Recommended

Recommended

More Related Content

Similar to Part a. facts Gibson acquired interest in Keller 112014 Various co.pdf

Similar to Part a. facts Gibson acquired interest in Keller 112014 Various co.pdf (20)

More from feetshoemart

More from feetshoemart (20)

Recently uploaded

Recently uploaded (20)

Part a. facts Gibson acquired interest in Keller 112014 Various co.pdf

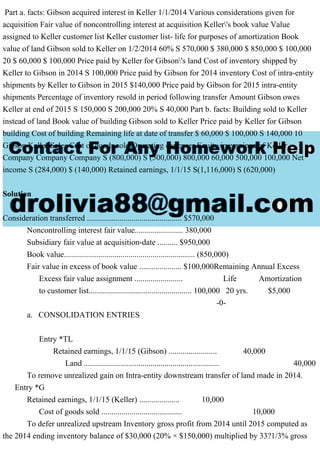

- 1. Part a. facts: Gibson acquired interest in Keller 1/1/2014 Various considerations given for acquisition Fair value of noncontrolling interest at acquisition Keller's book value Value assigned to Keller customer list Keller customer list- life for purposes of amortization Book value of land Gibson sold to Keller on 1/2/2014 60% S 570,000 $ 380,000 $ 850,000 $ 100,000 20 $ 60,000 $ 100,000 Price paid by Keller for Gibson's land Cost of inventory shipped by Keller to Gibson in 2014 S 100,000 Price paid by Gibson for 2014 inventory Cost of intra-entity shipments by Keller to Gibson in 2015 $140,000 Price paid by Gibson for 2015 intra-entity shipments Percentage of inventory resold in period following transfer Amount Gibson owes Keller at end of 2015 S 150,000 S 200,000 20% S 40,000 Part b. facts: Building sold to Keller instead of land Book value of building Gibson sold to Keller Price paid by Keller for Gibson building Cost of building Remaining life at date of transfer $ 60,000 $ 100,000 S 140,000 10 Gibson Keller Sales Cost of goods sold Operating expenses Equity in earnings of Keller Company Company Company S (800,000) S (500,000) 800,000 60,000 500,000 100,000 Net income S (284,000) $ (140,000) Retained earnings, 1/1/15 S(1,116,000) S (620,000) Solution Consideration transferred ............................................... $570,000 Noncontrolling interest fair value........................ 380,000 Subsidiary fair value at acquisition-date .......... $950,000 Book value................................................................. (850,000) Fair value in excess of book value ..................... $100,000Remaining Annual Excess Excess fair value assignment ........................ Life Amortization to customer list................................................... 100,000 20 yrs. $5,000 -0- a. CONSOLIDATION ENTRIES Entry *TL Retained earnings, 1/1/15 (Gibson) ........................ 40,000 Land ................................................................... 40,000 To remove unrealized gain on Intra-entity downstream transfer of land made in 2014. Entry *G Retained earnings, 1/1/15 (Keller) .................... 10,000 Cost of goods sold ........................................ 10,000 To defer unrealized upstream Inventory gross profit from 2014 until 2015 computed as the 2014 ending inventory balance of $30,000 (20% × $150,000) multiplied by 33?1/3% gross

- 2. profit rate ($50,000 ÷ $150,000). Entry *C Retained earnings, 1/1/15 (Gibson) ................. 9,000 Investment in Keller ....................................... 9,000 Parent is applying the partial equity method as can be seen by the amount in the Equity in earnings of Keller Company account (60 percent of the reported balance). Entry S Common stock (Keller) ....................................... 320,000 Additional paid-in capital ................................... 90,000 Retained earnings, 1/1/15 (Keller) (adjusted for Entry *G) ..................................................... 610,000 Investment in Keller (60%) ..................... 612,000 Noncontrolling interest in Keller, 1/1/15 (40%) 408,000 To remove stockholders' equity accounts of Keller and recognize beginning noncontrolling interest. Retained earnings balance has been adjusted in Entry *G. Entry A Customer list.......................................................... 95,000 Investment in Keller ....................................... 57,000 Noncontrolling interest in Keller, 1/1/15 (40%) 38,000 To recognize amount paid within acquisition price for the customer list. Original balance is adjusted for previous year’s amortization. Entry I Equity in earnings of Keller ............................... 84,000 Investment in Keller ....................................... 84,000 To eliminate intra-entity income accrual. Entry D Investment in Keller ............................................. 36,000 Dividends declared ....................................... 36,000 To eliminate intra-entity (60%) dividend transfers.

