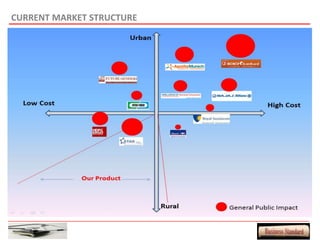

This document provides an overview of a proposed health insurance plan targeted at rural and semi-urban populations in India. The plan would offer health insurance for Rs. 2 per day per person, covering all medical expenses without hidden clauses. It aims to make quality healthcare accessible to all regardless of financial status. The target market is people in rural and semi-urban areas with a monthly family income above Rs. 3000 who are currently not covered by other insurance plans. The proposed plan would use the law of large numbers to provide high quality coverage at an affordable price through standardized treatments and a streamlined claims process.