Downloaded 10 times

![ASSET CLASS 2013ASSET CLASS 2013 2221

Infrastructure seems to be a logical

place for pension funds to look for

investments that help them reach their

funding goals. What’s the problem?

The logic for pension fund investment in

infrastructure is sound: pension funds need

low risk, long dated inflation-linked cash flows.

They always have, they always will. Happily,

the UK needs new infrastructure, much of the

funding for which is long-dated and inflation-

linked. Banks, which previously funded these

endeavours, are no longer funding them, and

pension funds seem to be the natural rebound

relationship that might just turn steady.

But the spanner in the works is the human

element: players from two vastly different

industries, pensions and infrastructure, are

clearly still circling each other, scoping each

other out. Each side needs to understand

how the other thinks and operates, and

how they are motivated. At dinners set up

by Eversheds and Pinsent Masons to facilitate

the budding romance, I’ve certainly noticed from

the dynamic of the room that infrastructure

players are from Mars, while pensions people are

from Venus.

What needs to happen for pension

funds to start taking advantage of

infrastructure opportunities routinely?

The way forward to a successful partnership and

an opening-up of lucrative opportunities is three

fold.

First, opportunities and risks in this space must

be clearly understood: for the infrastructure

industry, the challenge is to communicate these

in a way that pensions people can understand.

Equally, the pensions industry must meet them

half way and step outside their comfort zones to

explore the possibilities and allow themselves to

be educated.

Second, it is necessary to achieve clarity on how

investment decisions are made in practice to

allocate to infrastructure: how can the pension

fund change its strategic asset allocation to

accommodate these new opportunities, and

what are the implementation and governance

requirements? How should a pension fund

investment committee, investment consultant

and fund manager work together in making

these new ventures happen?

Third, the nature of the infrastructure beast

is temporality: if pension funds are to capture

these attractive opportunities they must be agile,

requiring an advanced governance structure

and a clear framework for making investment

decisions.

You have facilitated deals in this space,

though. What’s the future?

All in all, the recent successful transactions in

this arena prove that the relationship between

pension funds and infrastructure might just

flourish: when infrastructure players, fund

managers and investment consultants can

communicate the opportunity effectively to

pension funds, and when pension funds have the

vital governance and decision-making structures

in place, these transactions could form a new

method by which pension funds can both build

their hedge and achieve the returns they need to

reach their funding goals.

The key for pension funds, then, is to get

ready for the date: get a Pensions Risk

Management Framework in place, understand

the opportunities in infrastructure so you can

spot the difference between a frog and a prince,

and make sure your governance framework is up

to scratch so that, when the time comes, you’re

able to make decisions while the opportunity still

exists.

Otherwise, you might just be stood up…

Swiss Re will invest $500m to infrastructure

debt, joining AllianzGI and Metlife. If the

insurance industry gets to grips with these

infrastructure opportunities sooner, pensions

might find themselves without a date. And sadly,

there aren’t plenty of “inflation-linked return-

providing” fish in the sea.

When we first introduced the asset

class in 2011 opportunities

were scarce and investors were mainly

limited to investing in infrastructure

equity,

but opportunities to access the

debt part of the capital structure have

become more plentiful in recent times

because of the limited ability

of banks to provide longer term funding

for infrastructure projects.

Basel III regulatory changes, as well as the

disappearance of the insurance wrapper market

and the ongoing economic challenges have all

put constraints on the ability of banks to provide

term financing for these projects, and provided

an opportunity for institutional investors to

access these attractive assets. Senior secured

debt, for example, can offer an appealing

illiquidity premium, as well as a historically low

default risk and high recovery rates (as a result

of covenants and other investor protections) and,

happily, liability matching characteristics to boot.

The overall challenge, though, remains how to

access these investments in practice. However,

the market has evolved dramatically over the

last few years and a number of new players have

entered the market offering investors access to

both primary and secondary debt opportunities.

Nonethless infrastructure can involve complex

structures and requires specific execution

capabilities that are not always easy to find.

Infrastructue Today:

An Update

Infrastructure still offers an opportunity to

pension funds, but the universe has shrunk as

a result of recent improvements in the banking

sector that mean the pressure to sell secondary

loans at any level has dissipated, and prices

have risen. The recent credit spread rally has

impacted the majority of credit based asset

classes. However, some opportunities remain

attractive, and they are the ones that centre on

institutional provision of the longer term capital

banks are no longer willing to provide. This may,

however, require pension funds to take exposure

to greenfield projects that will be subject to

construction and/or development risk, which

trustees need to understand and get comfortable

with.

