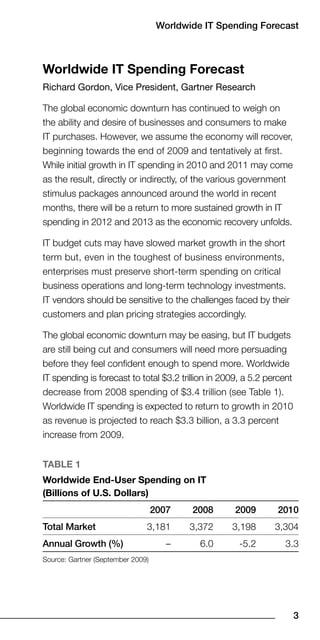

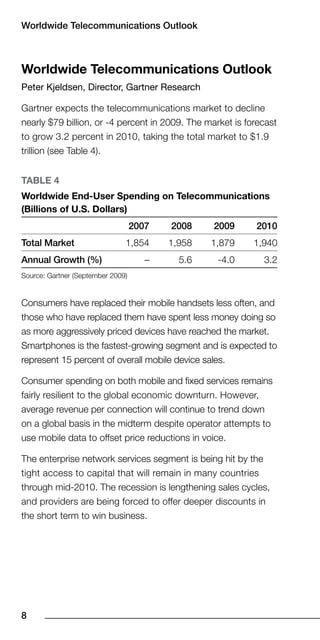

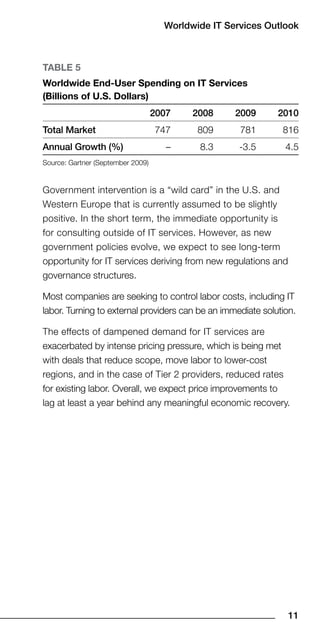

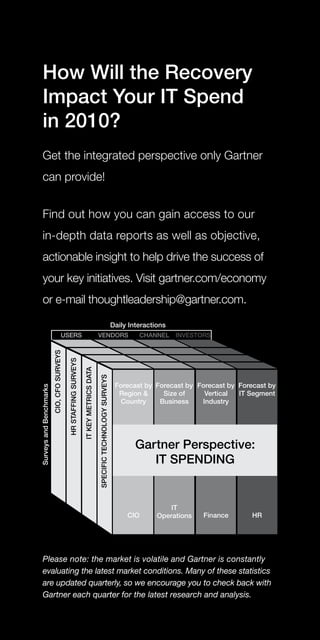

The document discusses the impact of the 2008-2009 economic recession on IT spending, highlighting the recovery expected in 2010. Gartner provides insights into global IT spending trends across various sectors including hardware, software, telecommunications, and IT services, projecting a total of $3.3 trillion in IT spending in 2010. It emphasizes the importance of strategic investment and understanding shifts in customer needs within the evolving economic landscape.