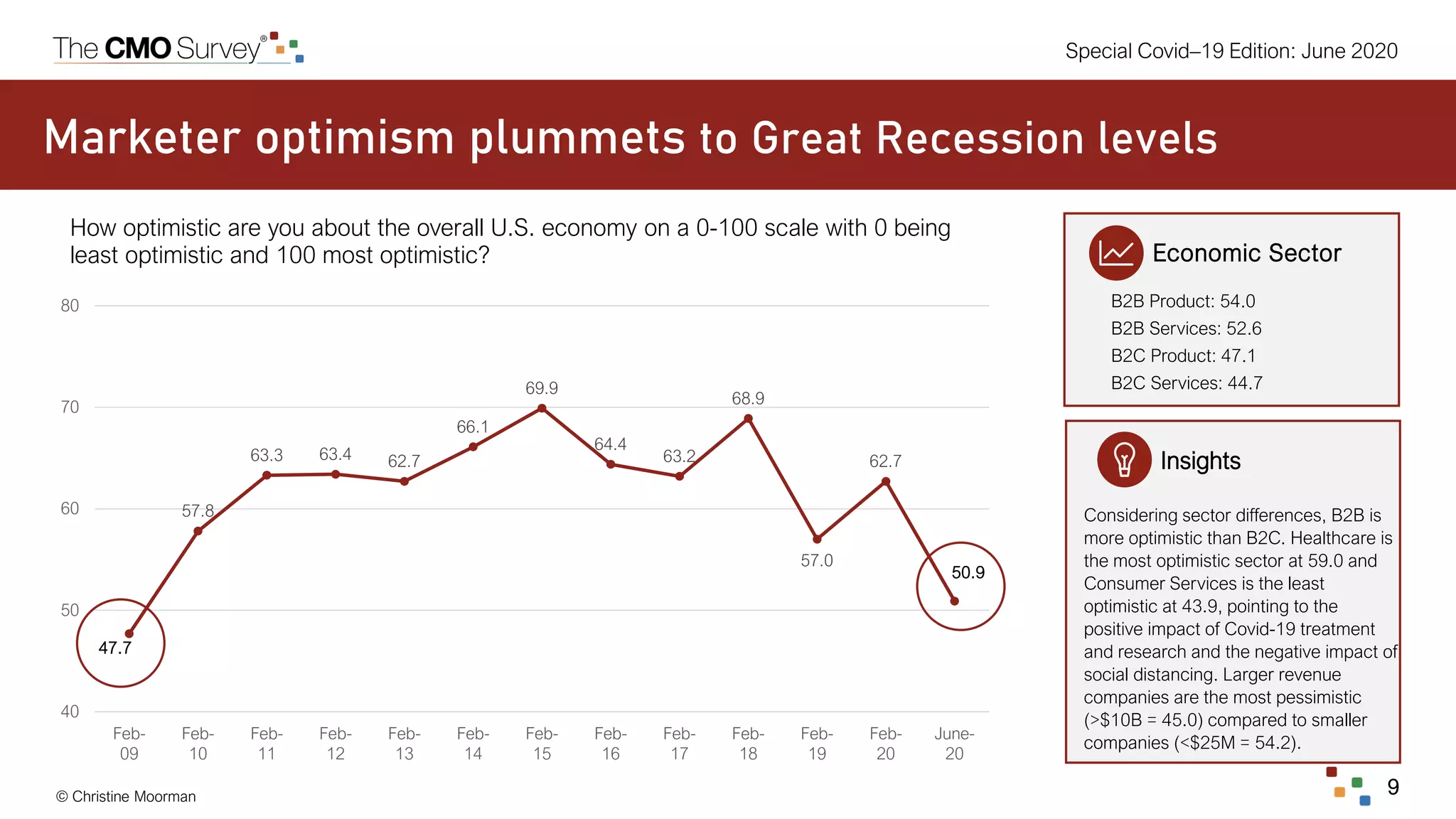