The good news is that, recently, a number of

asset managers have come to market offering

senior infrastructure debt products for the first

time, demonstrating a real interest to make

these assets more accessible to pension funds.

The downside, though, is that many of these

products seem to provide a mix of secondary and

primary deals, as well as an uncertain quantum

of construction risk, which is not necessarily

attractive or suitable for all pension funds. Three

asset managers in particular, Macquarie, MetLife

and Allianz Global Investors, seem to have gained

traction in this space, and a number of others

are hot on their heels.

The Opportunities

Infrastructure opportunities can be compared

with traditional asset classes. They show, in

particular, a significant illiquidity premium as well

as attractive risk characteristics (as a result of

their senior secured nature which makes them

arguably safer than most corporate bonds.)

The first opportunity allows a pension fund to

gain exposure to the UK core infrastructure

sector. Co-investors are sometimes sought out

to provide long-term financing to the UK Core

Infrastructure sector via private placement; so

opportunities exist for pension funds to co-invest

alongside a manager to invest in debt secured

on existing operational infrastructure with the

potential for explicit RPI linkage.

Target gross returns are around

LIBOR + 240-260bps.

The second, if an amenable and motivated seller

can be found, allows a pension fund to purchase

an existing diversified portfolio of secondary

UK availability-based PFI loans, arranged and

managed by an asset manager. Risk-adjusted

returns are attractive relative to corporate debt,

and average credit quality is currently high BBB/

low A. The weighted average life of these assets

is typically over

15 years, and the weighted average maturity

in excess of 22 years.

Full details of current opportunities

in Illiquid Credit here.

Infrastructure

STEP

6

The key for pension funds,

then, is to get ready for the

date: get a Pensions Risk

Management Framework in

place... Otherwise, you might

just be stood up…

Revisit

With Rob Gardner: Infrastructure

and Pensions – Making the Relationship WorkQA

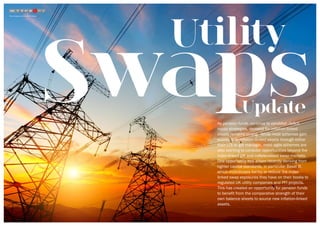

Corporate Bonds PFI Loans Core Infrastructure Loans

Issuer Corporates (all sectors) Project Company / SPV (Local Authority) Corporates (Core Infrastructure)

Cashflow Profile

Contractual, nominal cash flows

(occasionally index-linked)

Similar but loans amortize over time

Similar but loans amortize over time.

Can be index-linked

Security Capital Unsecured Secured Secured

Maturity Between 1to 35 years (typically 10yrs) Typically +20 years Typically +20 years

Valuation

If available banker/broker price quote

If not available priced using discounted cash flow

analysis, calibrated using corporate transactions

If available banker/broker price quote

If not available priced using discounted

cash flow analysis, calibrated using corporate

transactions

If available banker/broker price quote

If not available priced using discounted

cash flow analysis, calibrated using

corporate transactions

Liquidity Medium / Low Low Low

Route 1. Private Placement / Refinancing Route 2 Secondary Loans

Opportunities for pension schemes to provide direct financing to

UK Core Infrastructure borrowers and/or refinance existing loans

Estimated Gross Returns: LIBOR = [240-260] bps

Opportunities for pensions schemes to purchase secondary

infrastructure loans from banks)both PFI and Core Infrastructure)

Estimated Gross Return: LIBOR + [260-285] bps

With regard to secondary opportunities (i.e. with no construction risk), two routes

in particular provide pension funds with attractive risk/return characteristics:](https://image.slidesharecdn.com/11assetclass2013-130703060859-phpapp02/85/Asset-Class-Spring-Summer-Collection-2013-13-320.jpg)

This document discusses how pension funds and insurance companies need to access innovative investment ideas in order to meet their funding goals in the current challenging financial environment. The author's investment consultants identify the best ideas in the market, help develop them for clients' needs, and deliver them to clients. The publication, called Asset Class, aims to provide clients with the latest cutting-edge investment strategies and ideas being used or considered by other pension funds and insurance companies. It is organized according to the "7 Steps to Full Funding" framework to help clients make intelligent investment decisions and achieve strong results.