Recommended

More Related Content

What's hot

What's hot (20)

Similar to 3 jewellery market_structure

Similar to 3 jewellery market_structure (20)

Recently uploaded

Recently uploaded (20)

3 jewellery market_structure

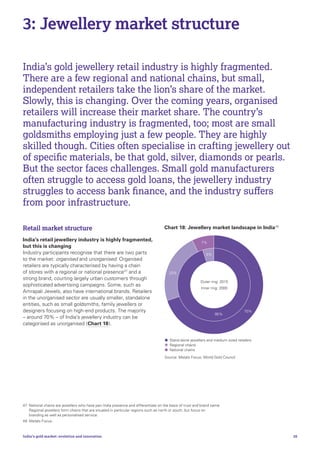

- 1. 28India’s gold market: evolution and innovation 3: Jewellery market structure Retail market structure India’s retail jewellery industry is highly fragmented, but this is changing Industry participants recognise that there are two parts to the market: organised and unorganised. Organised retailers are typically characterised by having a chain of stores with a regional or national presence47 and a strong brand, courting largely urban customers through sophisticated advertising campaigns. Some, such as Amrapali Jewels, also have international brands. Retailers in the unorganised sector are usually smaller, standalone entities, such as small goldsmiths, family jewellers or designers focusing on high-end products. The majority – around 70% – of India’s jewellery industry can be categorised as unorganised (Chart 18). India’s gold jewellery retail industry is highly fragmented. There are a few regional and national chains, but small, independent retailers take the lion’s share of the market. Slowly, this is changing. Over the coming years, organised retailers will increase their market share. The country’s manufacturing industry is fragmented, too; most are small goldsmiths employing just a few people. They are highly skilled though. Cities often specialise in crafting jewellery out of specific materials, be that gold, silver, diamonds or pearls. But the sector faces challenges. Small gold manufacturers often struggle to access gold loans, the jewellery industry struggles to access bank finance, and the industry suffers from poor infrastructure. 47 National chains are jewellers who have pan-India presence and differentiate on the basis of trust and brand name. Regional jewellers form chains that are situated in particular regions such as north or south, but focus on branding as well as personalised service. 48 Metals Focus. 38% Stand alone jewellers and medium sized retailers Regional chains National chains Chart 18: Jewellery market landscape in India48 Source: Metals Focus; World Gold Council 23% 7% 70% 95% 5% Outer ring: 2015 Inner ring: 2000

- 2. 29India’s gold market: evolution and innovation 49 This includes organised and unorganised retailers. 50 For more detail on the round table discussions, please see the methodology box. 51 Handbook of Statistics on the Indian Economy, RBI, 2015. 52 Company websites and investor presentations, correct as at April 2016. 53 Metals Focus. It is difficult to accurately quantify the number of jewellers across the country. The industry’s highly fragmented nature and very long tail of small retailers make it quite opaque and hard to gain full visibility. Even estimates by trade associations can vary considerably on a state-by- state basis. In order to form our own estimate we undertook a granular, bottom-up approach reviewing data on Justdial, a pan-India search services company. Based on this analysis, we estimate there are between 385,000 and 410,000 jewellers in India.49 This figure resonated with the industry during the round table discussions held in Mumbai, Kochi and Delhi.50 In contrast, there are only 125,857 bank branches.51 There are signs that the shape of the market is changing. Between 2000 and 2015 we have seen the emergence of more organised participants, with their market share rising from 5% to 30%. By 2020, it is likely that this share will have risen to between 35% and 40%. This trend is concentrated in cities, supported by growing urbanisation and increasing awareness of branded jewellery among younger consumers. Regional chains have taken the lead in increasing market share, but some national retailers have also emerged (Table 6). For an example of the rise of organised retailers, please see Focus Box: The rise of Tanishq. But the unorganised sector remains the major force in jewellery retailing across India. Local standalone family jewellers continue to dominate rural centres, not least as they fulfil several roles, including in some instances acting as banker. This role aside, there is also a clear demarcation between the market segment catered for by standalone retailers and that catered for by regional and national chains (Table 7). Table 6: Organised retailers‘ presence52 Name Stores Cities/towns Tanishq (Including Zoya) 195 111 GOLDPLUS 32 31 PC Jewellers 58 48 Shubh Retail 80 N/A* Malabar Gold and Diamonds 80 69 Kalyan Jewellers 68 59 Joyalukkas 58 53 *Not available Source: Metals Focus; World Gold Council Table 7: Size of retail shops, stocks and employees53 Stand alone/ Independent retailers Medium sized retailers Regional chains National chains Organised Unorganised Distinctive feature Caters to the market where customers make purchases based on price This can include family retailers. The focus is on the traditional market The focus is on local trends and designs. The differentiator is purity and trust The focus is on brands and purity. Typically, these chains have high making charges. Shop size in sq ft 150-500 300-1,000 500-3,000 4,000-25,000 Inventory 5-20kgs 25-50kgs 30-150kgs 150-500kgs Display in store (% of total stock) 40-50% 60% 80% 90% Employees per store 4-5 10-15 20-35 40-60 Source: Metals Focus; World Gold Council Only 30%of Indian jewellery retailers are national or regionally branded chains

