Download to read offline

![The challenge of raising productivity

The success stories—and failures—of the

1995-to-2000 productivity acceleration show why

companies need a comprehensive approach to

productivity.9

Walmart prioritized lowering costs

to offer higher-value-added goods, invested in a

hub-and-spoke distribution model to decrease

logistics costs, and deployed IT systems

specifically designed to improve in-store employee

efficiency. Intel prioritized ongoing development

of next-generation chips, standardized training,

and overhauled production processes to enable

quicker shifts to new higher-value-added products

that would sustain growth. Both companies

delivered significant productivity gains.

On the other hand, retail banking companies

created a more convenient customer experience

with online banking but failed to shift customers

from legacy products to higher-value-added

services. They made significant investments in

technology but not in employee training, ending up

9

McKinsey Global Institute, “US productivity growth, 1995–2000,” 2001.

10

Growth in GDP per capita, productivity and ULC, OECD.Stat; Over the 10 years preceding the [financial] crisis, trend labor productivity

growth declined in all G7 countries, particularly in France, Italy, and the United Kingdom. In the case of Canada, the United Kingdom and the

United States, the decline since the end of the 1990s marked a reversal of growth that coincided with the IT revolution. In other countries,

trend labor productivity growth has shown a gradual decline over the past 40 years [ending 2015] from relatively high rates; “Productivity

trends in G7 countries,” OECD iLibrary, Chapter 5.

with unused computing power that went beyond

the capabilities of the organization to leverage.

Hotels made significant investments in CRM

systems but continued to operate in silos, with

poor data sharing across properties, limiting the

potential benefits from creating better customer

experiences. They missed an opportunity to

extract more value from revenue management

systems because of a lack of employee training

and capability building.

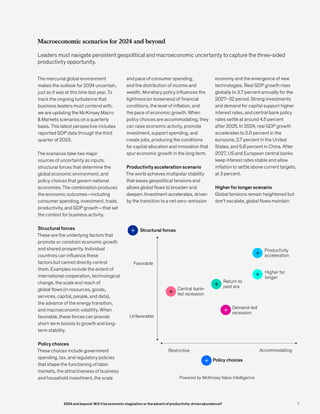

The challenge of creating productivity growth at

the economy level is likewise high, as the record

of G7 countries makes clear. In the 1995–2005

decade, growth in GDP per hour worked across

the G7 countries averaged just above 2 percent

annually (higher at the beginning of this period and

lower at the end). From 2010 to 2019, productivity

growth was just below 1 percent. In 2022,

productivity was negative in four G7 countries,

creating a roughly 0.5 percent decline for the

seven countries combined (Exhibit 4).10

Exhibit 4

Rates of productivity growth have been declining in G7 countries.

Trend GDP per hour worked, constant prices¹

1

Trend productivity growth derived using the Hodrick Prescott filter.

Source: OECD; McKinsey analysis

Rates of productivity growth have been declining in G7 countries.

McKinsey & Company

–2

–1

0

1

2

3

4

5

6

1970 1980 1990 2000 2010 2020

US

UK

Japan

Italy

Germany

France

Canada

13

2024 and beyond: Will it be economic stagnation or the advent of productivity-driven abundance?](https://image.slidesharecdn.com/2024-and-beyond-will-it-be-economic-stagnation-or-the-advent-of-productivity-driven-abundance-240410231536-614a0a6b/85/2024-and-beyond-will-it-be-economic-stagnation-or-the-advent-of-productivity-driven-abundance-pdf-13-320.jpg)

![Even productivity success can create unintended

consequences as the “creative destruction”

critical to productivity growth displaces existing

jobs, businesses, and industries.11

The last wave

of globalization lifted millions out of poverty but

entailed many consequences that were either

ignored, minimized, or simply missed along the

way. For example, the repercussions of labor

market polarization in the United States and

Europe (where high-education, high-wage and

low-education, low-wage jobs grew but middle-

paying jobs stagnated) are still being felt today.12

Governments, international institutions, and

businesses can choose to intentionally create an

environment conducive to productivity growth

and spend the resources to actively manage the

transition to new jobs, business opportunities,

and entire industries. Collectively this would lead

to prosperity that can be shared by all.

11

Shigeru Fujita, “Creative Destruction and Aggregate Productivity Growth,” Philadelphia Fed Business Review, Q3 2008; As originally

articulated by Joseph Schumpeter: “The fundamental impulse that keeps the capital engine in motion comes from the new consumers’

goods, the new methods of production and transportation, the new markets… [The process] incessantly revolutionizes from within,

incessantly destroying the old one, incessantly creating a new one. This process of Creative Destruction is the essential fact of

capitalism.” Joseph Schumpeter, “Capitalism, Socialism, and Democracy,” Third Edition, 1942.

12

David Autor; “Polanyi’s Paradox and the Shape of Employment Growth”, NBER Working Paper 20485, September 2014

Business productivity gains not only improve

company performance but translate into GDP

growth and higher living standards. Business

leaders who make decisions with this broader

view in mind have a higher chance of raising

shareholder returns while delivering on the

corporate purpose they had set out to achieve.

While delivering sustained productivity growth

is not easy, management teams have repeatedly

surmounted seemingly impossible challenges

over the past four years by taking unprecedented

actions, with exceptional speed, in the face of

enormous uncertainty. Leaders who internalize

these hard-won lessons and incentivize the

behaviors that have helped them weather the

recent period can significantly raise their odds of

outperformance and help make 2024 the advent

of future abundance.

Copyright © 2024 McKinsey & Company. All rights reserved.

Ezra Greenberg is a partner in McKinsey’s Stamford office, Asutosh Padhi is a senior partner in the Chicago office and

the North America managing partner, Sven Smit is chair of the McKinsey Global Institute and a senior partner in the

Amsterdam office.

The authors would like to thank Matt Banholzer, Vincent Bérubé, Rebecca Doherty, Steven Eklund, Arvind Govindarajan,

Sebastian Kohls, Alina Malinauskaite, Jake Matthews, Jake Milner, Nicholas Pingitore, Richard Sellschop, Erik Schaefer,

Zachary Silverman, Scott Schwaitzberg, Sarah Walker, Joris Wijpkema, and Shubo Yin for their contributions to this article.

14 2024 and beyond: Will it be economic stagnation or the advent of productivity-driven abundance?](https://image.slidesharecdn.com/2024-and-beyond-will-it-be-economic-stagnation-or-the-advent-of-productivity-driven-abundance-240410231536-614a0a6b/85/2024-and-beyond-will-it-be-economic-stagnation-or-the-advent-of-productivity-driven-abundance-pdf-14-320.jpg)

The document discusses the economic outlook for 2024 and beyond, arguing that pursuing productivity gains through upskilling workers, optimizing capital investments, and operating with excellence can lead to either economic stagnation or a new era of abundance. It notes uncertainties around inflation, interest rates, and demographic shifts that may constrain growth. However, it asserts that accelerating productivity across companies similar to the 1990s US can boost overall economic performance and standards of living if business leaders actively pursue the "three-sided productivity opportunity" of changing how their organizations operate, investing in technology and innovation, and offsetting higher costs. The document aims to convince readers that prioritizing productivity is the best path forward for both business success and economic prosperity in 2024