Download to read offline

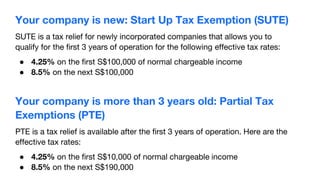

The document outlines the tax system in Singapore, emphasizing tax residency requirements, key tax rates, and various exemptions available for companies. Newly established companies can benefit from the Startup Tax Exemption (SUTE) for the first three years, while older companies may qualify for Partial Tax Exemption (PTE). Additional incentives include foreign tax credits and various deductions aimed at encouraging business expansion and development.