Recommended

More Related Content

What's hot

What's hot (13)

Similar to State Of California Debt Matrix Final

Similar to State Of California Debt Matrix Final (20)

Recently uploaded

Recently uploaded (20)

State Of California Debt Matrix Final

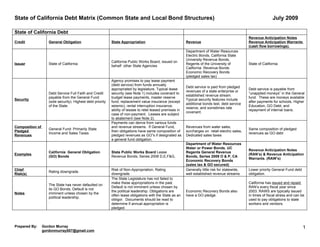

- 1. State of California Debt Matrix (Common State and Local Bond Structures) July 2009 State of California Debt Revenue Anticipation Notes Credit General Obligation State Appropriation Revenue Revenue Anticipation Warrants (cash flow borrowings). Department of Water Resources Electric Bonds, California State University Revenue Bonds, California Public Works Board, issued on Issuer State of California Regents of the University of State of California behalf other State Agencies California Revenue Bonds Economic Recovery Bonds (pledged sales tax) Agency promises to pay lease payment (debt service) from funds annually Debt service is paid from pledged appropriated by legislature. Typical lease Debt service is payable from revenues of a state enterprise or Debt Service Full Faith and Credit security (see Note 1) includes covenant to “unapplied moneys” in the General established revenue stream. payable from the General Fund budget lease payments, master reserve fund. These are moneys available Security Typical security features include (sole security). Highest debt priority fund, replacement value insurance (except after payments for schools, Higher additional bonds test, debt service of the State. seismic), rental interruption insurance, Education, GO Debt, and reserve, and sometimes rate ability of lessee to relet leased premises in repayment of internal loans. covenant. case of non-payment. Leases are subject to abatement (see Note 2). Payments can derive from various funds Composition of and revenue streams. If General Fund, Revenues from water sales, General Fund: Primarily State Same composition of pledged Pledged then obligations have same composition of surcharges on retail electric sales, Income and Sales Taxes revenues as GO debt Revenues pledged revenues as GO”s if designated as Dedicated sales taxes a general fund obligation. Department of Water Resources Water or Power Bonds, UC Revenue Anticipation Notes California General Obligation State Public Works Board Lease Regents General Revenue Examples (RAN’s) & Revenue Anticipation (GO) Bonds Revenue Bonds, Series 2008 D,E,F&G, Bonds, Series 2009 O & P, CA Warrants. (RAW’s) Economic Recovery Bonds (sales tax & GO secured) Chief Risk of Non-Appropriation, Rating Generally little risk for statewide, Lower priority General Fund debt Rating downgrade. Risk(s) downgrade. well established revenue streams. obligation. The State Legislature has not failed to make these appropriations in the past. California has issued and repaid The State has never defaulted on Default is not imminent unless chosen by RAN’s every fiscal year since its GO Bonds. Default is not the political leadership. Obligations are Economic Recovery Bonds also 2003. RAWS are typically issued Notes imminent unless chosen by the often lease obligations with the State as an have a GO pledge. in times of fiscal stress and can be political leadership. obligor. Documents should be read to used to pay obligations to state . determine if annual appropriation is workers and vendors. pledged. Prepared By: Gordon Murray 1 gordonmurray007@gmail.com

- 2. State of California Debt Matrix (Common State and Local Bond Structures) July 2009 City & County Debt Lease Appropriation Debt (Certificates Revenue Bonds & Credit General Obligation Tax Increment Revenue Bonds of Participation – "COP’s") Revenue COP’s City or County or Local Conduit Issuer: City or County Local Conduit Issuer (City or County) Local Redevelopment Agency Issuer Lease obligation (see note 1) debt service payments are subject to annual general Debt service is paid from pledged fund appropriations (inclusion in the Debt service is paid from ad revenues of a city enterprise or budget) by the governmental body. Typical valorem tax revenues levied on established revenue stream. Full Faith and Credit payable from legal provisions: Covenant to budget and incremental taxable value over that Typical security features include the General Fund (sole security) appropriate annual lease payments, debt of a base year in a fixed additional bonds test, debt service Security: secured by unlimited ad valorem service reserve fund, P&C insurance for geographical (project area). reserve, and rate covenant. taxes. Highest debt priority of the replacement value (excluding seismic Bondholder’s lien is not necessarily Revenue COP’s generally have City/County. damage), rental interruption insurance, first lien. Security Provisions similar security features but are Lessor can relet leased premises in case of include additional bonds test and issued by a conduit issuer and are non-payment. Payments may be abated debt service reserve. not abatable. (interrupted) (see note 2) if leased asset is not usable by lessee. Composition of General Fund: Primarily Property Enterprise Funds: Water, Sewer, Taxes derived from a 1% tax on Pledged Taxes (“ad valorem”), Sales Taxes, Same as General Fund Electric, Gas and other utility incremental assessed value (above Revenues and Local Fees & Charges revenues. a base value) in a defined area. City of Los Angeles Department of Water and Power Revenue County Of San Bernardino, California San Jose Redevelopment City of Los Angeles General Bonds, Examples Certificates Of Participation Agency Tax Increment Revenue Obligation Bonds Anaheim Public Financing Auth. (2008 Refunding Program) Series A Bonds Revenue Bonds, Series 2007-A (City Of Anaheim Elec, Sys,.) Thin coverage of tax increment Economic Risk, Commodity Risk, Economic Risk, Risk of Non-Appropriation, bond debt service is vulnerable to Economic Risk, Weather Risk, Customer/Market Chief Risks Risk of Abatement, Political/Management declines in assessed values within Political/Management Risk Concentration, Inability to raise Risk the project area. Taxpayer rates. concentration is another key risk. Tight limits on local General Obligation debt issuance in California make, lease Utility bonds are typically solid New money tax increment debt is financing a ubiquitous form of financing in Default is rare and generally credits in California unless there typically issued up to the maximum Notes California. Failure of an issuer to make recoverable over time. has been a failure to consistently allowed at issue lowering coverage lease payments could damage market increase rates to minimum levels. access to all issuers, even in the case of abatement. Prepared By: Gordon Murray 2 gordonmurray007@gmail.com

