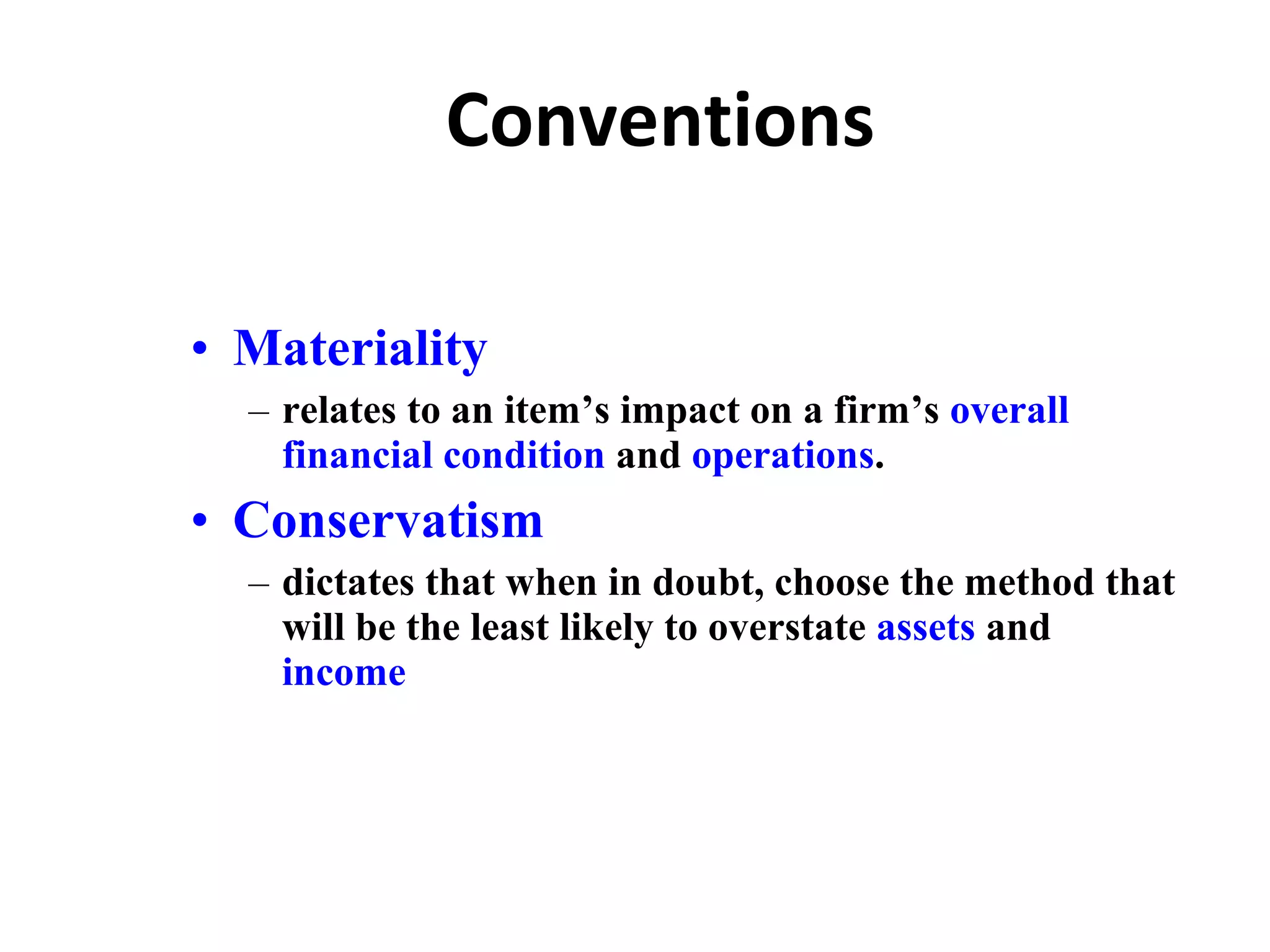

The document outlines several key accounting concepts:

1) The going concern concept assumes a company will continue operating to achieve its objectives, affecting depreciation and asset valuation.