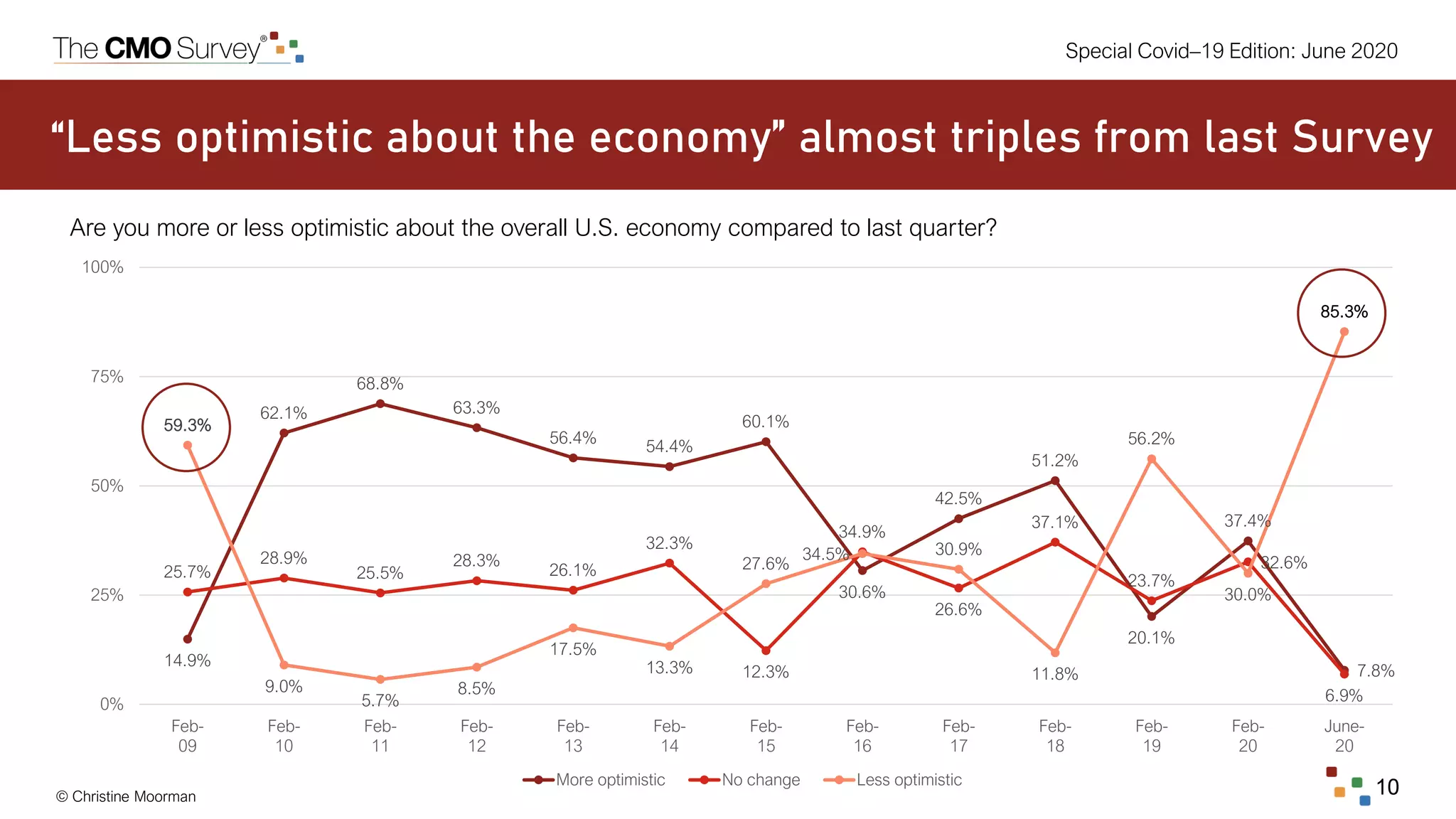