- 3. 30India’s gold market: evolution and innovation The growing importance of advertising As organised jewellers continue to grow and compete for business, they are embracing advertising to broaden their appeal. As explained in Chapter 2, while tradition and advice from friends and family are strong influencers on purchase behaviour, spontaneity and self-direction also play a role – some people buy a piece of jewellery simply because they see it and like it. Advertising can tap into that. Retailers view advertising campaigns as vital in targeting young, urban consumers. The evolution of retailers' advertising activity is interesting. In the past, more traditional means – such as print media – were used. Now, despite the cost, electronic as well as outdoor media are much more prevalent. On average, it can cost Rs9,000 per square centimetre to advertise in a leading Indian newspaper. By comparison, advertising on a national television channel during peak time may cost between Rs30,000 – Rs40,000 for a 10-second spot, and this can rise to Rs60,000 – Rs100,000 during major sporting events. Regional entertainment channels are cheaper, often by at least 30–50%.54 These often attract regional chains that prefer to advertise in local languages. The large organised retailers take marketing very seriously, allocating significant budgets. Television advertising spending by jewellers was consistently between Rs3400mn and Rs3700mn (US$56mn to US$58mn) during 2013–2015.55 To give a sense of individual company spend, top branded jewellery chain, Titan Company Limited, increased its advertising expenditure to Rs380mn (US$6mn) in 2015 from Rs240mn (US$4mn) in 2013. Similarly, Kalyan Jewellers spent Rs700mn (US$11mn) in 2015, up from Rs610mn (US$10mn) in 2013. Online market India has embraced online retailing. Flipkart, Snapdeal and Amazon are battling it out to gain market share in the broad consumer market. Some jewellery retailers have also ventured into this market place. At present retailers are largely focused on selling lighter pieces at lower price points online. Consumers have a strong preference to touch and feel larger or more intricate jewellery before purchasing – in our 2016 consumer research, 55% of consumers said they prefer to touch the product before buying it, and that was why they bought in-store rather than online. Although online jewellery retailing is at present a very small part of the market, it is growing. Traditional retailers are showing increasing interest in entering this space. In May 2016, Titan Industries acquired a majority stake in CaratLane, a move that will allow the company to enhance its e-commerce capabilities significantly and help target younger customers. Those close to the market believe that in 10 years online sales could account for between 7% and 10% of total sales by value. Whether or not this happens is dependent on the consumer – their preferences will shape how the online jewellery market grows. While the growth of online jewellery sales may take several years, online, digital and social activity already plays an important part of the purchase journey. In urban India 40% of consumers said that they browsed online before purchasing their jewellery. And around a quarter of urban consumers said that they used online blogs and social media for ideas and inspiration. For millennials – those aged between 18–33 years old – the figure is closer to a third. Gold jewellery transactions: cash buying vs exchange Cash is the most common method of purchasing gold jewellery. It accounts for 70%–80% of all transactions.56 But consumers often exchange bars and coins for jewellery. Why? There are two drivers which can influence whether bars and coins, or older jewellery, is exchanged for new jewellery or bought for cash: the time of year and gold price trends. Although gold is bought throughout the year, as discussed in Chapter 2, there are certain months when purchases accelerate, such as festive or marriage seasons. This affects how people buy gold jewellery. For example, during Diwali, the ratio of cash buying is much higher. This is because harvests have been reaped and cash has flowed into households’ coffers, especially in rural areas. This is in contrast to the marriage season when exchange rises as consumers exchange bars and coins, which they have accumulated over many years, for bridal jewellery. The Indian consumer is very savvy when it comes to the gold price. During periods of high and rising prices, a consumer is more likely to exchange gold for new jewellery, saving cash to buy gold when prices are at levels they are more comfortable with. 54 All costs are 2015 averages. 55 Maxus India. 56 The remaining 20–30% of transactions are made by cheque, credit or debit card.

