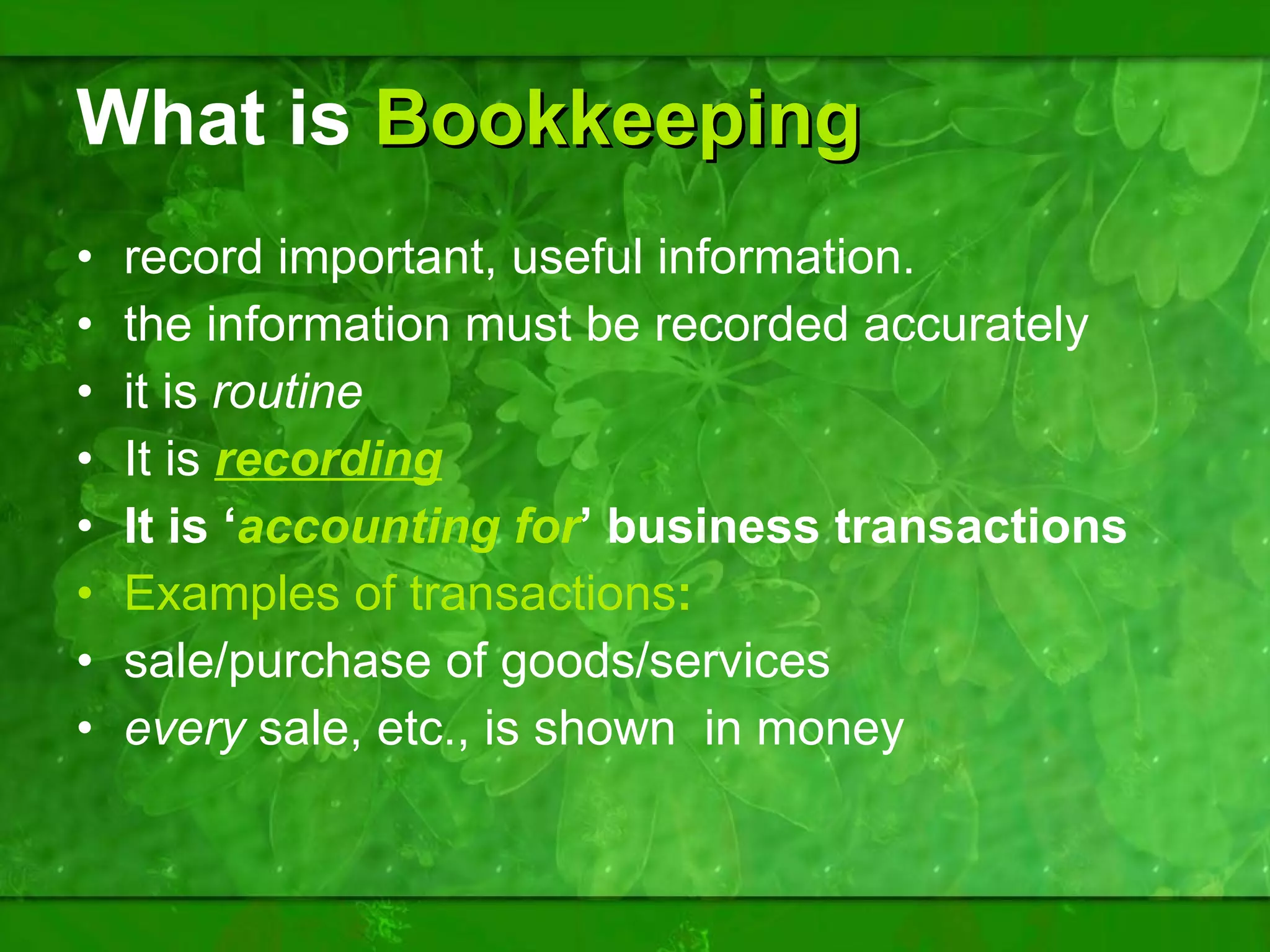

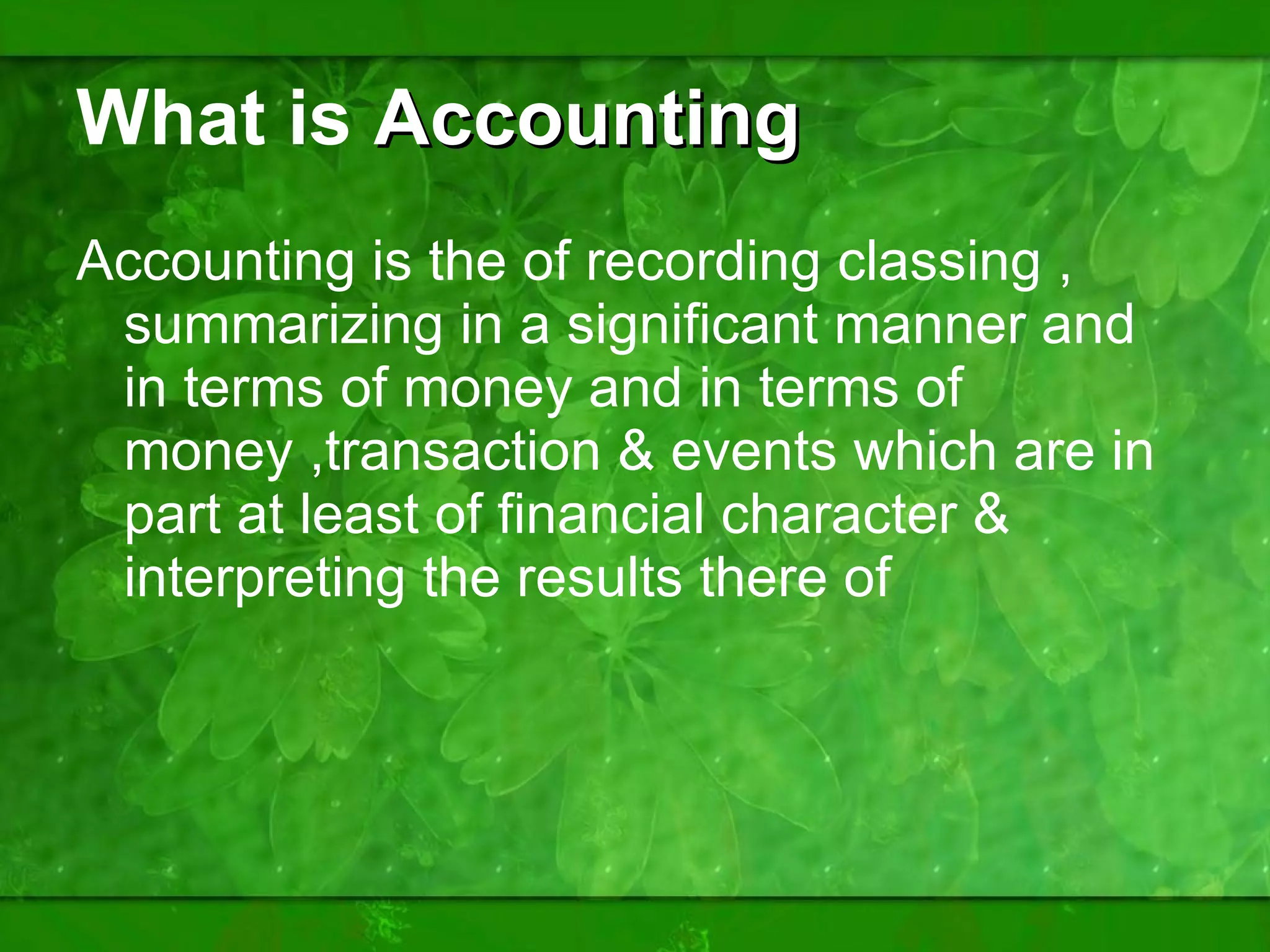

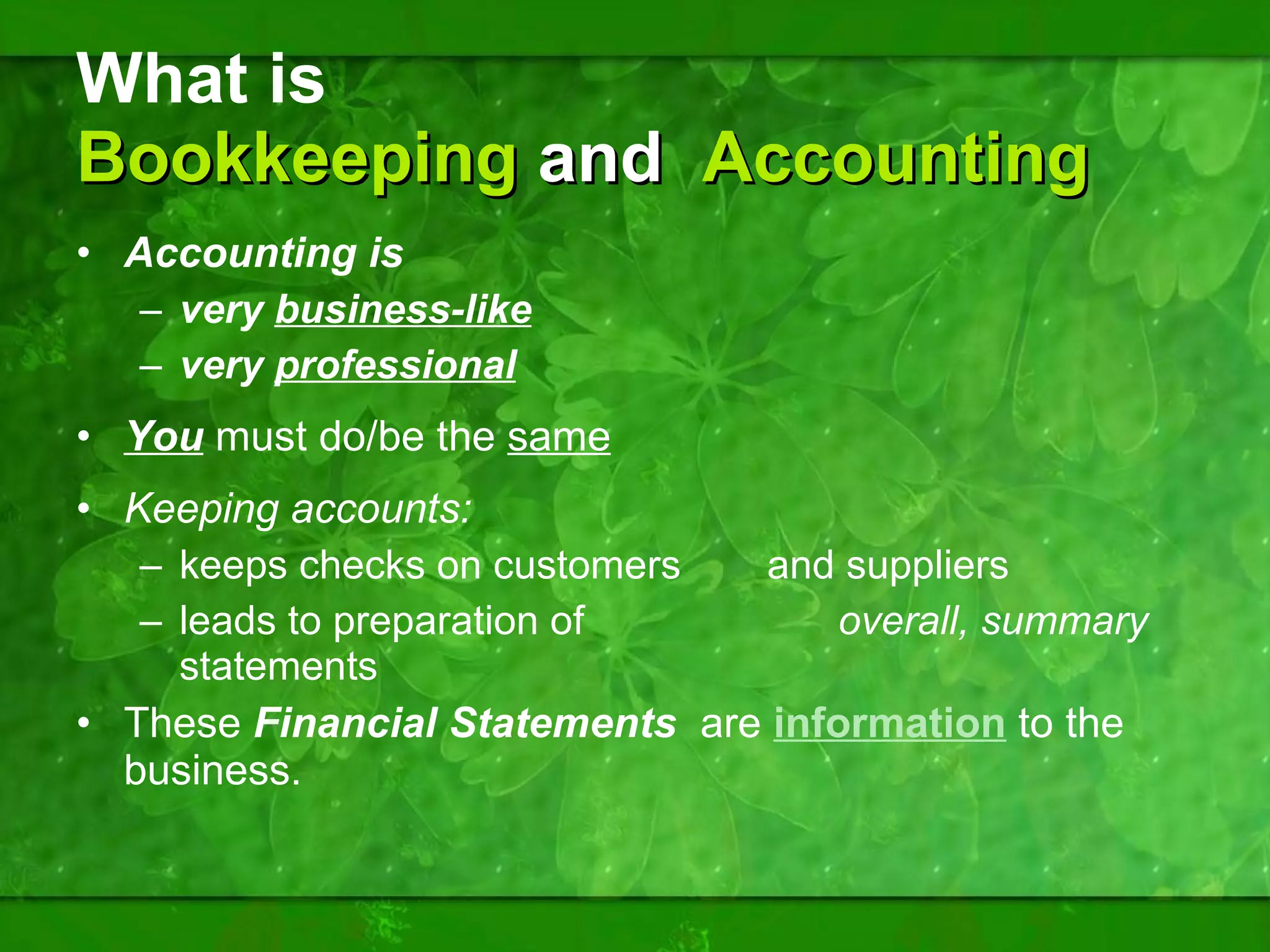