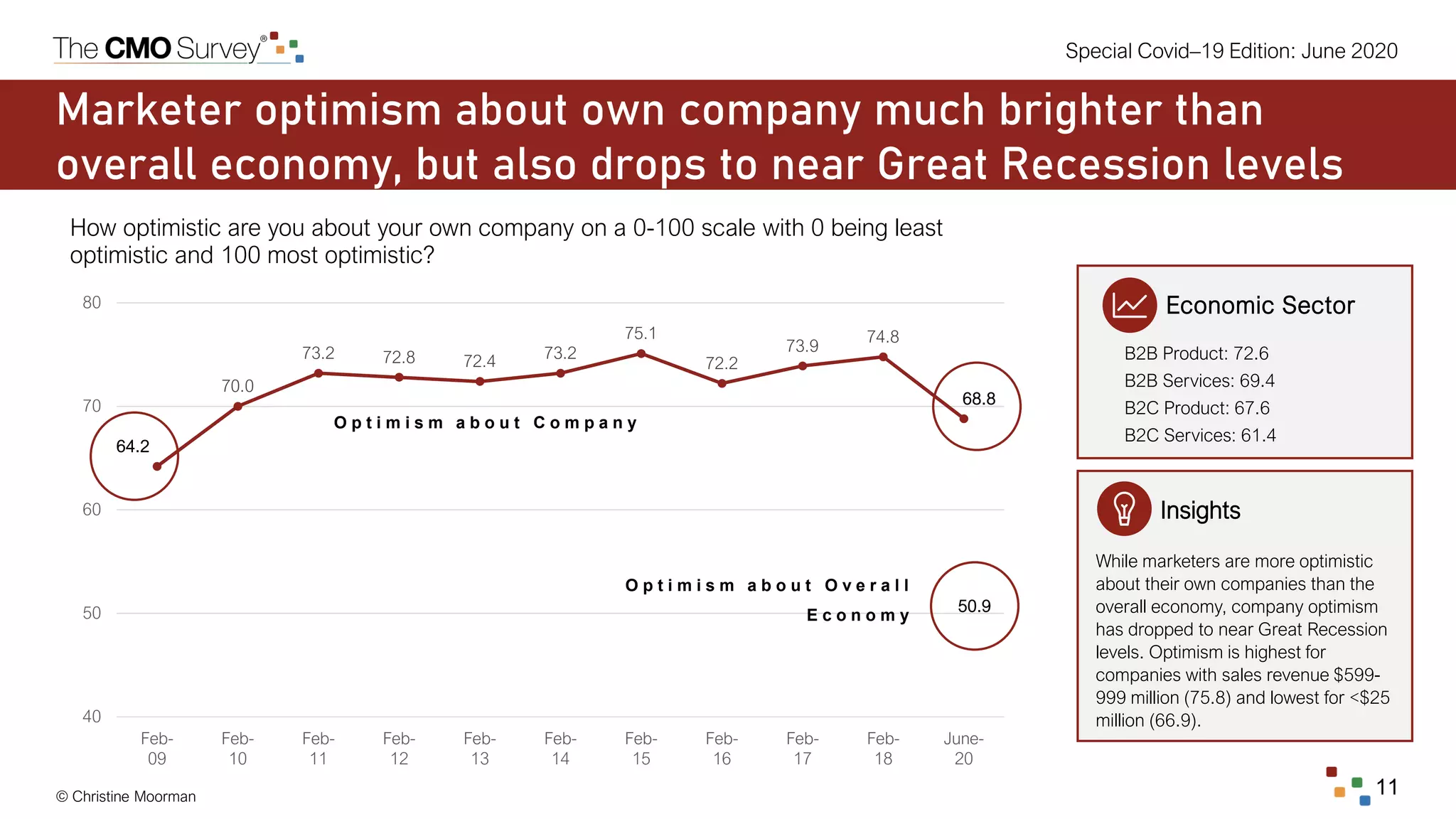

