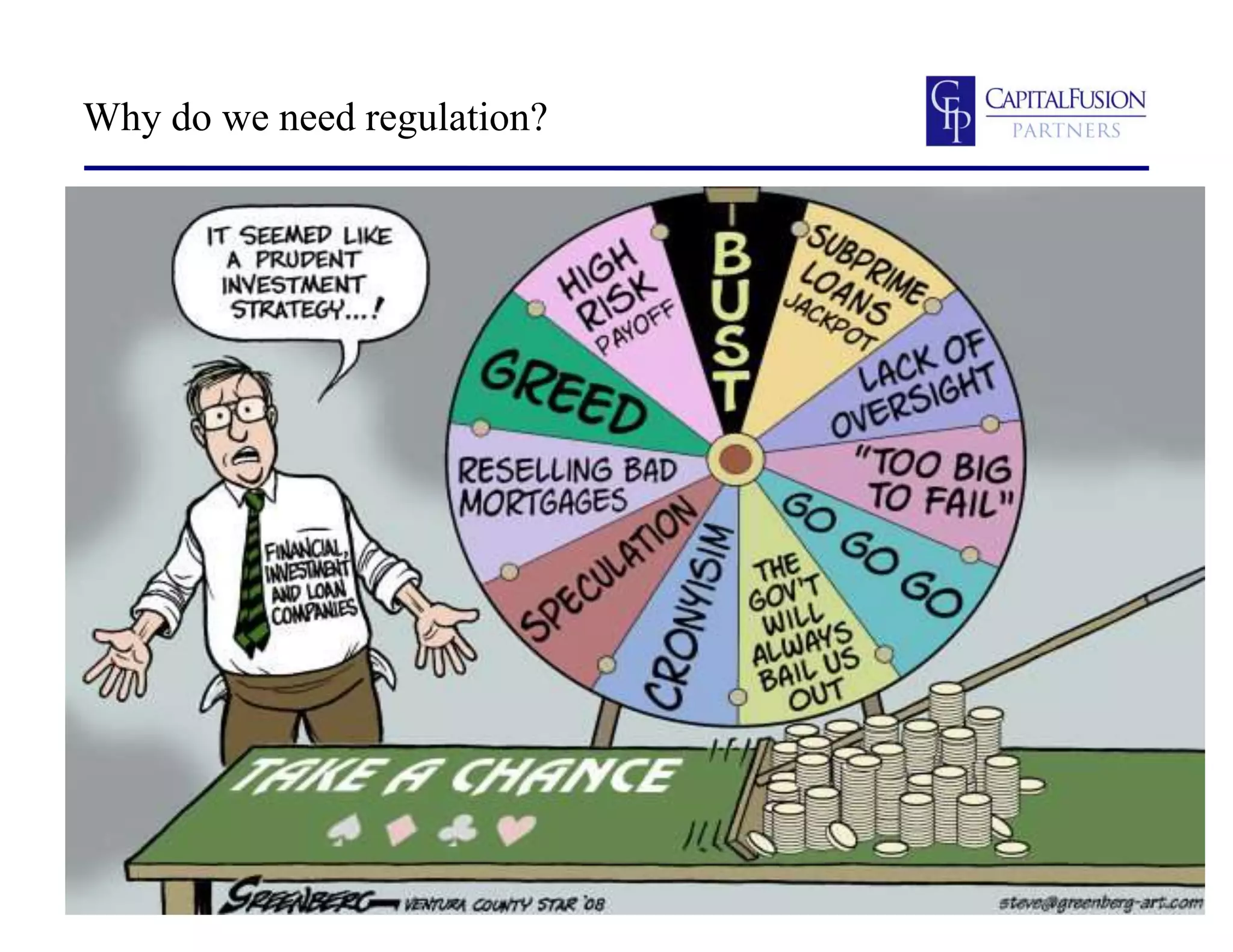

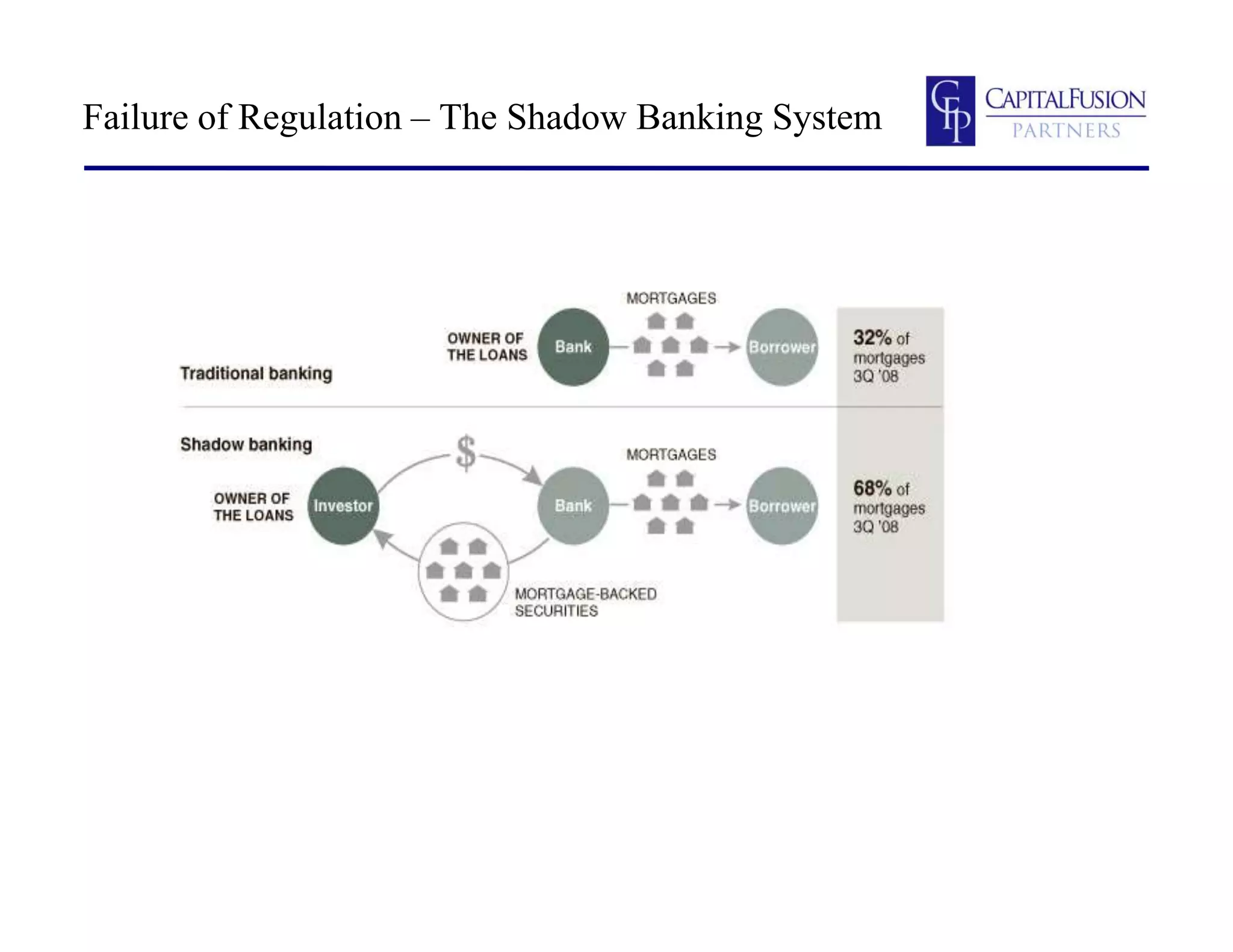

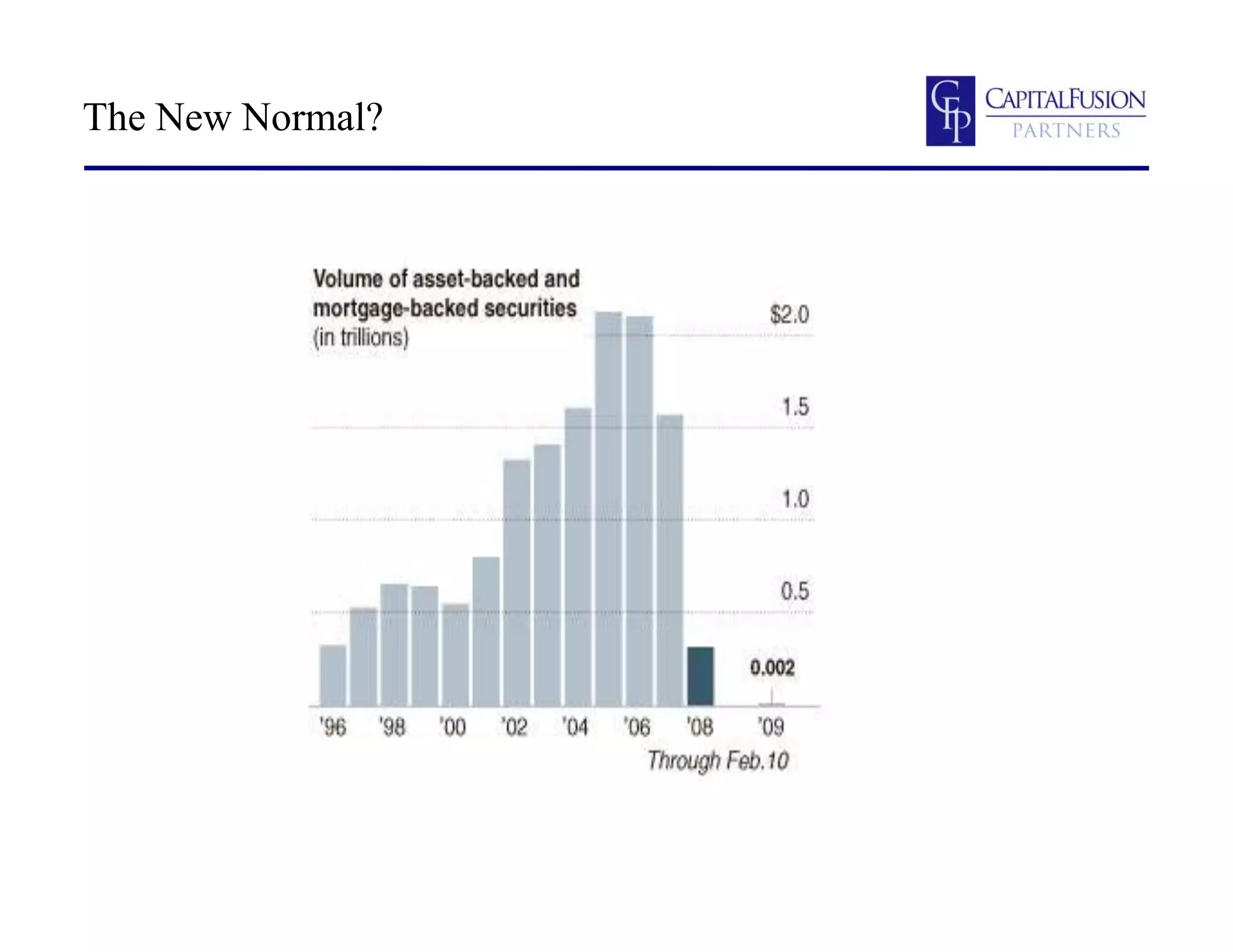

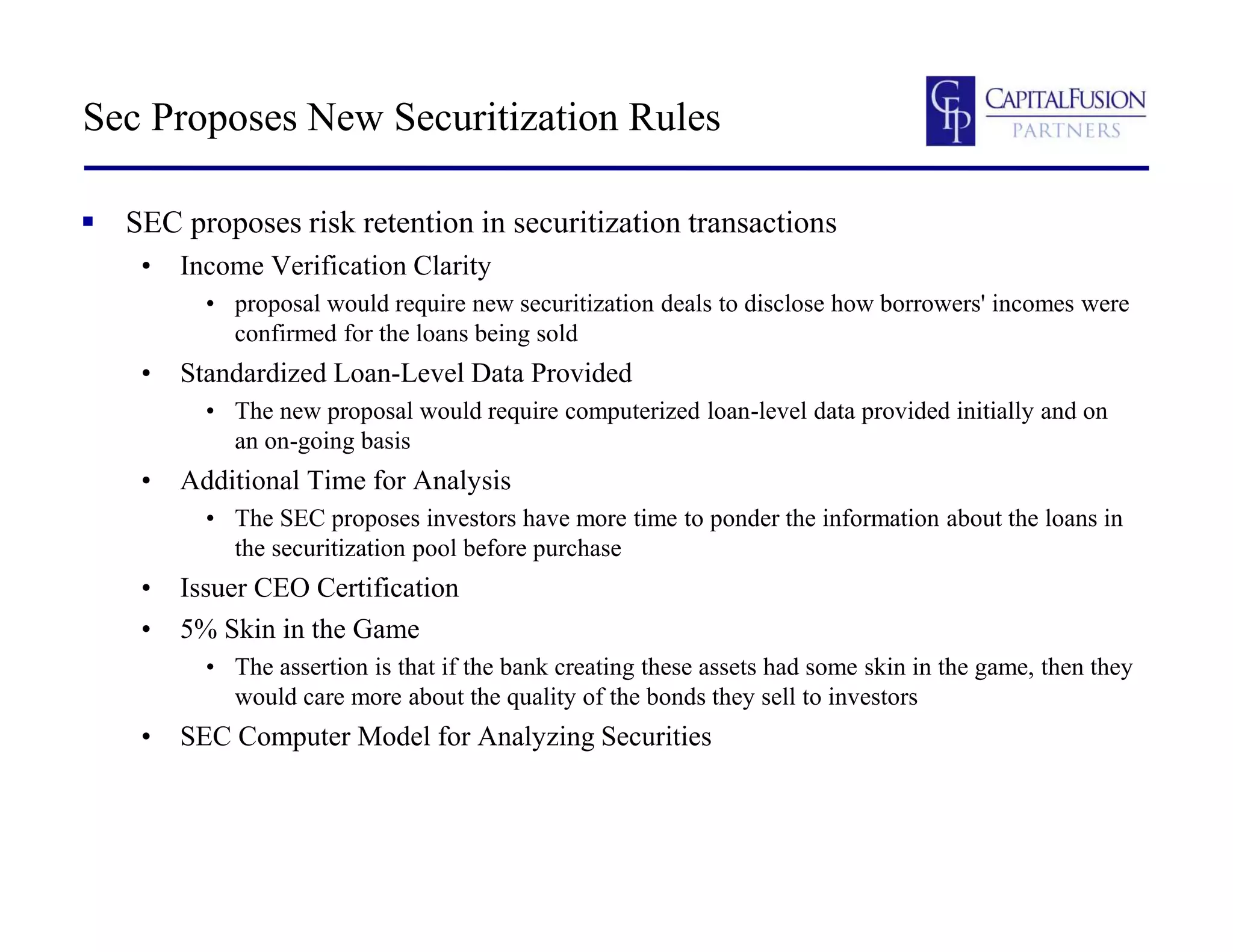

