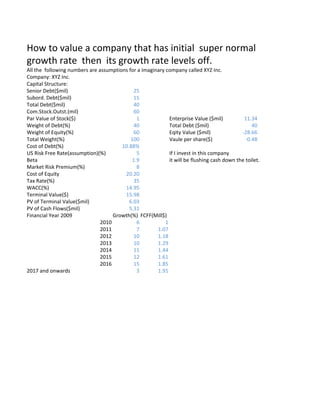

1. How to value a company that has initial super normal

growth rate then its growth rate levels off.

All the following numbers are assumptions for a imaginary company called XYZ Inc.

Company: XYZ Inc.

Capital Structure:

Senior Debt($mil) 25

Subord. Debt($mil) 15

Total Debt($mil) 40

Com.Stock.Outst.(mil) 60

Par Value of Stock($) 1 Enterprise Value ($mil) 11.34

Weight of Debt(%) 40 Total Debt ($mil) 40

Weight of Equity(%) 60 Eqity Value ($mil) -28.66

Total Weight(%) 100 Vaule per share($) -0.48

Cost of Debt(%) 10.88%

US Risk Free Rate(assumption)(%) 5 If I invest in this company

Beta 1.9 it will be flushing cash down the toilet.

Market Risk Premium(%) 8

Cost of Equity 20.20

Tax Rate(%) 35

WACC(%) 14.95

Terminal Value($) 15.98

PV of Terminal Value($mil) 6.03

PV of Cash Flows($mil) 5.31

Financial Year 2009 Growth(%) FCFF(Mill$)

2010 6 1

2011 7 1.07

2012 10 1.18

2013 10 1.29

2014 11 1.44

2015 12 1.61

2016 15 1.85

2017 and onwards 3 1.91