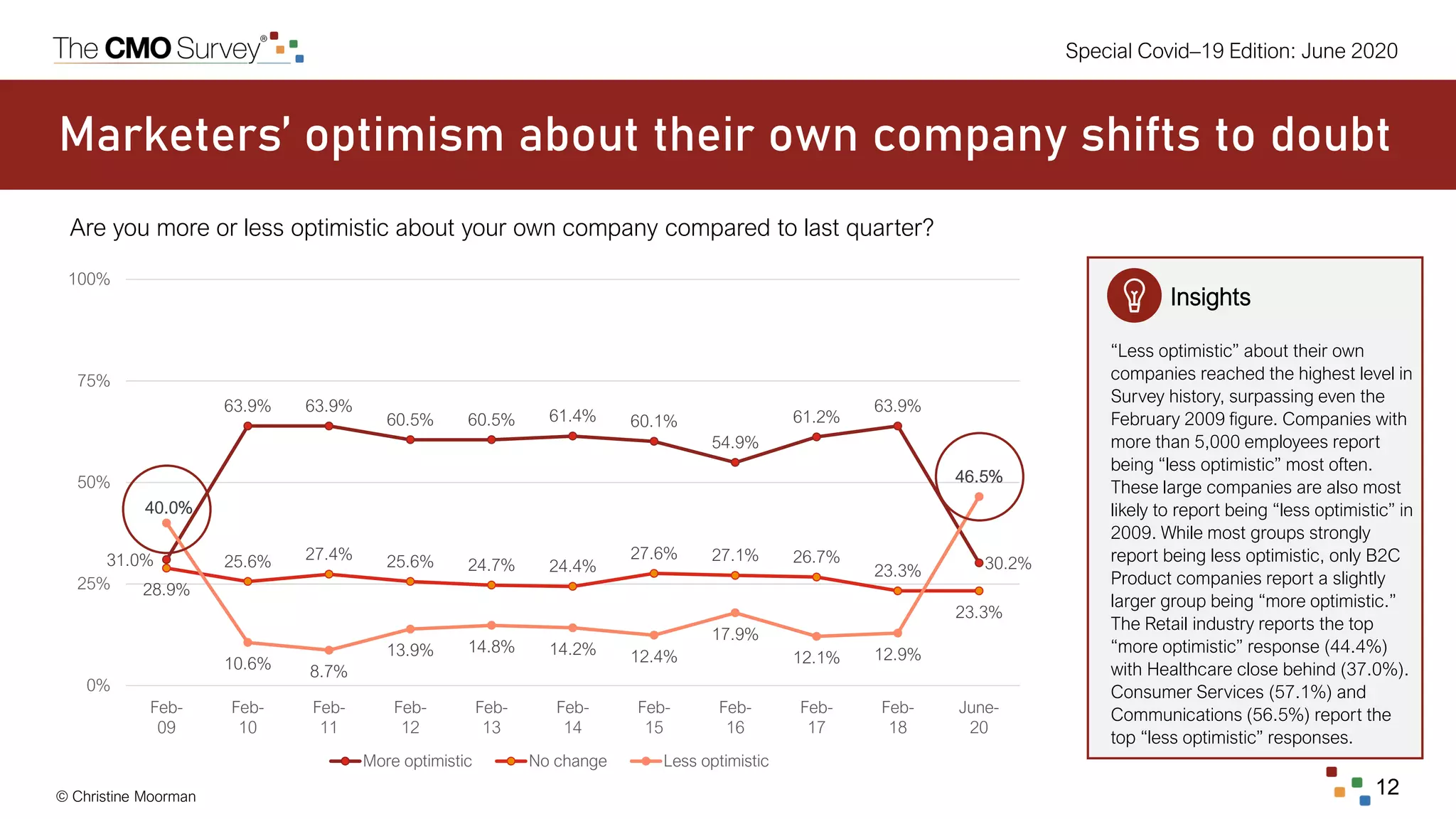

