More Related Content

Similar to Copy of seasadj.pdf3

Similar to Copy of seasadj.pdf3 (20)

Copy of seasadj.pdf3

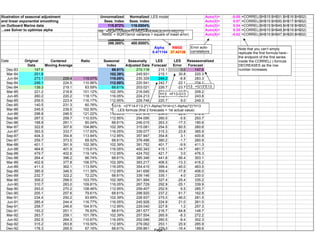

- 1. LES modelIllustration of seasonal adjustment Unnormalized Normalized Auto(1)= -0.05 =CORREL($H$15:$H$51,$H$16:$H$52)

and linear exponential smoothing Seas. Index Seas. Index Auto(2)= 0.07 =CORREL($H$15:$H$50,$H$17:$H$52)

on Outboard Marine data 115.872% 116.0504% Auto(3)= 0.04 =CORREL($H$15:$H$49,$H$18:$H$52)

...use Solver to optimize alpha 112.776% 112.9497% Auto(4)= 0.35 =CORREL($H$15:$H$48,$H$19:$H$52)

68.508% 68.6136% Auto(5)= -0.02 =CORREL($H$15:$H$47,$H$20:$H$52)

102.229% 102.3863%

399.385% 400.0000%

Alpha RMSE

0.471154 27.42136

Date Original Centered Ratio Seasonal Seasonally LES LES Reseasonalized

Data Moving Average Index Adjusted Data Forecast Error Forecast

Dec-83 147.6 68.61% 215.118 215.1 0.0 147.6

Mar-84 251.8 102.39% 245.931 215.1 30.8 220.3

Jun-84 273.1 229.4 119.07% 116.05% 235.329 244.2 -8.8 283.3

Sep-84 249.1 224.5 110.96% 112.95% 220.541 242.7 -22.1 274.1

Dec-84 139.3 219.1 63.59% 68.61% 203.021 226.7 -23.7 155.5

Mar-85 221.2 218.8 101.12% 102.39% 216.045 204.4 11.7 209.2

Jun-85 260.2 220.2 118.17% 116.05% 224.213 210.1 14.1 243.8

Sep-85 259.5 223.4 116.17% 112.95% 229.748 220.7 9.0 249.3

Dec-85 140.5 231.3 60.76% 68.61% 204.770 229.7 -24.9 157.6

Mar-86 245.5 239.5 102.50% 102.39% 239.778 208.7 31.1 213.6

Jun-86 298.8 246.5 121.22% 116.05% 257.474 234.9 22.6 272.6

Sep-86 287.0 259.7 110.53% 112.95% 254.095 260.0 -5.9 293.7

Dec-86 168.8 281.1 60.04% 68.61% 246.015 263.3 -17.3 180.6

Mar-87 322.6 307.6 104.86% 102.39% 315.081 254.5 60.5 260.6

Jun-87 393.5 333.7 117.93% 116.05% 339.077 315.3 23.8 365.9

Sep-87 404.3 354.8 113.94% 112.95% 357.947 354.8 3.1 400.8

Dec-87 259.7 373.5 69.52% 68.61% 378.496 380.2 -1.7 260.9

Mar-88 401.1 391.9 102.36% 102.39% 391.752 401.7 -9.9 411.3

Jun-88 464.6 401.9 115.61% 116.05% 400.343 415.1 -14.7 481.7

Sep-88 479.7 402.6 119.14% 112.95% 424.702 421.7 3.0 476.3

Dec-88 264.4 396.2 66.74% 68.61% 385.346 441.8 -56.4 303.1

Mar-89 402.6 377.8 106.57% 102.39% 393.217 406.5 -13.3 416.2

Jun-89 411.3 362.1 113.59% 116.05% 354.415 399.4 -45.0 463.5

Sep-89 385.9 346.5 111.39% 112.95% 341.656 359.4 -17.8 406.0

Dec-89 232.7 322.2 72.22% 68.61% 339.146 335.1 4.0 230.0

Mar-90 309.2 298.0 103.75% 102.39% 301.994 327.4 -25.4 335.2

Jun-90 310.7 283.0 109.81% 116.05% 267.729 292.9 -25.1 339.9

Sep-90 293.0 270.2 108.46% 112.95% 259.407 252.9 6.5 285.7

Dec-90 205.1 257.6 79.61% 68.61% 298.920 237.2 61.7 162.8

Mar-91 234.4 250.2 93.69% 102.39% 228.937 275.0 -46.0 281.5

Jun-91 285.4 244.4 116.77% 116.05% 245.928 224.9 21.0 261.0

Sep-91 258.7 246.6 104.91% 112.95% 229.040 227.8 1.2 257.3

Dec-91 193.2 251.1 76.93% 68.61% 281.577 216.7 64.8 148.7

Mar-92 263.7 259.1 101.78% 102.39% 257.554 265.9 -8.3 272.2

Jun-92 292.5 264.3 110.67% 116.05% 252.046 260.5 -8.4 302.3

Sep-92 315.2 263.8 119.50% 112.95% 279.062 253.1 25.9 285.9

Dec-92 178.3 265.5 67.16% 68.61% 259.861 276.3 -16.4 189.6

G15: =2*F14-F13-2*(1-Alpha)*H14+((1-Alpha)^2)*H13

....LES formula (first 2 forecasts = 1st actual value)

H13: =F13-G13

I13: =G13*E13

Error auto-

correlations

Note that you can't simply

replicate the first formula here--

the endpoint of the first series

inside the CORREL( ) formula

DECREASES as the row

number increases

H9: =SQRT(VAR(H15:H52)+AVERAGE(H15:H52)^2)

…RMSE = SQRT(error variance + square of mean error)

Page 1

- 2. LES modelMar-93 274.5 265.4 103.42% 102.39% 268.102 265.3 2.8 271.6

Jun-93 295.4 116.05% 254.545 268.8 -14.2 311.9

Sep-93 311.8 112.95% 276.052 256.8 19.2 290.1

Dec-93 68.61% 273.2 273.2 0.0 187.5

Mar-94 102.39% 275.8 275.8 0.0 282.4

Jun-94 116.05% 278.4 278.4 0.0 323.1

Sep-94 112.95% 280.9 280.9 0.0 317.3

Dec-94 68.61% 283.5 283.5 0.0 194.5

Mar-95 102.39% 286.1 286.1 0.0 292.9

Jun-95 116.05% 288.6 288.6 0.0 335.0

Sep-95 112.95% 291.2 291.2 0.0 328.9

F53: =G53

Bootstrapping begins here:

forecasts substituted for data

Page 2