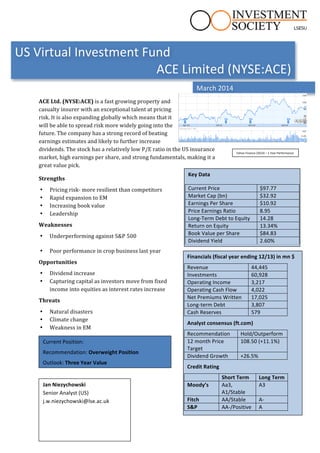

1.

Key

Data

Current

Price

$97.77

Market

Cap

(bn)

$32.92

Earnings

Per

Share

$10.92

Price

Earnings

Ratio

8.95

Long-‐Term

Debt

to

Equity

14.28

Return

on

Equity

13.34%

Book

Value

per

Share

$84.83

Dividend

Yield

2.60%

Current

Position:

Recommendation:

Overweight

Position

Outlook:

Three

Year

Value

Financials

(fiscal

year

ending

12/13)

in

mn

$

Revenue

44,445

Investments

60,928

Operating

Income

3,217

Operating

Cash

Flow

4,022

Net

Premiums

Written

17,025

Long-‐term

Debt

3,807

Cash

Reserves

579

Analyst

consensus

(ft.com)

Recommendation

Hold/Outperform

12

month

Price

Target

108.50

(+11.1%)

Dividend

Growth

+26.5%

Credit

Rating

Short

Term

Long

Term

Moody’s

Aa3,

A1/Stable

A3

Fitch

AA/Stable

A-‐

S&P

AA-‐/Positive

A

ACE

Ltd.

(NYSE:ACE)

is

a

fast

growing

property

and

casualty

insurer

with

an

exceptional

talent

at

pricing

risk.

It

is

also

expanding

globally

which

means

that

it

will

be

able

to

spread

risk

more

widely

going

into

the

future.

The

company

has

a

strong

record

of

beating

earnings

estimates

and

likely

to

further

increase

dividends.

The

stock

has

a

relatively

low

P/E

ratio

in

the

US

insurance

market,

high

earnings

per

share,

and

strong

fundamentals,

making

it

a

great

value

pick.

Strengths

• Pricing

risk-‐

more

resilient

than

competitors

• Rapid

expansion

to

EM

• Increasing

book

value

• Leadership

Weaknesses

• Underperforming

against

S&P

500

• Poor

performance

in

crop

business

last

year

Opportunities

• Dividend

increase

• Capturing

capital

as

investors

move

from

fixed

income

into

equities

as

interest

rates

increase

Threats

• Natural

disasters

• Climate

change

• Weakness

in

EM

March

2014

US

Virtual

Investment

Fund

ACE

Limited

(NYSE:ACE)

Yahoo

Finance

(2014)

–

1

Year

Performance

Jan

Niezychowski

Senior

Analyst

(US)

j.w.niezychowski@lse.ac.uk

2.

1.

Insurance

Sector

Overview

• Companies

in

the

industry

must

brace

for

increased

regulation

in

the

US-‐

focus

may

shift

to

securitised

insurance

risks,

synthetic

investment

portfolios,

etc.

• Net

income

premium

growth

is

increasing

year

on

year

(2012-‐

3.7%,

2013-‐4.5%)-‐

Deloitte

property

and

casualty

insurance

outlook

• Most

successful

businesses

in

2014

will

invest

in

“transformative

technology

with

high

ROI”-‐

EY

2014

US

property

and

casualty

insurance

outlook

• M&A

trends

firmly

downward

from

2008-‐2013

(in

terms

of

price/book

value

as

well

as

deal

value).

• Strong

underwriting

opportunities

in

“pockets

of

opportunity”-‐

need

to

look

at

regional

difference

and

exploit

them

• There

exists

a

greater

focus

on

risk

and

capital

management

in

investments-‐

but

those

who

outperform

will

tap

into

opportunities

in

emerging

economies

Industrial

Sector:

Telecoms

(EU)

Risk

Potential

Sector

Uncertainty

in

emerging

markets

investment

Other

opportunities

remain

in

EM,

such

as

accessing

local

markets

in

M&A

deals

Growth

Regulatory

uncertainty

leaves

US

insurance

market

in

a

holding

pattern,

could

continue

through

2014

Continued

growth

in

net

underwriting

income

may

ease

the

potential

future

cost

of

presenting

more

data

on

risk

exposure

Value

Low

P/E

multiples

in

industry

as

a

whole,

underperforming

S&P

500

Protection

against

asset

bubble

that

may

be

forming?

Underperformance

may

leave

industry

as

great

value

buy

Yield

Dividend

has

been

rising

rapidly

in

the

last

year.

Room

for

much

more?

Underwriting

profits

increasing

as

is

global

expansion,

leaving

more

room

for

increased

dividends

Market

Risk

in

EM

Still

lots

of

potential

in

M&A

deals

a.

Macroeconomic

Drivers

The

main

economic

intuition

for

investing

in

the

insurance

market

is

based

on

a

prediction

that

interest

rates

are

going

to

increase

in

the

near

future.

This

will

shift

fixed

asset

investors

into

equities.

Insurance

companies

may

not

have

the

largest

dividend

yields,

but

stability

is

what

these

investors

will

prefer.

Insurance

companies

also

have

large

capital

investments

in

fixed

income,

which

reduced

the

equity

risk

on

their

performance.

While

investment

gains

are

important,

underwriting

income

growth

typically

drives

the

stocks

in

this

sector,

and

as

the

global

economy

grows,

this

income

will

too

for

international

P&C

insurers.

2.