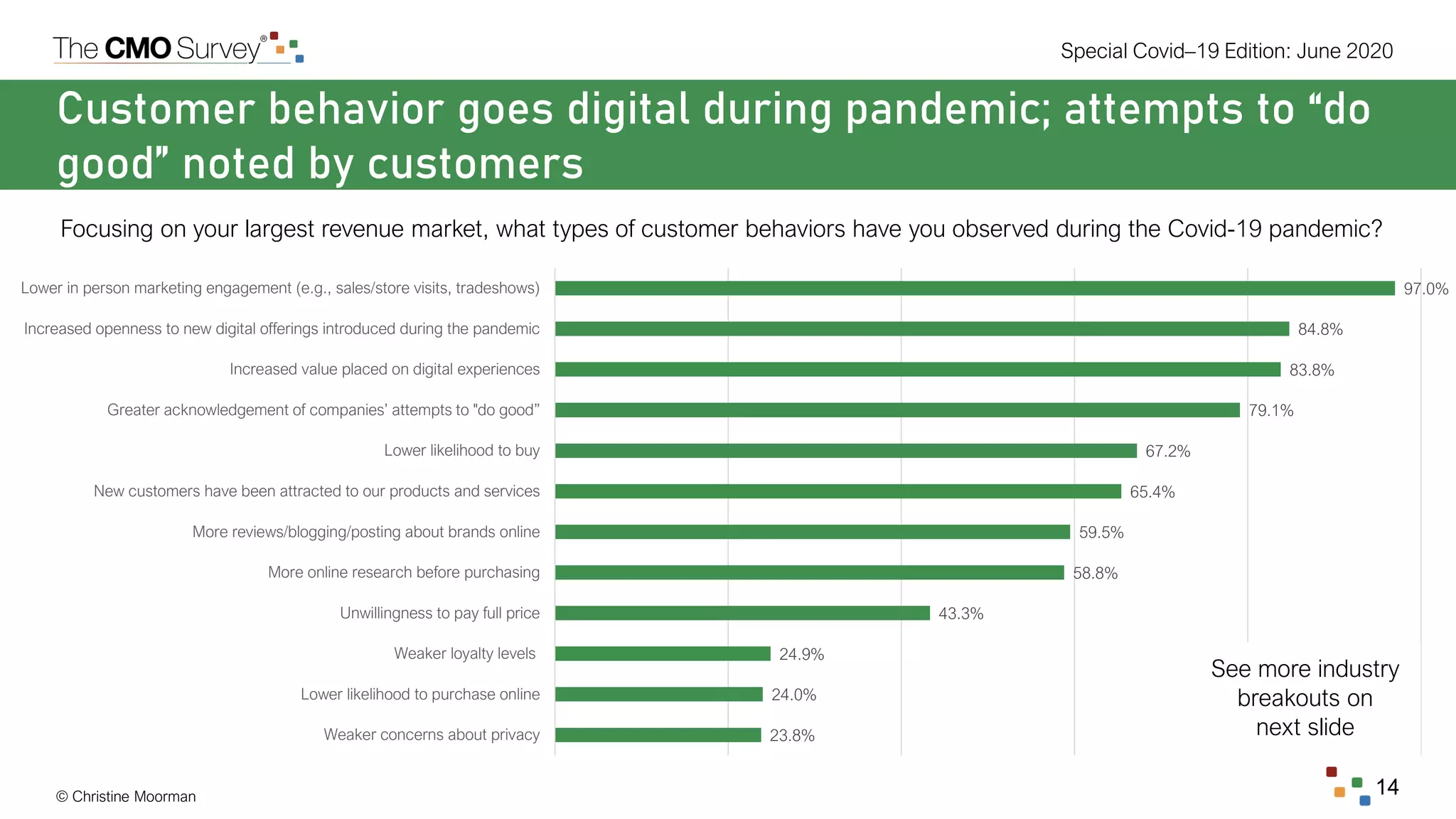

