Argie bond quant portfolio track record

•

0 likes•75 views

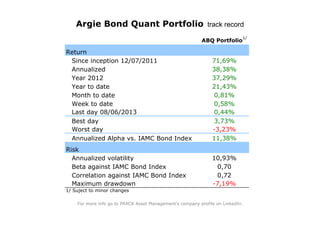

This document summarizes the performance of the ABQ Portfolio, a quantitative bond portfolio, since its inception on December 7, 2011. It provides annualized and year-to-date returns, along with various risk metrics like annualized volatility, beta, correlation, and maximum drawdown compared to an index. For more information, it directs the reader to PRACK Asset Management's LinkedIn profile.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

More from Francisco Prack

More from Francisco Prack (20)

Argie bond quant portfolio track record

- 1. Return Since inception 12/07/2011 Annualized Year 2012 Year to date Month to date Week to date Last day 08/06/2013 Best day Worst day Annualized Alpha vs. IAMC Bond Index Risk Annualized volatility Beta against IAMC Bond Index Correlation against IAMC Bond Index Maximum drawdown 1/ Suject to minor changes ABQ Portfolio 1/ 71,69% 0,81% 0,58% 38,38% 21,43% 37,29% -3,23% 0,44% 3,73% 11,38% 10,93% 0,70 -7,19% 0,72 Argie Bond Quant Portfolio track record For more info go to PRACK Asset Management's company profile on LinkedIn.

- 2. Daily data Inception date 12/07/2011 =1 Argie Bond Quant Portfolio track record 0,90 1,00 1,10 1,20 1,30 1,40 1,50 1,60 1,70 1,80 D 2011 J 2012 F M A M J J A S O N D J 2013 F M A M J J A Maximum drawdown Recovery ABQ Portfolio