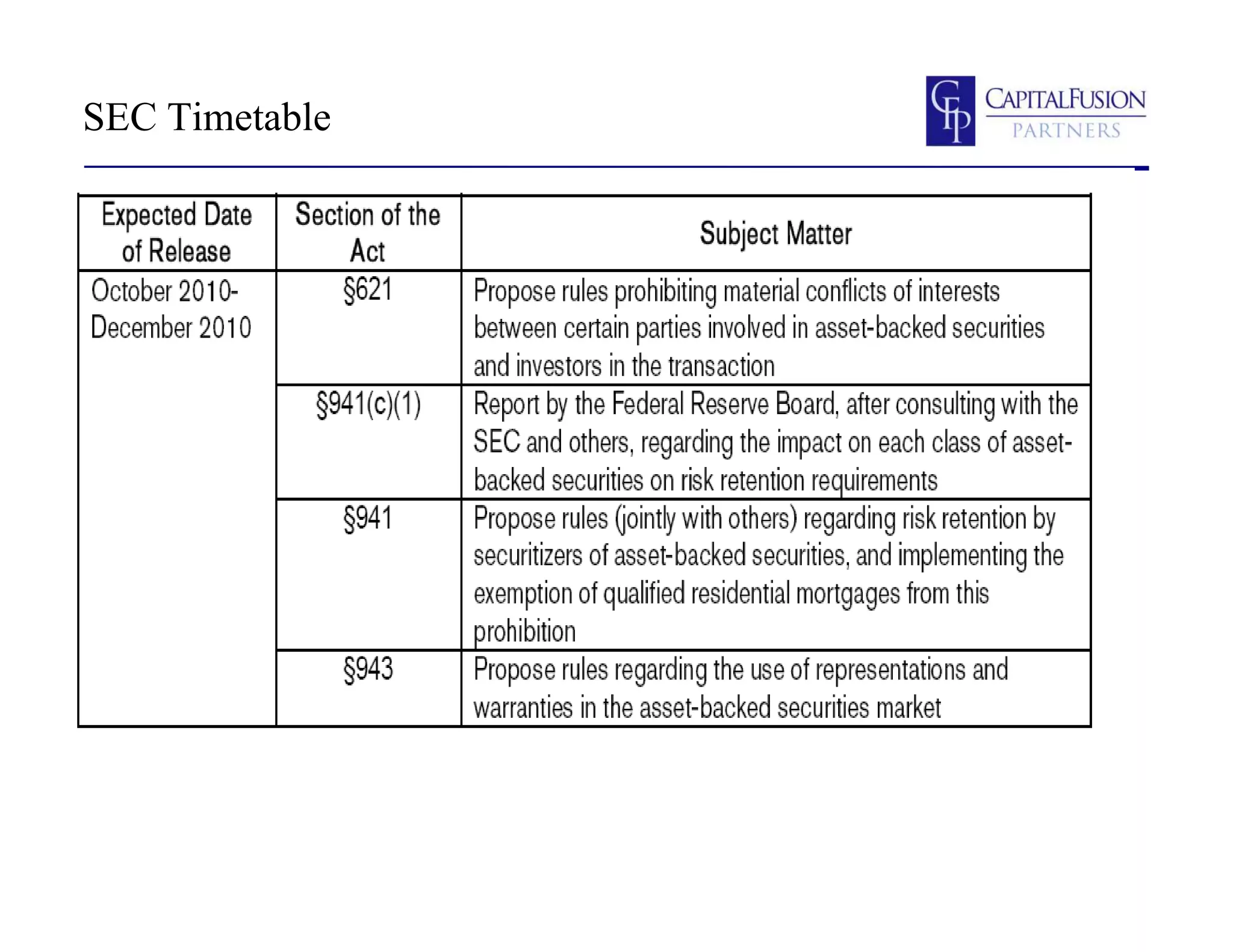

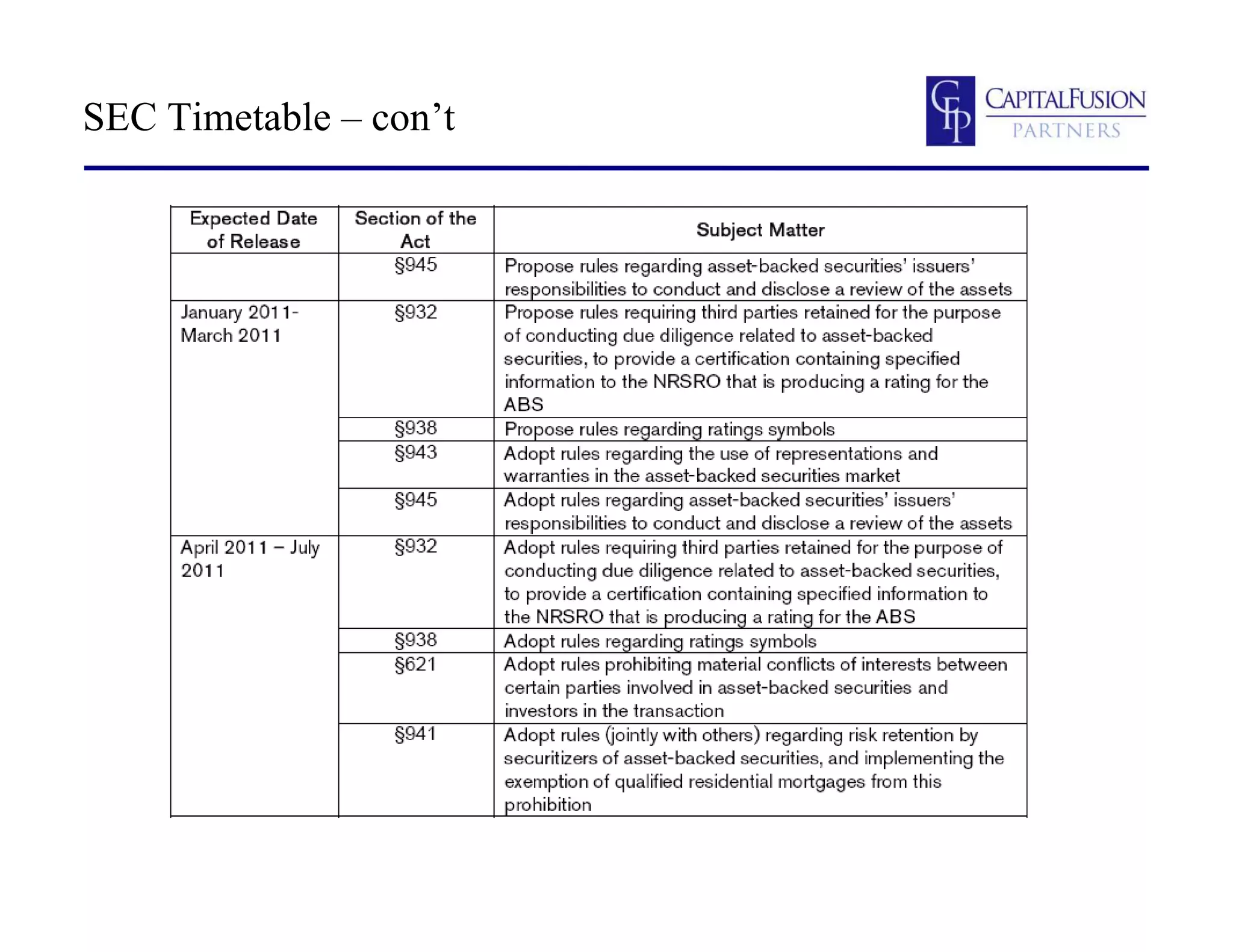

This document summarizes a presentation on due diligence, reporting standards, and transparency in asset-backed securities given by John Joshi of CapitalFusion Partners. It discusses proposed new SEC rules on risk retention and standardized loan-level data disclosure in securitizations. The presentation notes headlines about financial regulatory reform and lawsuits against firms involved in subprime mortgage securitizations. It outlines a SEC timetable for proposing and finalizing new securitization rules and identifies key changes needed for securitization markets like improved transparency, standardized disclosure, rating agency reform, representations and warranties, and effective regulation.