- 3. State of California Debt Matrix (Common State and Local Bond Structures) July 2009 School District (USD) and Community College District Debt Tax Increment Lease Appropriation Debt (Certificates of Participation – Revenue Bonds Credit General Obligation “COP’s) Revenue Bonds Revenue COPS Schools do not issue Schools do not issue Issuer: City or County Local or Statewide Conduit Issuer this form of debt this form of debt Lease obligation (debt service) payment is subject to annual general fund appropriations (inclusion in the budget) by the governmental body. Typical legal provisions: Covenant to Full Faith and Credit payable from the budget and appropriate annual lease payments, debt service District General Fund (sole security) Security: reserve fund, P&C insurance for replacement value (excluding secured by unlimited ad valorem taxes. seismic damage), rental interruption insurance, Lessor can Highest debt priority of the District. relet leased premises in case of non-payment. Payments may be abated (interrupted) (see note 2) if leased asset is not usable by lessee. School Districts: Primarily State Aid Composition of 65-75% and Local Property Taxes Pledged 25-35%, Community College Districts: Same as General Fund Revenues Various Proportions of Federal, State and Local Funding. Albany Unified School District Hawthorne School District Certificates of Participation 2007 (Alameda County, California) General Series A, Obligation Bonds Election of 2008, Certificates Of Participation (2006 Financing Project) Examples Series A, Foothill-De Anza Community Evidencing The Fractional Interests Of The Owners Thereof In College District (Santa Clara County, Lease Payments To Be Made By The Foothill-De Anza California) Election of 2006 General Community College District Obligation Bonds, Series A Economic Risk, State Budgetary Cutbacks & Delays, Economic Risk, State Budgetary Political/Management Risk Economic Risk, Chief Risks Cutbacks & Manipulations, Political/Management Risk. Risk of Non-Appropriation, Risk of Political/Management Risk Abatement Tight limits on local General Obligation debt issuance in California make, lease financing a ubiquitous form of financing Default is rare and generally recoverable Notes in California. Failure of an issuer to make lease payments over time. could damage market access to all issuers even in the case of an abatement. Prepared By: Gordon Murray 3 gordonmurray007@gmail.com

- 4. State of California Debt Matrix (Common State and Local Bond Structures) July 2009 Mello Roos Bonds Debt (Special Tax or Special Assessment Bonds) Credit Special Tax or Special Assessment Bonds Community Facility Districts or Community Service Districts are created by Cities, Counties, or School Districts to borrow money to build roads, Issuer: utilities, drainage improvements, and schools to serve real estate development. Issuers are typically small areas within the City, County, or District. “Mello-Roos” is the name of the State law that authorized this form of financing. Annual assessments or taxes paid by property owners. Special taxes and assessments can be annual assessments (up to a maximum amount) for the Security: life of the bonds or limited taxes levied sufficient to pay annual debt service. Security features typically include a debt service reserve. Additional new money bonds, if allowed by bond documents, are often subject to an additional bonds test. Composition of Pledged 100% Special Assessments or Special Taxes, Bond Proceeds, or debt service reserve, Revenues Example Riverside County Community Facility District 89-1 (Mountain Cove) Series 2007 Special Tax Revenue Refunding Bonds Chief Risk Economic risk, tax payer (developer or other) concentration, limited tax base, delinquencies due to developer failure, foreclosure, or illiquid real estate. Mello Roos Bonds vary widely in credit quality based on economic area, seasoning, and local real estate trends. Due diligence is on these bonds highly Notes recommended and can be time consuming. Notes: (1) Lease financing is a structure devised primarily to circumvent debt limitations in certain states. In a California lease structure, the owner (typically a State, City, County or other governmental entity) leases an asset (typically a public building) to a conduit bond issuer. The conduit issues bonds and loans the funds the the owner via a leaseback of the asset. In the leaseback agreement, the owner (the lessee) agrees to pay installment lease payments equal to debt service on the bonds to the lessor (the conduit). (2) Abatement is a typical feature in California lease financings. It requires that installment payments under the lease be stopped if the lessee does not have beneficial use of the leased asset. Mitigants to abatement risk include typical lease features that require 24 months of rental interruption insurance and P&C coverage up to replacement value for all risks except seismic risk. Abatement due seismic risk should be rare due to the building code requirements for most public structures. Prepared By: Gordon Murray 4 gordonmurray007@gmail.com