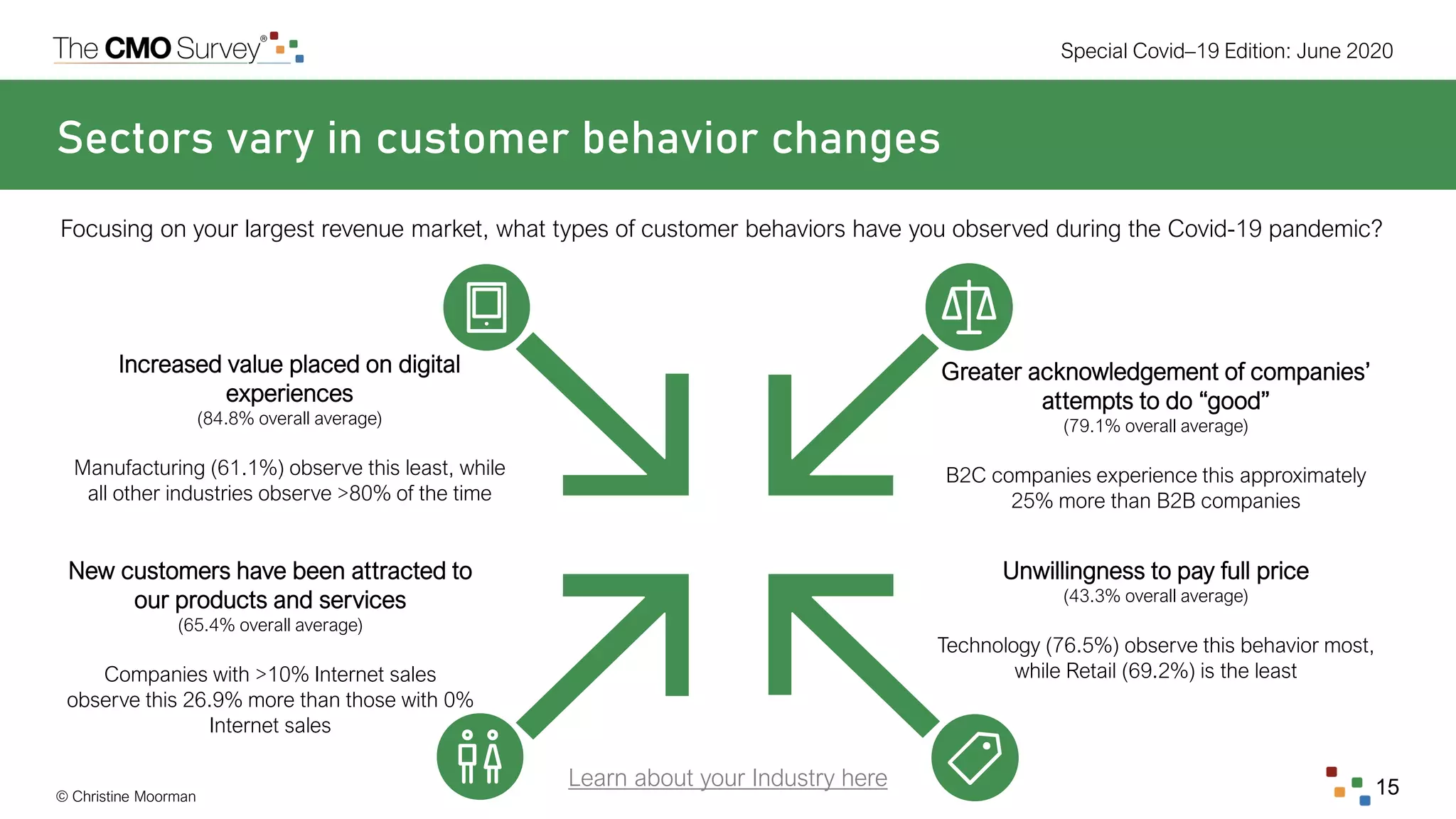

