Download to read offline

![Geometry Global is the largest and most geographically complete

activation agency of its kind, providing brand marketers with

a unique solution for an unmet need: Precision Activation. This

proprietary approach focuses on the exact blend of context and

content that combine to influence consumer behavior, transforming

proven communication techniques and big creative ideas into

effective and profitable business growth drivers. With a team of

4000 experts in 56 markets, the global network develops highly

compelling marketing programs – informed by data and insights

– connecting people with brands at precisely the right times, in

the right places, and right ways – making a measurable difference

to clients’ businesses. Launched in June 2013, Geometry Global

delivers award-winning creativity and integrated talent across a

range of disciplines including Shopper, Relationship, Promotional

and Experiential, Trade and Digital Marketing.

For more information, visit www.geometry.com

As humans, we constantly seek to define and

evaluate ourselves, using social interactions,

experiences and personal inventory to project our

own identity. Community and participation are

powerful influencers: we crave connections with

people whose beliefs and values we share. And with

digital as the mighty enabler, our connections are

widening alongside our collective experiences.

People’s relationships with brands have changed.

A recent survey [GlobalWebIndex] asked

consumers how they would want a brand to act

towards them: 50 percent of 25-34 year olds

reported their favorite brand plays an integral

part in their online life and experience, while 38

percent would buy a product or service simply to

be part of the community around it.

Add to this the Convergence Economy [LS:N Global]

where boundaries between brands, sectors,

economy and emotion are dissolving. Look to retail

spaces, products, hospitality and entertainment and

there’s one distinctive theme: it’s difficult to tell one

thing from the other.

Consequently, we need a fresh way to activate

brands, to find new ways to engage with people and

gain a greater share of life and “share of self.”

Today’s smart winners are imaginative, reaching

outside of their historical boundaries to create new

experiences and solutions. Nike, Samsung, Sony and

others, are moving from purely product offers to

services and lifestyle enhancement. For the time

poor, Google’s Future Home has launched life-

enhancing apps from voice-activated cooking to

tablet-operated smart TV.

Such brands are going wide and creating

partnerships to take an increased share of life.

Clothing retailer Banana Republic has collaborated

with Condé Nast Bon Appetit and online reservation

service Open Table to create a Desk to Dinner

collection – an innovative solution for the working

woman while making the brand relevant to a much

larger market. Through a collaborative movement,

Shop Elsewhere in Hong Kong enabled independent

fashion retailers to recommend each other’s

products, allowing shoppers browsing in one

designer’s store to activate the QR code on an item,

leading to a web site with recommendations for

other designers’ products pre-selected to match.

Designers increased reach and attracted new clients

while creating a unique in-store experience.

Critical to brand success in this digital age is the

ability to create precise and relevant connections

and experiences, with communications that engage

people at the right time, in the right place and in the

right way. Mastery of big data has replaced

supposition to extract real time consumer insights,

enhancing a sense of self. In Korea, retailer Emart

created a mobile, Wi-Fi flying store. High footfall

rivals were visited by the drones encouraging

consumers to connect to the flying store via

smartphones. Once connected, consumers were

directed to the Emart online shopping portal to

access discounts. The result: satisfied, value

conscious shoppers and soaring sales for Emart.

The human brand

Technology and data are merely brand conduits and

enablers. The reality is that brands are transitioning

from acquaintance to become life influencers in real

and valuable ways.

Smart brands are inviting people to share an

experience, rather than product. Apple changed the

retail landscape forever to become the supreme

shopper experience where people could learn, seek

help and socialize. In tandem with its aspirational

product it became an iconic global brand with the

best brand retention in the industry [source: WDS].

And this engagement goes beyond the physical,

with 10 percent of Internet users having talked about

Apple online (GlobalWebIndex). In Latin America,

Huggies moved the hearts and minds of parents

when, to celebrate Friendship Day, it delivered a

special crib for two new born babies to a maternity

ward. Bringing two boys together meant each had

their first friend. And Huggies created a moment

parents would never forget.

Apple and Google’s brand-lifestyle ecosystems are an

elegant attempt by both brands to refocus themselves

around an arresting experience; demonstrating

reliability, innovation, design and a defined personality

across every customer touch point.

Participatory brands are here

and now

The past is another country for brands, as they

journey towards a social role within a much broader

community. People are now invited to view brands

as they do their friends, colleagues and partners –

offering products and services the opportunity to

embrace change and help people to think smarter,

lead healthier lives, and enjoy richer experiences.

To succeed, a brand simply has to be clear about its

own values, and the places, spaces and occasions

where it has both role and purpose.

1. People are seekers, searching for solutions

– functional or emotional – to support both them

and their identity. Brands must understand these

needs and their associated behaviors.

2. In doing this, brands can move away from industry

definitions of category to identify opportunities

by observing consumer and shopper behavior

relating to consumption, usage occasions and

solutions that enhance people’s lives.

3. For example, in Asia, Cadburys incentivized

shoppers to give chocolate at key gifting

occasions with its “Say it with chocolate”

campaign. Allowing shoppers to create

personalized messages in store, this innovative

approach created a crucial social connection

with the brand, sharing joy and changing

purchase behavior.

MY

BRANDS.

MY

SELF.Jonathan Dodd

Global Chief Strategy Officer

Geometry Global

Jonathan.Dodd@geometry.com

92 BrandZ™ Top 100 Most Valuable Global Brands 2014 9392 BrandZ™ Top 100 Most Valuable Global Brands 2014

Section 03 | Thought Leadership](https://image.slidesharecdn.com/c2eb24e1-33d6-4efc-877d-695a6cd83dbf-150225120221-conversion-gate02/85/2014_BrandZ_Top100_Report-47-320.jpg)

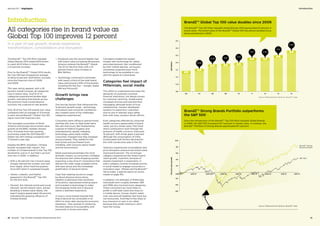

The 2014 BrandZTM Global Top 100 report found that the total brand value of the top 100 brands grew 12% to $2.9 trillion. This marks a shift from economic recovery to growth. Key points: - All categories increased in value led by Apparel at 29% growth. - Google overtook Apple as the most valuable brand. - Tencent was the fastest growing brand at 97% value increase. - Technology brands still dominate representing 1/3 of total value. - Growth has led to new challenges for brands around consumer expectations shaped by mobile technology.

![[Millward Brown] Brandz report 2014](https://cdn.slidesharecdn.com/ss_thumbnails/2014brandztop100report-140928232328-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)