Abc of hospital finance

•

2 likes•1,231 views

ABC of finance of hospital .A hospital adminstrator requires this knowledge .

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Abc of hospital finance

Similar to Abc of hospital finance (20)

More from Dr.Ashok Khandelwal

More from Dr.Ashok Khandelwal (20)

Recently uploaded

Recently uploaded (20)

Abc of hospital finance

- 1. 4/17/2015 http://www.healthbizindia.in/flip.php?type=26&date=20150413%2000:00:00#page1718 1/1

- 2. 4/17/2015 http://www.healthbizindia.in/flip.php?type=26&date=20150413%2000:00:00#page1819 1/1

- 3. Health Biz India May 20154 Front of the Book Top News------------------------------------------------06 News that impacts the industry in ways more than one. Every month, we fish out and bring to you the top news from among the lot of numerous news that streams in CurrentAffairs----------------------------------------08 Latest takeovers & mergers, new launches, new technologies, and updates of the industry Content May 2015 Vol 5 Issue 2 Center Stage----------------------------------------------------------------------------18 The Inspire Series: MiraCradle is an affordable passive cooling device, which uses the advanced savE® phase change material (PCM) technology to induce therapeutic hypothermia among newborns suffering from birth asphyxia. It has been developed by Pluss Polymers in collaboration with CMC Vellore. And the best part? It costs just under Rs. 2 lakh, while others in the market are no less than `10-15 lakh! Editor-in-Chief Jayata Sharma-Sand Editorial Contributors Vivek Shukla Dr. AK Khandelwal Vipul Jain Dr. Anand Shroff Subodh Tiwari Avirat Shete Marketing & Sales Regional Sales Head (New Delhi) Bhupesh Tewari Consultant (Mumbai) Deepti Khanna Art & Design Glowrt Design House Cover Design Pramod Jadhav Online Production Pramod Jadhav & Vishal Phalke Disclaimer: Health Biz India is an online maga- zine only. We do not deal in any other service/ product under this name. Views and opinions expressed in this magazine are not necessarily those of Health Biz India, its Publisher and/or Editors. We, at Health Biz India do our best to verify the information published but do not take any responsibility for the absolute accuracy of the information. Health Biz India does not take the responsibility for any investment or decision taken by readers based on the information provided in the maga- zine. No part of this magazine can be reproduced without prior written permission of the Publisher. Health Biz India reserves the right to use the information published in the magazine in any manner whatsoever. Printed by Vijay Dhingra and Published by Jayata Sharma-Sand on behalf of Health Biz India. Printed at 1752, Street No. 10, Rajgarh Colony, Krishna Niger, New Delhi 110051; and Published at C-1/701, Neelpadamkunj, Sector 1, Vaishali, Ghaziabad 201010 HEALTH BIZ INDIA India’s 1st Online Healthcare Business Magazine Content May 2015_vol5 issue2 _HB.indb 4May 2015_vol5 issue2 _HB.indb 4 13-05-2015 22:49:5213-05-2015 22:49:52

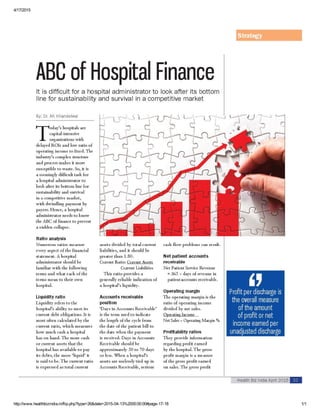

- 4. 34 Strategy Health Biz India May 2015 By: Dr. Ashok Khandelwal I n the last issue, we started discussing how it is a difficult task for a hospital administrator to look after its bottom line for sustainability and survival in a competitive market. Several ratio calculations and the ABC of finance was written about. In this second and final part of the series, we will try and know more about budget planning and making of financial reports. Budget planning A budget is a formal written statement of a hospital’s plan for the future. The financial budget is a management control tool normally covering a one year period. The essentials of budgeting are to set specific goals for future operations and to have a periodic comparison of actual results with the financial goals established. There are three types of budgets: operating budget, cash flow budget, and capital budget. The objectives of a budget are: • To provide written terms of the hospital goals • To provide a basis for the evaluation of financial performance according to the plans • To provide a tool to control costs • Statistical budget The first step in preparing an operating budget is to prepare the statistical budget. The objective is to provide a measure of activity in each department for the upcoming budget period. Examples: Number of radiological investigations, number of pathological investigations, number of indoor patients, outdoor patients, number of operations, etc. Planning & Reporting Budget planning and financial reports should form a major part of a hospital administrator’s profile May 2015_vol5 issue2 _HB.indb 34May 2015_vol5 issue2 _HB.indb 34 13-05-2015 22:50:1813-05-2015 22:50:18

