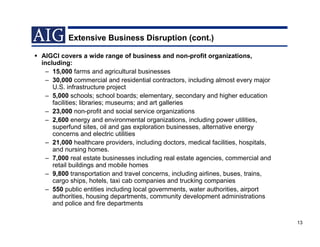

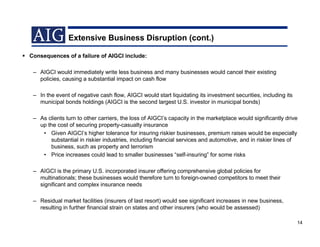

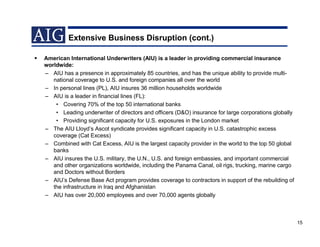

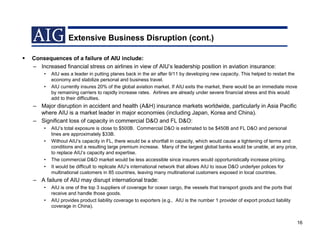

The document discusses the systemic risk posed by an AIG failure and its potential consequences. It summarizes that an AIG failure would: 1) Have devastating impacts on the global economy due to AIG's extensive business operations and interconnections. 2) Potentially trigger a "run on the bank" for AIG's $1.9 trillion in life insurance policies and cause turmoil in credit markets beyond the Lehman fallout. 3) Negatively impact the U.S. government's efforts to stabilize the economy by crushing confidence and increasing borrowing costs.