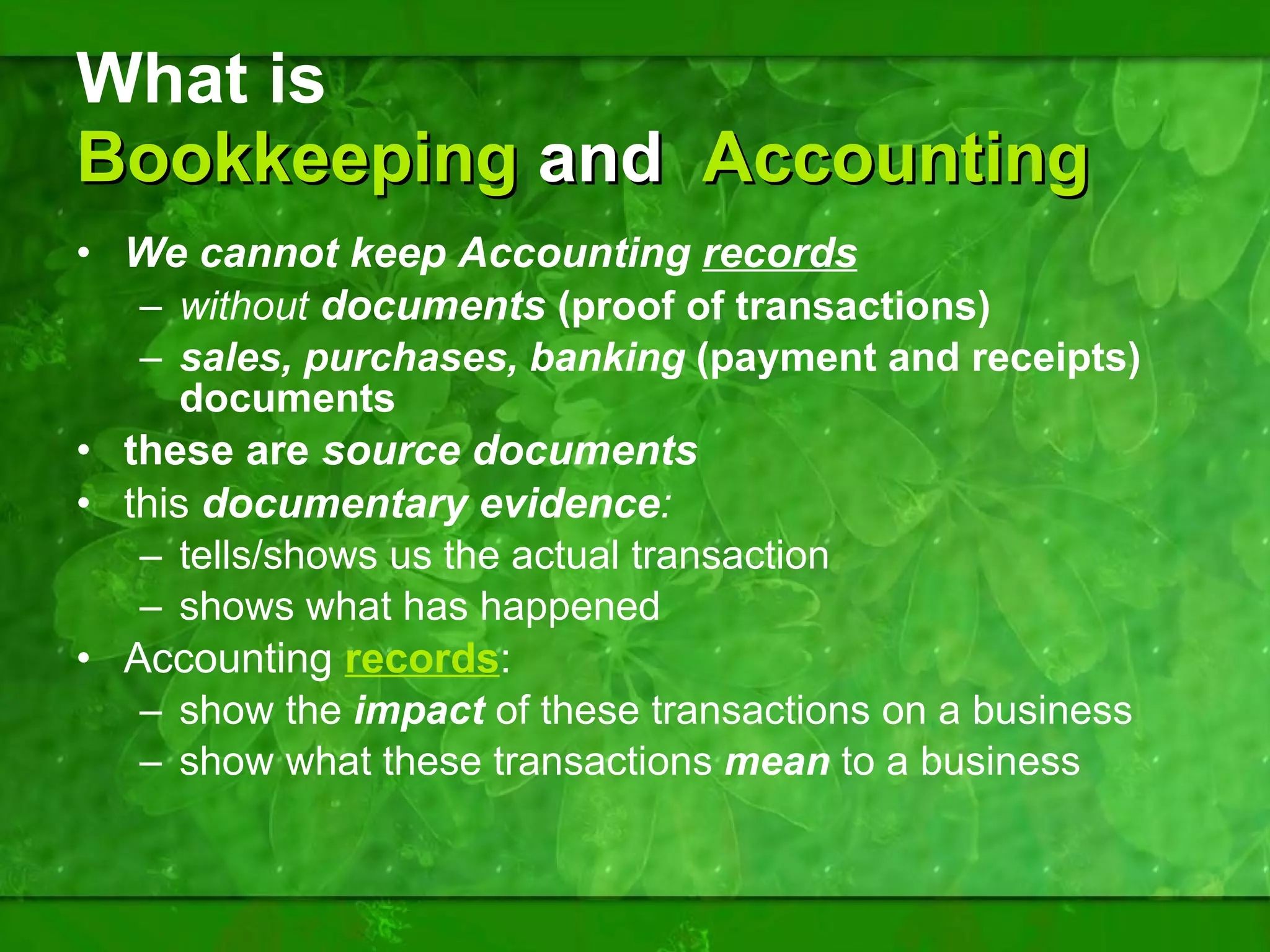

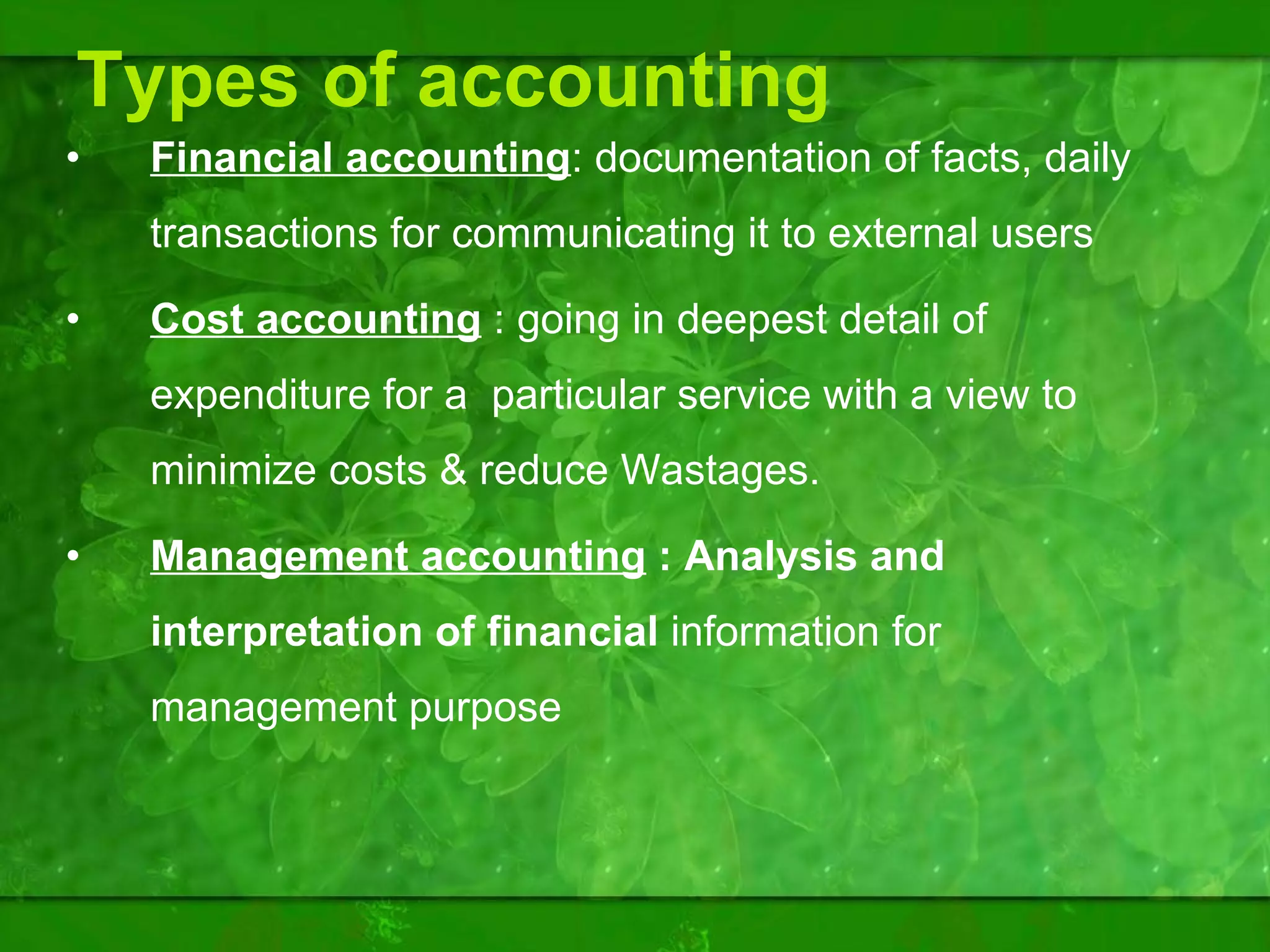

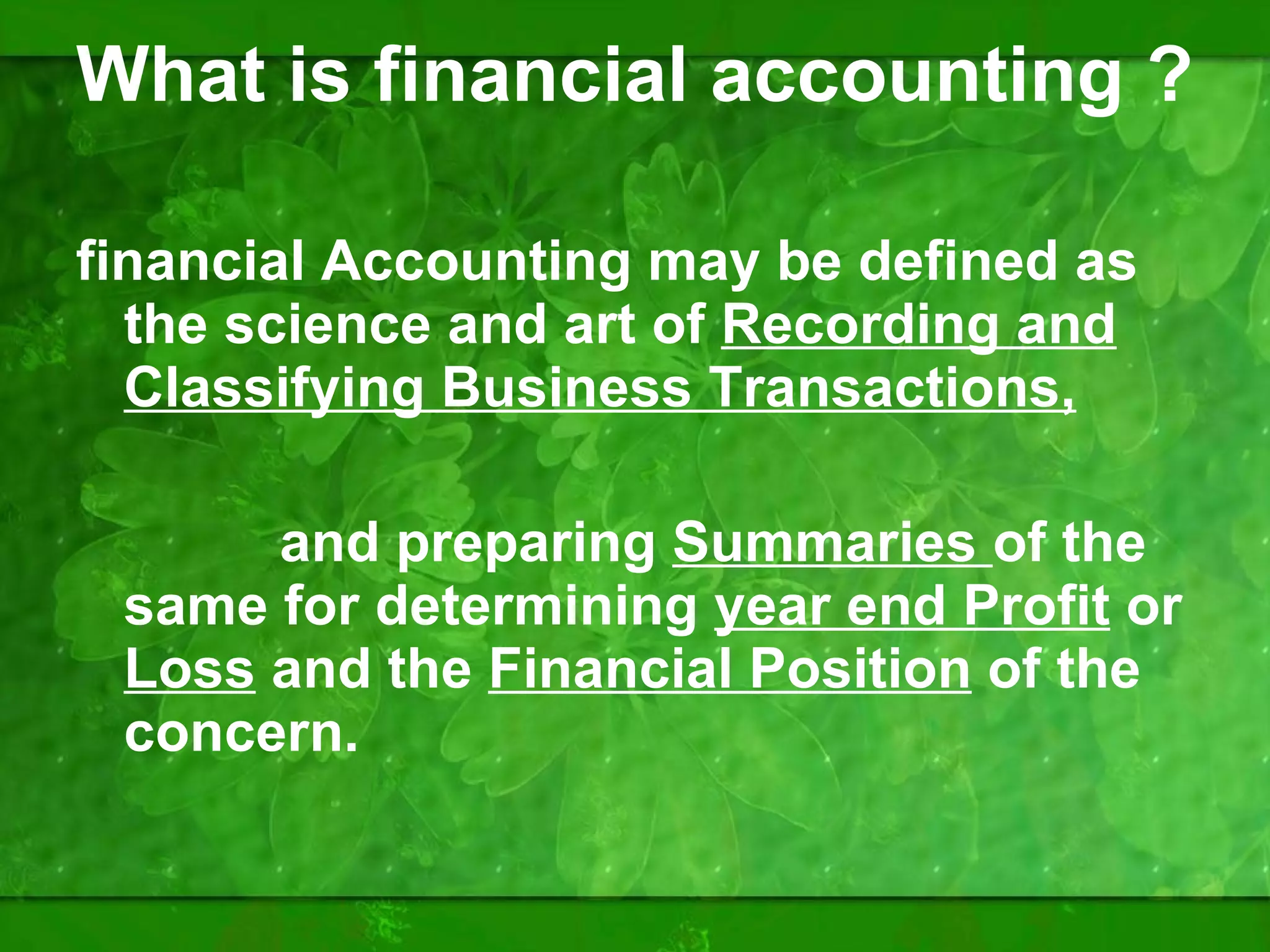

