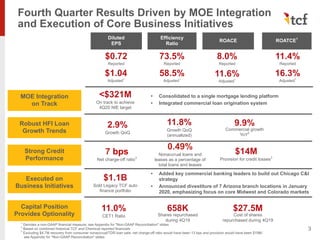

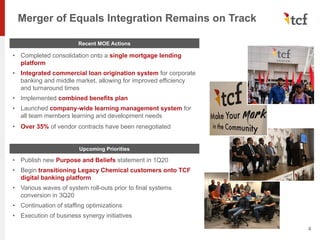

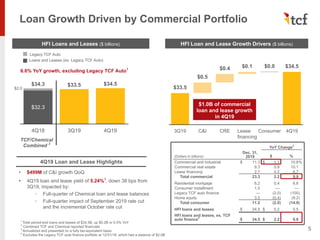

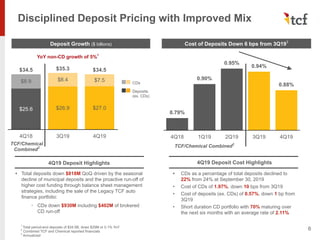

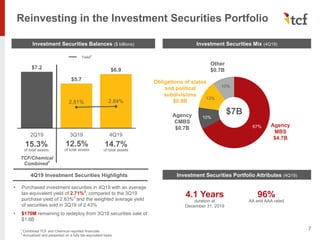

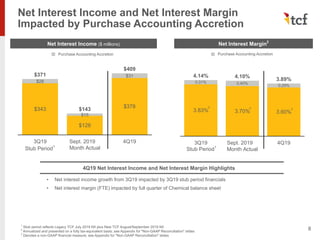

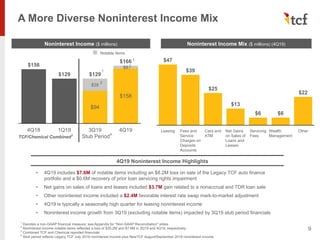

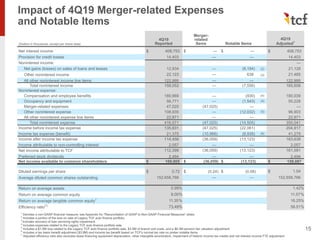

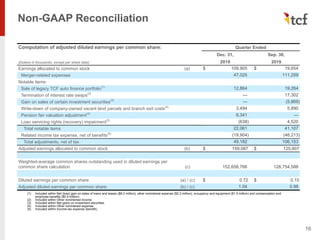

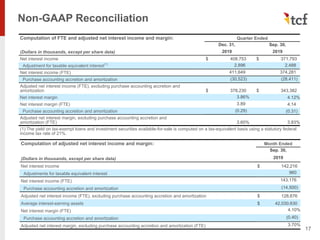

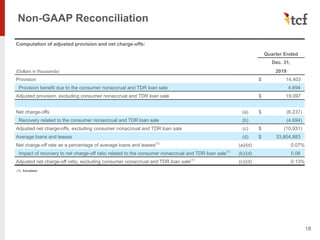

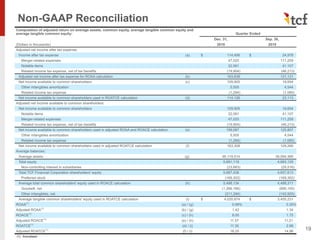

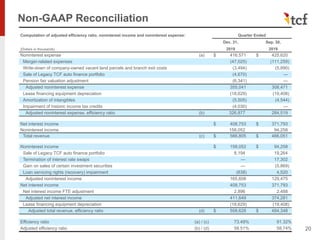

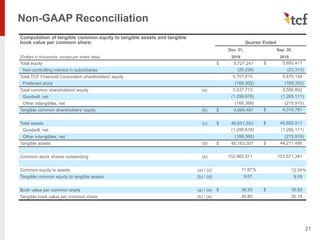

TCF Financial Corporation held a 4Q19 earnings presentation on January 27, 2020. The presentation contained forward-looking statements regarding TCF's financial performance and the merger with Chemical Financial Corporation. The presentation also contained cautionary language stating that TCF's actual future results could differ from projected results due to risks and uncertainties. TCF provided non-GAAP financial measures to allow for comparisons between periods and other institutions, but warned that non-GAAP measures have limitations. TCF reported diluted EPS of $0.72 but adjusted diluted EPS was $1.04. Integration of the merger was on track and loan growth was strong, particularly in commercial loans, while credit quality remained solid.