ACE

Limited

Management

sees

its

Property

&

Casualty

business

divided

in

2

separate

strands:

Global

P&C,

and

Agriculture,

due

to

the

different

nature

of

the

two

business

lines.

3.

a.

Global

Property

and

Casualty

This

includes

the

company’s

Insurance

–

North

American

P&C,

Insurance

–

Overseas

General

and

Global

Reinsurance

segments.

It

is

the

better

performing

part

of

the

business,

and

what

makes

the

company

especially

attractive

for

investors.

The

business’s

spectacular

growth

in

underwriting

income

of

111.2%

this

year

mostly

generated

by

Global

P&C.

It

was

also

due

to

relatively

tame

catastrophe

losses

in

the

year.

Another

factor

was

the

new

M&A

deals,

such

as

the

acquisition

of

a

Mexican

personal

lines

business

which

contributed

to

a

40%

increase

in

the

business.

However,

if

the

effect

of

the

acquisition

is

taken

out,

the

PL

business

still

grew

11%

on

the

year.

b.

Agriculture

The

agriculture

business

line

saw

a

12.5%

reduction

in

net

premiums

written

on

2012.

This

has

been

the

main

struggle

for

the

business

line

for

the

past

two

years.

However

it

was

largely

an

increase

in

the

amount

of

reinsurance

that

the

company

bought.

Lower

commodity

prices

led

to

lower

premiums

(Q4

Earnings

Conference

Call).

3.

Investments

Source:

ACE

2013

Form

10K

Here

we

can

see

how

the

company’s

capital

is

managed.

It

is

a

well-‐diversified

investment

portfolio

consisting

of

fixed

assets,

asset

and

mortgage

backed

securities

as

well

as

short

term

investments.

Additionally,

the

investments

have

considerable

4.

exposure

to

foreign

fixed

income

assets

totalling

$7,255

million.

There

is

however

no

exposure

to

distressed

European

economies

including

Portugal,

Ireland,

Italy,

Greece

and

Spain

as

ACE

looks

for

limited

risk

and

longevity

in

their

investments.

Net

investment

income

totalled

$2.1

billion

which

is

2%

lower

than

2012,

however

is

a

quite

impressive

when

the

environment

of

ultralow

interest

rates

are

factored

in

to

the

performance.

(Q4

2013

Earnings

Conference

Call).

4.

Growth

Prospects

The

company

is

poised

for

future

growth.

M&A

activity

combined

with

solid

fundamentals

are

the

foundation

for

this.

However,

ACE

has

also

been

sowing

the

seeds

for

future

success

by

growing

their

P&C

net

premiums

written

by

almost

20%

just

in

the

last

quarter

of

2013.

This

growth

came

from

across

the

board

of

all

of

all

their

product

lines

(except

agriculture).

a.

Recent

M&A

(i.)

Acquisition

of

ABA

Seguros,

Mexico

In

early

May

2013,

ACE

bought

the

fourth

largest

personal

lines

insurer

in

Mexico

for

approximately

$690

million

in

cash.

This

well

established

company

has

50

year

of

expertise

in

the

Mexican

market.

It

also

shows

ACE’s

commitment

to

conducting

more

business

abroad,

as

this

has

been

a

trend

for

several

years.

This

exposes

the

company

to

wider

global

opportunities

for

growth

and

increases

its

diversification

in

policies.

4.

Competitor

Comparison

Source:

Morningstar.com

5.

a.

Key

indicators

Here

we

can

see

that

ACE

has

a

huge

5

year

revenue

CARG

(compound

annual

growth

rate)

of

7.2%

which

is

more

than

twofold

the

next

highest

among

their

competitors.

This

is

in

spite

of

being

the

biggest

P&C

insurer

(by

market

cap)

already.

The

figure

is

partly

explained

by

ACE’s

M&A

activity,

but

a

large

chuck

of

it

is

also

from

organic

growth

in

underwriting

income.

Even

though

having

posted

large

growth,

ACE

has

a

P/E

ratio

of

just

8.9

which

is

the

second

lower

of

its

competitors.

Another

Impressive

statistic

is

the

company’s

Med

Operating

Margin

which

is

on

the

top

end.

This

is

interesting

as

Evan

Greenberg,

the

CEO

of

ACE

has

said

(Q4

Earning

Conference

Call)

that

the

focus

right

now

is

growth,

and

then

a

widening

of

margins.

This

is

good

news

for

the

firm

and

means

that

there

is

plenty

more

room

for

improvement

in

the

margins

as

the

company

shifts

its

focus

to

this.

The

dividend

has

grown

by

80%

since

the

beginning

of

2012.

The

debt

to

earnings

ratio

is

also

one

of

the

lowest

among

the

group.

b.

Pricing

Risk

ACE

is

exceptional

at

pricing

risk.

This

is

important

in

the

long-‐term

success

of

the

company

as

the

future

is

unpredictable

and

undercutting

the

competition

and

taking

too

much

risk

was,

as

learned

in

the

case

of

AIG,

disastrous.

Source:

ACE

Annual

Report

2012

5.

Portfolio

With

anticipated

increase

in

interest

rates,

investors

in

the

fixed

income

market

will

look

to

shift

into

relatively

high

dividend

equities,

but

ones

that

are

stable

and

perform

more

like

a

fixed

income

asset.

ACE

looks

to

be

a

strong

here

with

a

long

history

of

solid

growth

and

performance.

This

stock

also

looks

attractive

to

investors

looking

to

take

profits

from

overheating

stocks

as

the

DJIA

is

near

historical

highs.

Considering

these

macro

drivers,

the

strong

outlook

for

the

future

growth

of

ACE,

and

the

fact

that

this

is

the

only

asset

with

exposure

to

the

financial

sector,

I

suggest

a

weighting

of

10%

of

the

US

Fund.