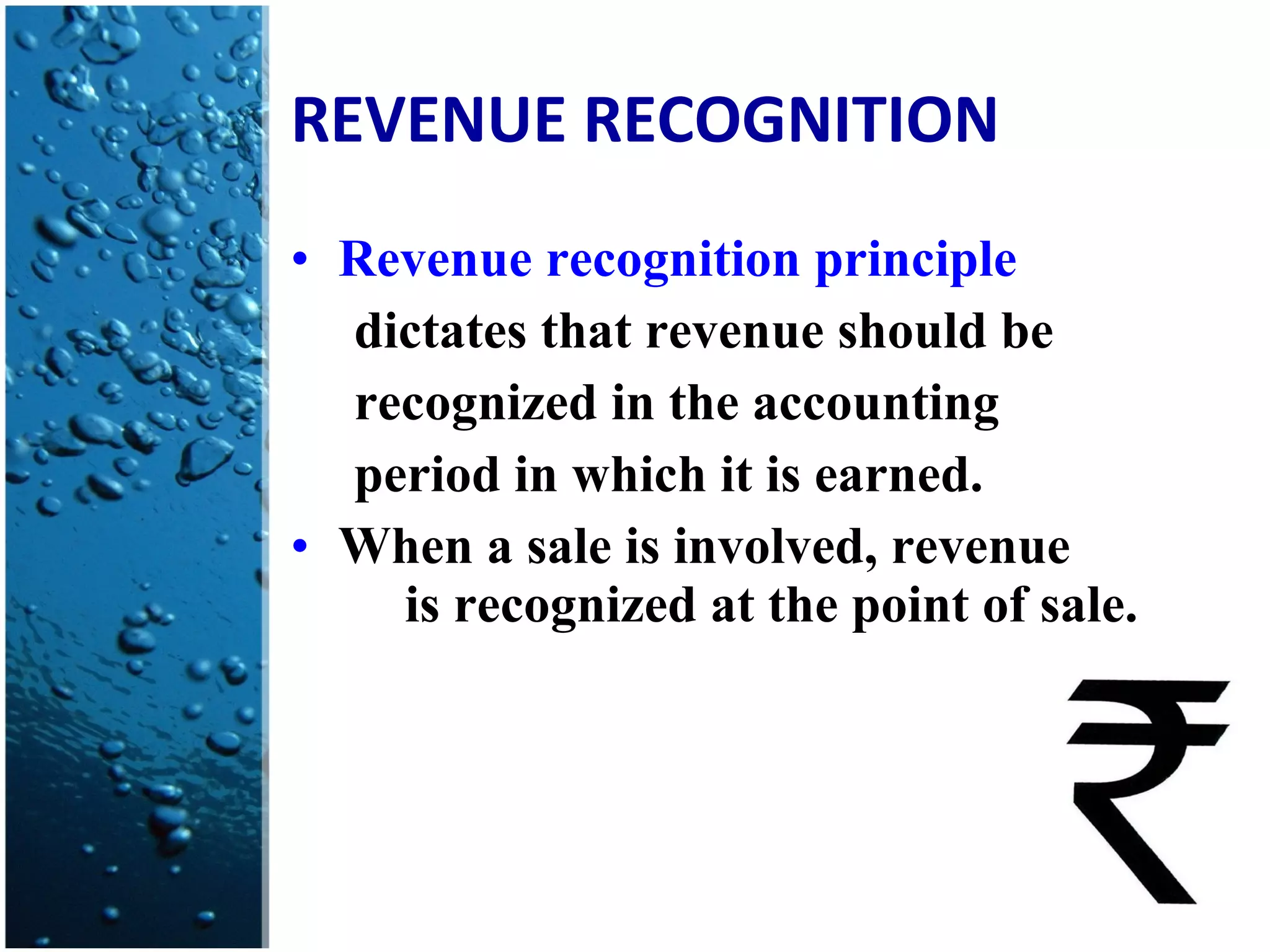

2) The revenue recognition principle states revenue should be recognized when earned, usually at the point of sale.

