream, and others in the small

side valleys that put into it. These latter are exceedingly rich, and

two ounces were considered an ordinary yield for a day's work. A

small gutter not more than a hundred yards long, by four feet wide

and two or three feet deep, was pointed out to me as the one where

two men—William Daly and Parry McCoon—had, a short time before,

obtained $17,000 worth of gold. Captain Weber informed me that he

knew that these two men had employed four white men and about a

hundred Indians, and that, at the end of one week's work, they paid

off their party, and had left $10,000 worth of this gold. Another

small ravine was shown me, from which had been taken upward of

$12,000 worth of gold. Hundreds of similar ravines, to all

appearances, are as yet untouched. I could not have credited these

reports, had I not seen, in the abundance of the precious metal,

evidence of their truth.

"Mr. Neligh, an agent of Commodore Stockton, had been at work

about three weeks in the neighborhood, and showed me, in bags

and bottles, over $2000 worth of gold; and Mr. Lyman, a gentleman

of education, and worthy of every credit, said he had been engaged,

with four others, with a machine, on the American Fork, just below

Sutter's mill; that they worked eight days, and that his share was at

the rate of fifty dollars a day; but hearing that others were doing

better at Weber's place, they had removed there, and were then on

the point of resuming operations. I might tell of hundreds of similar

instances; but, to illustrate how plentiful the gold was in the pockets

of common laborers, I will mention a single occurrence which took

place in my presence when I was at Weber's store. This store was

nothing but an arbor of bushes, under which he had exposed for

sale goods and groceries suited to his customers. A man came in,

38.

picked up abox of Seidlitz powders, and asked the price. Captain

Weber told him it was not for sale. The man offered an ounce of

gold, but Captain Weber told him it only cost fifty cents, and he did

not wish to sell it. The man then offered an ounce and a half, when

Captain Weber had to take it. The prices of all things are high, and

yet Indians, who before hardly knew what a breech cloth was, can

now afford to buy the most gaudy dresses.

"The country on either side of Weber's creek is much broken up by

hills, and is intersected in every direction by small streams or

ravines, which contain more or less gold. Those that have been

worked are barely scratched; and although thousands of ounces

have been carried away, I do not consider that a serious impression

has been made upon the whole. Every day was developing new and

richer deposits; and the only impression seemed to be, that the

metal would be found in such abundance as seriously to depreciate

in value.

"On the 8th of July, I returned to the lower mines, and on the

following day to Sutter's, where, on the 19th, I was making

preparations for a visit to the Feather, Yuba, and Bear Rivers, when I

received a letter from Commander A. R. Long, United States Navy,

who had just arrived at San Francisco from Mazatlan with a crew for

the sloop-of-war Warren, with orders to take that vessel to the

squadron at La Paz. Captain Long wrote to me that the Mexican

Congress had adjourned without ratifying the treaty of peace, that

he had letters from Commodore Jones, and that his orders were to

sail with the Warren on or before the 20th of July. In consequence of

these, I determined to return to Monterey, and accordingly arrived

here on the 17th of July. Before leaving Sutter's, I satisfied myself

that gold existed in the bed of the Feather River, in the Yuba and

Bear, and in many of the smaller streams that lie between the latter

and the American Fork; also, that it had been found in the

Cosumnes to the south of the American Fork. In each of these

streams the gold is found in small scales, whereas in the intervening

mountains it occurs in coarser lumps.

39.

"Mr. Sinclair, whoserancho is three miles above Sutter's, on the

north side of the American, employs about fifty Indians on the north

fork, not far from its junction with the main stream. He had been

engaged about five weeks when I saw him, and up to that time his

Indians had used simply closely woven willow baskets. His net

proceeds (which I saw) were about $16,000 worth of gold. He

showed me the proceeds of his last week's work—fourteen pounds

avoirdupois of clean-washed gold.

"The principal store at Sutter's Fort, that of Brannan and Co., had

received in payment for goods $36,000 (worth of this gold) from the

1st of May to the 10th of July. Other merchants had also made

extensive sales. Large quantities of goods were daily sent forward to

the mines, as the Indians, heretofore so poor and degraded, have

suddenly become consumers of the luxuries of life. I before

mentioned that the greater part of the farmers and rancheros had

abandoned their fields to go to the mines. This is not the case with

Captain Sutter, who was carefully gathering his wheat, estimated at

40,000 bushels. Flour is already worth at Sutter's thirty-six dollars a

barrel, and soon will be fifty. Unless large quantities of breadstuffs

reach the country, much suffering will occur; but as each man is now

able to pay a large price, it is believed the merchants will bring from

Chili and Oregon a plentiful supply for the coming winter.

"The most moderate estimate I could obtain from men acquainted

with the subject, was, that upward of four thousand men were

working in the gold district, of whom more than one-half were

Indians; and that from $30,000 to $50,000 worth of gold, if not

more, was daily obtained. The entire gold district, with very few

exceptions of grants made some years ago by the Mexican

authorities, is on land belonging to the United States. It was a

matter of serious reflection with me, how I could secure to the

government certain rents or fees for the privilege of procuring this

gold; but upon considering the large extent of country, the character

of the people engaged, and the small scattered force at my

command, I resolved not to interfere, but to permit all to work

40.