- 4. 31India’s gold market: evolution and innovation The early years India’s jewellery industry started to change in 1995 when Titan Industries,57 one of India’s leading watch manufacturers, launched its own jewellery brand, Tanishq. Its aim was to target a different type of jewellery consumer. Rather than focus on traditional 22-carat designs it developed a stylish portfolio of contemporary 18-carat jewellery and watches. Up until this point, the Indian jewellery market had been largely unorganised and fragmented, with few recognised brand names. Tanishq found trading challenging at the start. Domestic consumers did not readily accept a modern concept in what was such a traditional jewellery market. By contrast, exports performed well. Sales to key jewellery markets such as the UK, US, Australia and the Middle East flourished. Re-working its strategy for the home market Tanishq revised its strategy. With an initial emphasis on exports, its designs were predominantly Western oriented, but similar product lines were also offered at home. For many consumers, the designs were too contemporary. Given India’s diversity, Tanishq realised that it should cater to the tastes across the country. Its emphasis shifted from modern to more traditional design, including 22k and 24k ornaments inspired by designs from various states. It incorporated traditional styles into its more contemporary designs. The company also began seasonal and localised promotions based on Indian festivals, and embarked on an overhaul of its retail stores. The second step involved enhancing its brand and reputation by building trust. To do this it focused on purity. In 1999, Tanishq introduced the concept of Karatmeters in its retail boutiques. The Karatmeter used X-rays to provide an accurate reading, within three minutes, of the constitution of gold in an ornament. As part of its strategy, Tanishq also conducted tests on 10,000 ornaments selected at random. In many cases, the pieces were found to be under carat. Over time, this focus on purity proved to be a key selling point for Tanishq. And to bolster trust further it decided to use a standard gold price across all its showrooms from March 2000. This emphasis on trust led to a sharp jump in sales and helped the firm expand. By 2001, Tanishq had nearly 50 stores located in metros and Tier 1 cities. Tanishq further built its market by highlighting its connection with Tata, a trusted brand in the Indian corporate world with businesses ranging from steel to airlines. Its marketing budget expanded to encompass national-level spending (both electronic and print media), regional budgets, direct mail and research. Second push for penetration Having built its brand and established itself as a leading jeweller, Tanishq started to branch out. In 2005 it explored the corporate gifts and vouchers market and began to provide financing for the purchase of gold jewellery. In 2007, the company started focusing on higher-end jewellery with the introduction of Zoya, a chain of luxury jewellery boutiques encompassing designer and international designs. It also expanded its geographic coverage. After establishing Tanishq among the large and growing middle class in urban centres, Titan Industries decided to venture into rural India. To do so, it launched Gold Plus, a brand aimed at semi-urban and rural locations. Tanishq and Gold Plus delivered approximately Rs87bn (US$1.29bn) of combined net sales in 2015. Tanishq has over 190 stores and Gold Plus has over 30 stores, with a combined retail space of more than 800,000 sq ft. Tanishq is now one of the largest retail jewellery chains in India, with an excellent reputation for its combination of traditional and contemporary designs. Focus: The rise of Tanishq 57 Titan Industries is a subsidiary of Tata Group.

- 5. 32India’s gold market: evolution and innovation Manufacturing market structure Jewellery manufacturing also highly fragmented, but this is changing Even though India is one of the foremost jewellery fabricators in the world, its manufacturing facilities are largely unorganised. Barely 5%–10%58 of units operate as organised, large-scale facilities – ten years ago these would have hardly existed. The vast majority of the industry is characterised by small workshops, each typically employing two to four goldsmiths. This is reflected in the fact that between 60% and 65% of jewellery manufactured in India is handmade. This figure was much higher a decade ago – the rise of manufactured jewellery has led to the drop in share of handmade jewellery. One of the key reasons that jewellery manufacturing remains largely unorganised is the relatively low capital requirements of small workshops. Rarely do they own the gold on which they work. Instead, they carry out what the industry calls job work for others. Regions specialise in producing different types of jewellery Jewellery manufacturing in India is highly concentrated. Around 60%59 of the gems and jewellery industry is centred around Mumbai, Kolkata and New Delhi. The majority of jewellery manufactured in these locations is sold outside these cities, either nationally or internationally. As jewellery tastes and preferences differ across the country, so do manufacturing skills and expertise (Map page 33). Regions specialise in producing specific types of jewellery. Jaipur in Rajasthan has a world-class reputation for producing jewellery with semi precious stones and gems; Hyderabad has a tradition in pearls going back centuries, so much so that it is known as the City of Pearls; similarly, Surat in Gujarat is known as Diamond City. 58 Metals Focus. 59 Metals Focus, World Gold Council: an introduction to the Indian gold market. The majority of manufacturing facilities in India are small workshops of two to four employees. This is both a strength and a weakness. The artisan, bespoke nature of the handmade jewellery allows the karigars to produce beautiful, intricate pieces which are not possible with machine-made jewellery. But it also means the sector suffers from a lack of transparency. This makes it difficult for banks to lend and goes some way to explaining the lack of readily available capital, which would be required for a manufacturer to develop its workshop or factory and recruit more employees. Growth in organised manufacturing over recent years has owed much to the growth in exports and the requirements of the organised retail sector. International buyers, for example, have strict procurement policies which rule out many of the smaller workshops. Orders from overseas and domestic organised retailers are often large and manufacturers need to be of a certain size in order to fulfil them. Therefore, growth in the organised retail sector and in India’s jewellery exports – as outlined in Chapter 4 – has supported the development of the organised manufacturing sector. 60%–65% of jewellery manufactured in India is handmade

