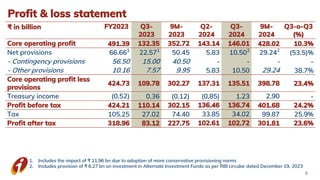

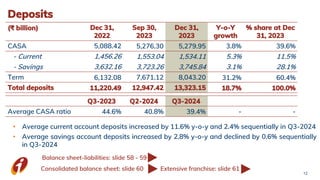

ICICI Bank reported its financial results for the third quarter of 2024. Core operating profit grew 10.3% year-over-year to Rs. 146.01 billion. Retail loans grew 21.4% year-over-year while deposits grew 18.7% year-over-year. The bank continued expanding its digital platforms to enhance customer experience.