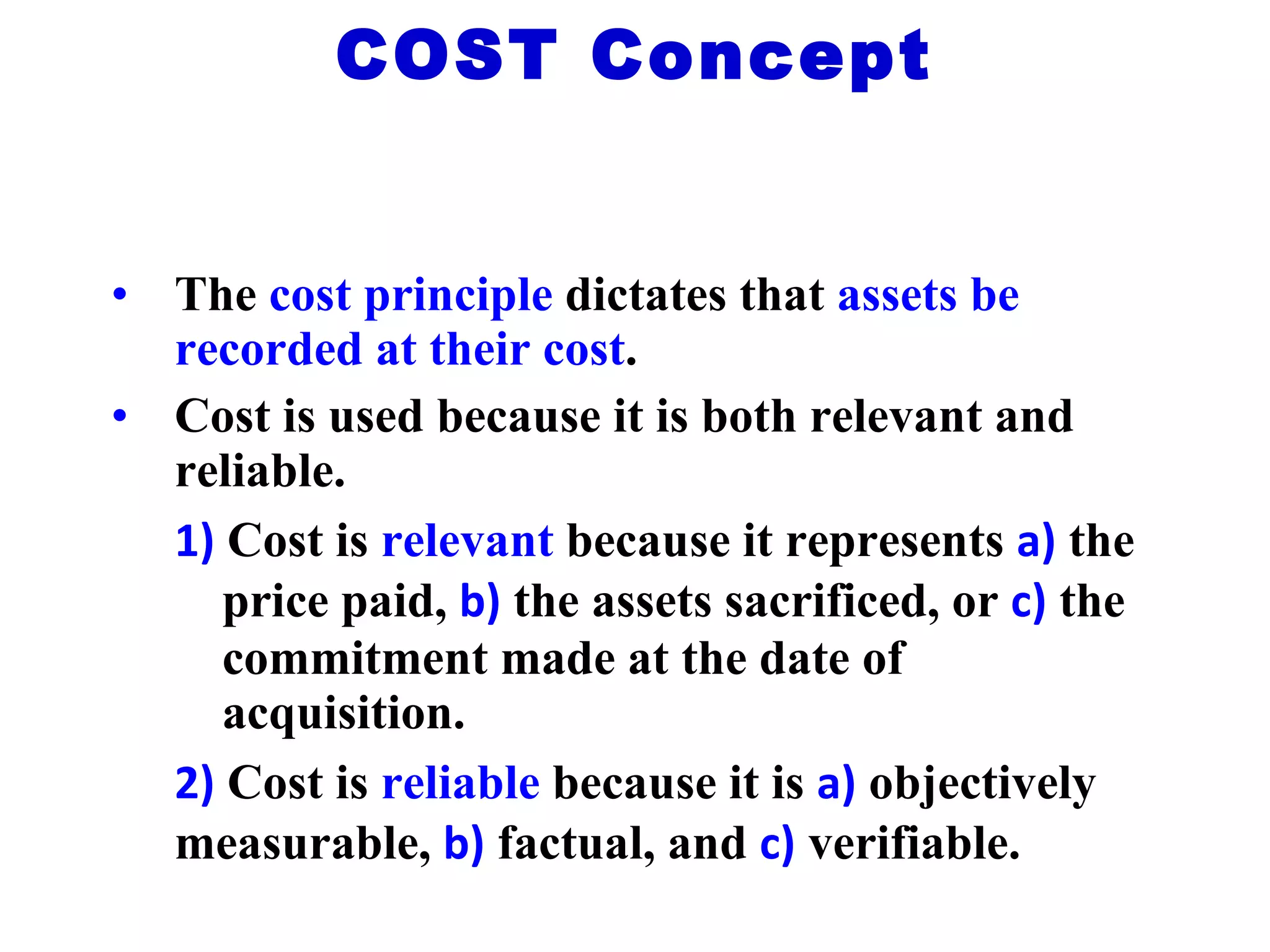

3) The cost principle dictates assets be recorded at cost, which is relevant and reliable.

![Project mgmt. & entrepenuership[1]](https://cdn.slidesharecdn.com/ss_thumbnails/projectmgmt-entrepenuership1-110129111354-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)