- 3. Entry E Amortization expense.......................................... 5,000 Customer list ................................................... 5,000 To recognize current period excess amortization expense. Entry P Liabilities................................................................. 40,000 Accounts receivable ..................................... 40,000 To eliminate intra-entity debt. Entry Tl Sales......................................................................... 200,000 Cost of goods sold ........................................ 200,000 To eliminate current year intra-entity inventory transfer Entry G Cost of goods sold .............................................. 12,000 Inventory........................................................... 12,000 To defer 2015 unrealized inventory gross profit. Unrealized gain is the ending inventory of $40,000 (20% of $200,000) multiplied by 30% gross profit rate ($60,000 ÷ $200,000). Net income attributable to noncontrolling interest Keller reported net income ............................................................... $140,000 Excess fair value amortization ......................................................... (5,000) 2014 Intra-entity gross profit realized in 2015 (inventory).......... 10,000 2015 Intra-entity gross profit deferred (inventory) ...................... (12,000) Keller realized net income 2015........................................................ $133,000 Outside ownership percentage ....................................................... 40% Net income attributable to noncontrolling interest ............... $ 53,200 GIBSON AND KELLER Consolidation Worksheet Year Ending December 31, 2015 Consolidation Entries Noncontrolling Consolidated Accounts Gibson Keller Debit Credit Interest Totals

- 4. Sales (800,000) (500,000) (TI) 200,000 (1,100,000) Cost of goods sold 500,000 300,000 (G) 12,000 (*G) 10,000 602,000 (TI) 200,000 Operating expenses 100,000 60,000 (E) 5,000 165,000 Equity in earnings of Keller (84,000) -0- (I) 84,000 -0- Separate company net net income (284,000) (140,000) Consolidated net income (333,000) To noncontrolling interest (53,200) 53,200 To Gibson Company (279,800) RE, 1/1—Gibson (1,116,000) (*TL) 40,000 (1,067,000) (*C) 9,000 RE, 1/1—Keller (620,000) (*G) 10,000 (S) 610,000 Net income (above) (284,000) (140,000) (279,800) Dividends declared 115,000 60,000 (D) 36,000 24,000 115,000 Retained earnings, 12/31 (1,285,000) (700,000) (1,231,800) Cash 177,000 90,000 267,000 Accounts receivable 356,000 410,000 (P) 40,000 726,000 Inventory 440,000 320,000 (G) 12,000 748,000 Investment in Keller 726,000 (D) 36,000 (*C) 9,000 -0-

- 5. (S) 612,000 (I) 84,000 (A) 57,000 Land 180,000 390,000 (*TL) 40,000 530,000 Buildings and equipment (net) 496,000 300,000 796,000 Customer list -0- -0- (A) 95,000 (E) 5,000 90,000 Total assets 2,375,0001,510,0003,157,000 Liabilities (480,000) (400,000) (P) 40,000 (840,000) Common stock (610,000) (320,000) (S) 320,000 (610,000) Additional paid-in capital (90,000) (S) 90,000 Retained earnings, 12/31 (1,285,000) (700,000) (1,231,800) NCI in Keller, 1/1 (S) 408,000 (408,000) (A) 38,000 (38,000) NCIIn Keller, 12/31 (475,200) (475,200) Total liabilities and equity (2,375,000) (1,510,000)1,551,0001,551,000 (3,157,000) b. Entry *TA Retained earnings, 1/1/15 (Gibson) ................. 36,000 Buildings ................................................................ 40,000 Accumulated depreciation .......................... 76,000 To defer unrealized gain ($40,000 original amount less one year of excess depreciation at $4,000 per year) as of beginning of year. Entry *TA (Alternative) Retained earnings, 1/1/15 (Gibson) ................. 36,000

- 6. Buildings (net) ................................................ 36,000 Entry ED Accumulated depreciation ................................ 4,000 Operating (or depreciation) expense ........ 4,000 To remove excess depreciation for current year created by transfer price.