EY Global insurance outlook 2015 summary

•

0 likes•1,129 views

EY Global insurance outlook 2015 summary.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to EY Global insurance outlook 2015 summary

Similar to EY Global insurance outlook 2015 summary (20)

More from EY

More from EY (20)

Recently uploaded

Recently uploaded (20)

EY Global insurance outlook 2015 summary

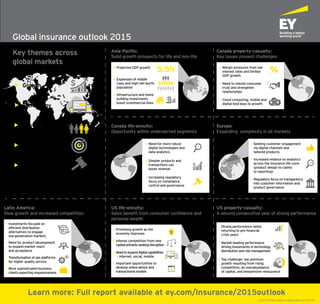

- 1. Asia-Pacific: Solid growth prospects for life and non-life Canada property-casualty: Key issues present challenges Canada life-annuity: Opportunity within underserved segments Simpler products and transactions can boost revenue Increasing regulatory focus on compliance, control and governance Need for more robust digital technologies and data analytics Projected GDP growth Expansion of middle class and high-net-worth population Infrastructure and home building investments boost vcommercial lines 5.5% Margin pressures from low interest rates and limited GDP growth Need to rebuild consumer trust and strengthen relationships Cloud computing, mobile and digital hold keys to growth Latin America: Slow growth and increased competition Europe: Expanding complexity in all markets Investments focused on efficient distribution alternatives to engage low-penetration markets Need for product development to expand market reach and acceptance Transformation of ops platforms for higher quality service More sophisticated business clients expecting responsiveness Growth Technology Customer Transformation Regulation Key themes across global markets US life-annuity: Sales benefit from consumer confidence and personal wealth Promising growth as the economy improves Need to expand digitalcapabilities – internet, social, mobile Important opportunities to develop online advice and transactional models Intense competition from new capitalentrants seeking disruption $ US property-casualty: A second consecutive year of strong performance Strong performance ratios returning to pre-financial crisis years Market-leading performance driving investments in technology, distribution and risk management Top challenge: low premium growth resulting from rising competition, an overabundance of capital, and inexpensive reinsurance Increased reliance on analytics across the insurance life cycle (product design to claims to reporting) Regulatory focus on transparency into customer information and product governance Seeking customer engagement via digital channels and tailored products Learn more: Full report available at ey.com/insurance/2015outlook © 2015 EYGM Limited. All Rights Reserved. EYG No. Global insurance outlook 2015