- 6. 33India’s gold market: evolution and innovation Key % = Regional share of Indian jewellery demand. 58 58 58 58 58 58 58 58 58 58 58 58 58 58 58 58 58 58 58 58 58 58 58 58 sh hattisgarh Odisha West Bengal Jharkhand Bihar Assam Meghalaya Arunachal Pradesh Nagaland Manipur Mizoram Tripura Andaman and Nicobar Islands Sikkim herry 58 6 3 1 3 1 22 East 15% South 40% Delhi/Agra Silver jewellery Kolkata Handmade jewellery derabad mi-precious dded jewellery mbatore ting jewellery king centres in India = The number of BIS-approved hallmarking centres in each Indian state.60 BIS. Major Jewellery manufacturing centres and hallmarking centres in India60 The map shows the number of BIS-approved hallmarking centres in each Indian state. Jammu and Kashmir Himachal Pradesh Punjab Haryana Rajasthan Uttarakhand Uttar Pradesh Madhya Pradesh Karnataka Andhra Pradesh Telangana Chhattisgarh Odisha Tamil Nadu West Bengal Jharkhand Bihar Assam Meghalaya Arunachal Pradesh Maharashtra Dadra and Nagar Haveli Delhi Gujarat Chandigarh Nagaland Manipur Mizoram Tripura Kerala Lakshadweep Andaman and Nicobar Islands Sikkim Puducherry Goa Daman and Diu 58 38 26 26 2 6 3 1 1 1 5 7 3 9 1 3 13 23 1 22 4 36 28 North 20% East 15% West 25% South 40% Delhi/Agra Silver jewellery Jaipur Kundan stones and semi precious Gujarat • Rajkot – coloured stones and gold jewellery • Surat – diamond polishing hub Mumbai • Machine made jewellery • Largest wholesale market Kolkata Handmade jewellery Hyderabad Semi-precious studded jewellery Coimbatore Casting jewellery Thrissur Lightweight jewellery Major jewellery manufacturing centres and hallmarking centres in India

- 7. 34India’s gold market: evolution and innovation Hallmarking It is odd that there has been little consumer protection in a country with such a strong relationship with gold The Bureau of Indian Standards (BIS) is the national body of standards in India. In 2000, it launched a long-term scheme to encourage the voluntary hallmarking of gold jewellery. The objectives of the BIS certification of gold are to protect consumers, support the export of gold jewellery and to develop the country as a reliable gold centre. BIS has made huge strides in this area. Over 300 hallmarking centres61 have been rolled out across the country (Map page 33), 13,000 jewellers have been accredited, and a supervisory structure has been established for both hallmarkers and retailers. But more needs to be done. Despite 15 years of hallmarking, gold jewellery is still routinely under-carated. According to research by the consultancy, Oliver Wyman, under-carating of gold jewellery weight has fallen from between 20%–40% to somewhere around 10%–15%, although the true percentage may well be far higher given there are limited number of BIS certified jewellers.62 This is an important issue for the consumer. In urban India, 5% of consumers say they do not know the caratage of the jewellery they bought in the past 12 months; this increases to 18% in rural India. Furthermore, 86% of respondents in India said that hallmarking is extremely or very important. Tackling this issue is key to ensuring the health of the gold industry. Consumer protection can be improved in the short and medium term More rigour in the hallmarking process would benefit India’s consumers and gold market. Trust in the industry would increase. This would benefit consumers, retailers and exporters. What needs to be done? In our report Developing Indian hallmarking, a roadmap for future growth, we advocate six short-term measures to improve the efficiency and effectiveness of hallmarking: • Strengthen governance around hallmarking processes • Drive customer awareness of hallmarking • Incentivise and facilitate expansion of hallmarking centres • Use BIS data to develop a ratings system for jewellers • Pilot Unique ID or other technology solutions to support hallmarking • Pursue membership of the International Hallmarking Convention, or develop an Asian alternative. Over the longer-term, we suggest: • Moving to a mandatory hallmarking regime • Placing the onus of hallmarking on manufacturers • Developing mechanisms to monitor the flow of gold across the supply chain. Mandatory hallmarking of jewellery with BIS Act, 2016 Recent developments herald further improvements, with the approval of a new BIS Act 2016. A detailed overview of the Bill is discussed in Chapter 10, but its primary aim is to make the hallmarking of gold jewellery mandatory and allow the government to enforce it. This could largely wipe out the malpractice of gold jewellery and ornaments of inferior purity being sold as 22-carat. 61 As of Jan 2017, there are 431 hallmarking centres. 62 World Gold Council, Developing Indian Hallmarking, a road map for future growth. Hallmarked bangle.

