Downloaded 57 times

![© benefitexpress 2016

Final SBC Templates Released

SBC Template and Instructions.

The template itself is substantially similar to the most recent proposal. In the “Why This

Matters” column relating to the “Important Questions” chart, the prescribed language for

describing certain coverage components—including services covered before the

deductible is met, embedded deductibles for family coverage, and out-of-pocket limits—

has been made clearer and more straightforward.

For the coverage examples, the instructions explain that the generic “[cost sharing]”

notations in the template should be replaced with the appropriate cost-sharing category

(e.g., copayment, coinsurance) to accurately reflect the plan.

Overall, the instructions provide more details than the currently applicable instructions—

for example, specifying where in the SBC the plan should add premium information, if it

voluntarily chooses to do so.](https://image.slidesharecdn.com/new-developments-in-health-welfare-plans-160628192943/85/2016-Developments-in-Health-and-Welfare-Plans-54-320.jpg)

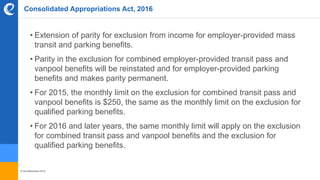

The document outlines significant changes from December 2015 regarding regulations from the EEOC, IRS, DOL, and HHS, particularly related to the Affordable Care Act (ACA). Key updates include guidance on employer-sponsored coverage, requirements for health reimbursement arrangements, adjustments to affordability standards for employer mandates, and the extension of reporting deadlines for ACA-related forms. Additionally, the Consolidated Appropriations Act of 2016 introduces provisions delaying the implementation of the 'Cadillac tax' and creating parity for employer-provided transit and parking benefits.