- 5. 36 Strategy Health Biz India May 2015 Knowledge of the past performance of a facility is useful in the forecasting. The last five years is an appropriate amount of history to keep on file. This enables management to plan for future operations. • Operating budget The operating budget is composed of the expense budget and revenue budget. It mentions, for the upcoming fiscal year, anticipated income by source, and anticipated xpenses. Administration should always pursue a larger revenue budget than expense budget, therefore projecting a profit on the bottom line. The profit is used to finance the capital budget. • Capital budget ‘The capital budget summarises future plans for acquisitions of plant facilities and equipment. It is essential for the growth and survival of a hospital in present era of competition. Cost benefit analysis should be used appropriately. It should be around 2%. • Cash budget Without cash, a hospital cannot survive. This is the primary reason for a cash budget. In the present era of around 30-50% of services provided on credit basis for TPAs, medical insurance, and corporates, the problem of delayed payment in this reccessible amount and predicting cash flow requires a lot of thought and planning. Cash flow should be reviewed on a monthly basis to enable administration to foresee cash shortages and seek possible financing if necessary. Financial reports The hospital’s financial staff is responsible for providing the hospital administrator with accurate financial statements on a timely basis. Why is it important to understand your financial reports? Because financial statements are the language of business. Not understanding them leaves you vulnerable to a number of potentially unpleasant situations. Advantages of knowing your financial reports: Information is provided about whether your hospital is profitable or not; you come to know if your hospital operations provide enough cash flow to: pay your debts, pay your current Statistical Budget Expense Budget Revenue Budget Operating Budget Capital Budget Expected Operating Expenditure Finance 9% Administrative 6% Man Power cost 40% Operational 45% • Analysis of Financial Ratios A B C • Budget Planning • Comprehending Key Financial Reports May 2015_vol5 issue2 _HB.indb 36May 2015_vol5 issue2 _HB.indb 36 13-05-2015 22:50:2113-05-2015 22:50:21

- 6. www.healthbizindia.in 37 Strategy Health Biz India May 2015 obligations (like payroll and rent); it is the way to know if your hospital business has grown. Simply being on high occupancy or more utlisation of services is not a reliable indicator of true practice growth or financial health. Balance sheet The balance sheet reports the hospital’s assets, liabilities and fund balance. Assets can be current, property, plant, equipment, designated and other. Current assets have an expected life of one year or less. These include cash, accounts receivable and inventories. It is expected that inventory supplies will be used within one year of purchase. Property, plant and equipment assets have a life of more than one year. Designated assets may be board-designated accounts such as fund depreciation, self-insurance reserves or other reserve accounts, or trustee-designated accounts, which include interest and sinking funds as required by bond trustees. Other assets include donated property, bond issuance costs and deferred charges. Liabilities are the monies a hospital owes to other parties, or benefits that the hospital has accrued but not yet earned. Liabilities are recorded in two categories – current liabilities and long-term liabilities. Current liabilities are those that are expected to be paid by the hospital within one year. For example, under ‘Accounts Payable’, paying vendors for hospital supplies. Long-term liabilities require extended payments, the hospital’s long-term debt is a long-term liability. The fund balance or retained earnings is the difference between total assets and total liabilities and represents the equity of the hospital. It is an accumulation of all the prior year’s earnings and contributed capital such as stock or donations. Profit and loss statement (P&L) It is also known as income statement. Revenue in the income statement represents patient revenues or charges to the patient for hospital services provided. Revenue is the accumulation of total patient billings. Gross revenue is the total charge that the hospital has billed for services provided to the patient. Net revenue is the amount that is expected to be paid by the patient and a third-party payer, such as Mediclaim, ECHS, CGHS etc. • Covering a one-year period Operating Budget Cash Flow Budget Capital Budget • Supplementing the operating budget • Generally covering a three-year pan May 2015_vol5 issue2 _HB.indb 37May 2015_vol5 issue2 _HB.indb 37 13-05-2015 22:50:2113-05-2015 22:50:21

- 7. 38 Strategy Health Biz India May 2015 Contractual allowances, bad debt, discounts and charity care account for the difference between gross revenue and net revenue. These allowances are one of the features that make hospital accounting different from most other industries’ accounting practices. The ‘contractual allowance’ is the difference between the hospital’s gross charge and what the third party will be paying under the reimbursement system. Different payers have different reimbursement methodologies, and each third-party payer has different systems for reimbursing inpatient and outpatient services. They usually pay less than actual charges. The amount of contractual allowances fluctuates and is an estimate. Generally accepted accounting principle (GAAP) requires that bad debt expense be listed as an expense item and not a deduction from revenue. Many hospitals still list it as a deduction from revenue, producing a discrepancy with how bad debt is listed in their audited financial statements. Bad debt is considered a revenue deduction in the case of net revenue per patient day and net revenue in accounts receivable. Expenses in hospital accounting are fairly straightforward. There are two broad categories of expenses – operating expenses and capital expenses. Operating expenses consist of salary and non-salary expenses (supplies and materials, fringe benefits, etc.). Capital expenses represent the depreciation, amortisation and interest expense associated with capital purchases or leases. Conclusion Today, in the era of rising cost and price sensitive customer, it is very essential that a hospital administrator should have knowledge and understanding of the ABC of hospital finance. It is a key to the efficient operation of any hospital and is especially critical to the survival of the hospital. QT 11% Ward 29% Investigations 29% Pharmacy 31% About the author Dr. Ashok Kumar Khandelwal is the Medical Director, Anandaloke Hospital & Neurosciences Centre, West Bengal. He is a trained Assessor from the National Accreditation Board for Hospital and Health Care Provider (NABH). He carries around two decades of experience in the hospital industry and 15 years of experience as a hospital administrator. Profit & Loss Account Balance Sheet Cash Flow Account Cash Flow Three Key Financial Reports May 2015_vol5 issue2 _HB.indb 38May 2015_vol5 issue2 _HB.indb 38 13-05-2015 22:50:2113-05-2015 22:50:21