- 8. 35India’s gold market: evolution and innovation The hallmarking process explained In accordance with BIS procedures, hallmarking is applied to all parts of the item that can be easily detached or replaced, except for bangles and light weight items where hallmarking is only applied once. A hallmark is made up of five different symbols which should be inscribed to illustrate the following: • BIS mark • Fineness • Assaying and Hallmarking Centre mark • Year of marking • Jeweller’s mark. Outlook Challenges… Despite its huge importance to the economy, the jewellery industry is one of the most heavily regulated industries in India. Take how difficult it has been to secure its raw material; gold. No other industry has had to endure rules as complex and market-distorting as the 80:20 rule. Encouragingly, the policy approach seem to be improving. In November 2014 the 80:20 rule was repealed. And in the 2015 Union Budget a policy framework – including the gold monetisation scheme and Indian gold coin – was established to support India’s gold industry. BIS hallmarks for gold jewellery consist of several componentsFocus box: BIS hallmarking components 916 J ABC The BIS logo A three digit number (out of a set of six predefined values) indicating the purity of the gold in part-per- thousand-format viz; 958, 916, 875, 750, 585, 375 A code denoting the year of hallmarking Logo of the assaying centre Logo/code of the jeweller

- 9. 36India’s gold market: evolution and innovation But the industry still faces some challenges. For a start, small and medium sized manufacturers struggle to obtain gold loans to purchase material. This may change given the introduction of the government’s gold monetisation scheme, which may make it easier for manufacturers to obtain gold loans. More generally, smaller participants in the industry struggle to access credit. For FY2015–16, only Rs727bn was made available to the industry by the financial sector, accounting for just 2.7% of total bank credit.63 This is unlikely to change any time soon. The fragmented nature of the industry means that some parts lack transparency, which makes it hard for banks to complete the due diligence necessary to advance loans. The opacity also hides some shady practices. Stories of banks falling foul of devious jewellery firms who fraudulently obtain loans, and subsequently default, are rife. The gold jewellery industry also suffers from poor infrastructure, largely as a result of it being unorganised and dominated by small, independent retailers and manufacturers. Transport, vaulting, technology and training are weak by international standards. As the sector becomes more organised this will improve. … and opportunities India’s gold jewellery industry is highly fragmented: 70% of retailers and 90%–95% of manufacturers are small, independent firms. But we have seen slow and steady progress in this area. Large regional and national retailers have taken a greater share of the retail market. They seem to have the momentum behind them. By 2020 their share could rise to 35%–40%. And as India’s jewellery export market grows, organised manufacturers should grow too. 63 Industry-wide deployment of Gross Bank Credit from RBI, published on 10 May 2016. By 2020, large regional and national retailers could have become 35%–40%of the market India’s gold jewellery industry can look to other sectors, and indeed other countries, for inspiration. The Bharat Diamond Bourse (BDB) in Mumbai, which opened in 2001, supports industry sourcing, transportation and vaulting. In 2006 a complex in Istanbul, Turkey, called Kuyumcukent – Goldsmiths’ City – began making gold jewellery. Kuyumcukent is the world’s largest integrated goldsmith centre and houses around 2,500 production units and shops, as well as the Istanbul Gold Refinery. We see no reason why India’s gold industry cannot emulate either of these.