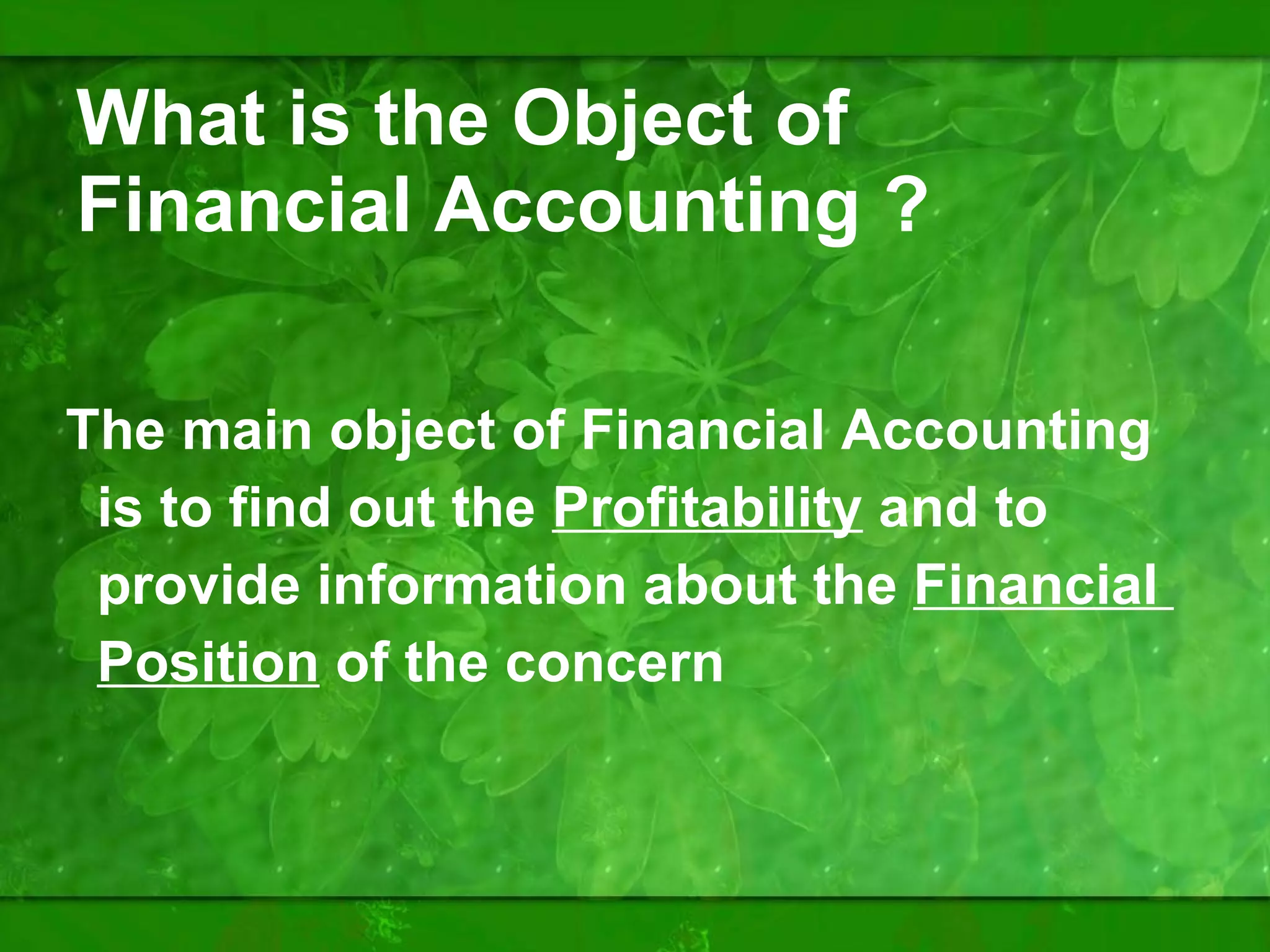

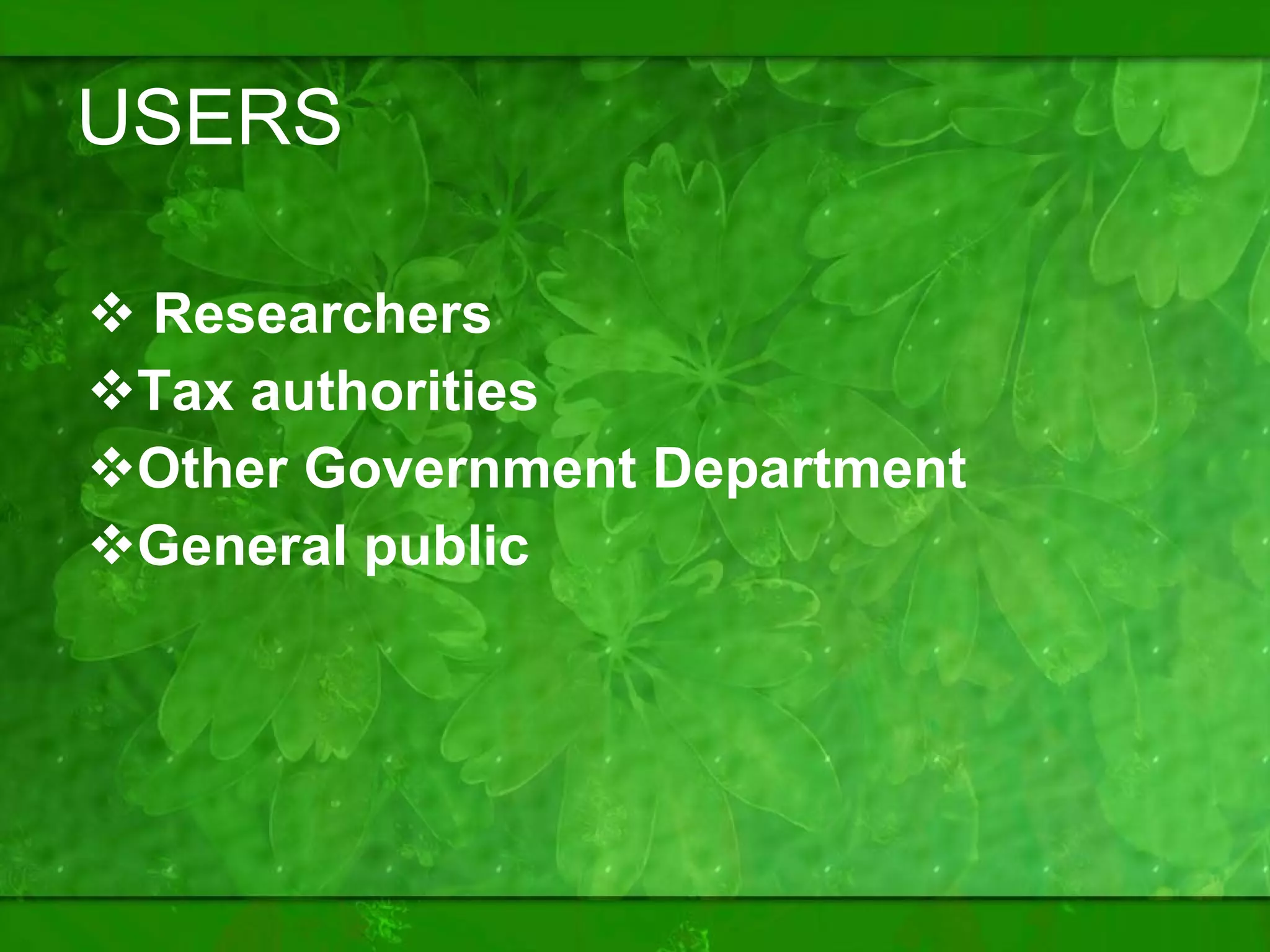

Bookkeeping involves routinely recording business transactions, while accounting analyzes a business's financial performance and position. Bookkeeping keeps track of money in and out, like a person's birthday money. Accounting examines the impact of transactions through financial statements. Both require documenting proof of transactions for accuracy and to prevent fraud. Accounting has various types including financial, cost, and management accounting that serve different purposes like external reporting, cost analysis, and internal decision making.

![Project mgmt. & entrepenuership[1]](https://cdn.slidesharecdn.com/ss_thumbnails/projectmgmt-entrepenuership1-110129111354-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)