Download to read offline

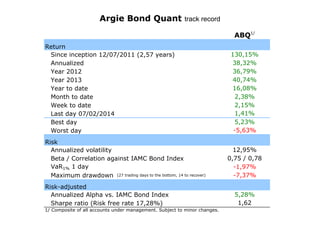

The document presents a performance summary of an investment strategy called Argie Bond Quant since its inception on December 7, 2011. It outlines annualized returns, risk metrics, and maximum drawdown data, showing significant volatility and recovery timelines. The performance metrics indicate varying returns across years, with specific details on best and worst days, along with risk-adjusted measures.