Daily iron ore price update (froth gone)

•

1 like•335 views

Australian exports of iron ore to China surged 45.8 percent in April from a year earlier, customs data showed on Wednesday, with the country’s miners pushing ahead with expansion plans to meet demand from the world’s top consumer. Monthly shipments imported by China from Australia reached 47 million tonnes in April, amounting to 56.4 percent of the total volume of 83.39 million tonnes, the second highest on record. The rapid increase came amid weaker iron ore prices, with the country’s miners, including Rio Tinto (Xetra: 855018 – news) and BHP Billiton (NYSE: BBL – news) , all in the middle of plans to expand production capacity on expectations of rising Chinese demand.

Recommended

Recommended

More Related Content

Similar to Daily iron ore price update (froth gone)

Similar to Daily iron ore price update (froth gone) (20)

More from eximbroker

More from eximbroker (20)

Recently uploaded

Recently uploaded (20)

Daily iron ore price update (froth gone)

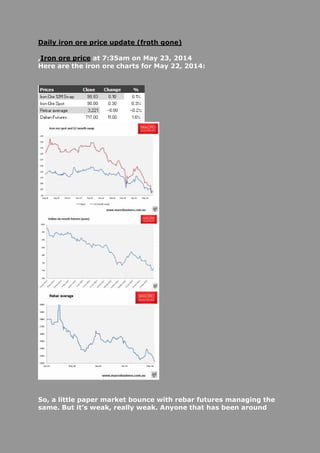

- 1. Daily iron ore price update (froth gone) ,Iron ore price at 7:35am on May 23, 2014 Here are the iron ore charts for May 22, 2014: So, a little paper market bounce with rebar futures managing the same. But it’s weak, really weak. Anyone that has been around

- 2. iron ore markets for any length of time knows how volatile it can be. In old times, if we’d seen the kind of news flow of the past few days – PH strike, India pulling mines offline, rebounding China PMI – we be into a massive paper market short squeeze. This is especially the case since steel mills have been effectively destocking for five months (notwithstanding the port pile). But what we have isn’t even a dead cat bounce, it’s just…splat. Physical is similar with spot barely moving, rebar average still falling an the Baltic Dry capesize component down another 4%. Yet there is no shortage of shipped ore: Australian exports of iron ore to China surged 45.8 percent in April from a year earlier, customs data showed on Wednesday, with the country’s miners pushing ahead with expansion plans to meet demand from the world’s top consumer. Monthly shipments imported by China from Australia reached 47 million tonnes in April, amounting to 56.4 percent of the total volume of 83.39 million tonnes, the second highest on record. The rapid increase came amid weaker iron ore prices, with the country’s miners, including Rio Tinto (Xetra: 855018 – news) and BHP Billiton (NYSE: BBL – news) , all in the middle of plans to expand production capacity on expectations of rising Chinese demand. Perhaps it’s the Chinese lending crimps taking out the marginal trader, or it’s an oversupply born of major miners running flat chat to make up for price falls with volume. And there’s one more possible reason, fromReuters: But Chinese mills are buying some iron ore cargoes after a recent slide in prices. …”Since most of the mills haven’t really cut output, there’s no surprise that they are replenishing their inventory at lower price levels,” said a trader in Shanghai. But tight liquidity and expectation that prices could fall further are limiting purchases to short-term needs. “I don’t think any mill would consider the current price as a solid bottom for iron ore, maybe closer to $90 would be a stronger support.” Mills are replenishing used stocks but not restocking. They clearly don’t expect impending stimulus.

- 3. I’ve argued for some time that the above reasons should combine to kill volatility in the iron ore price as it becomes more of a “real time” delivery system. I’d still expect the Q3 and Q4 destock and restock to happen because they’re in part driven by the seasonal slowing of Chinese activity and Pilbara weather patterns. But beyond that, the froth and bubble appears to be history in the iron ore market. http://www.macrobusiness.com.au/2014/05/daily-iron-ore- price-update-froth-gone/