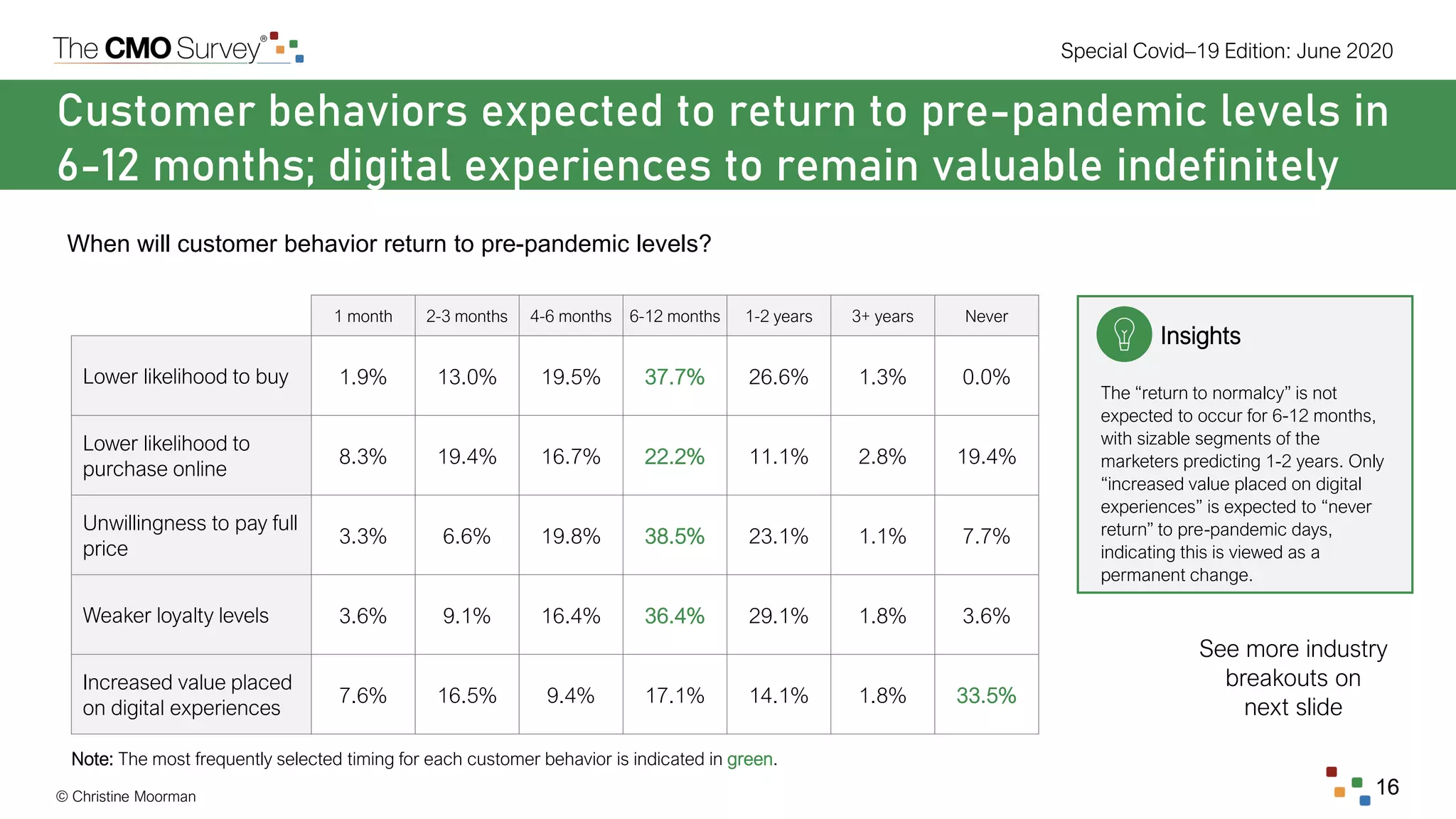

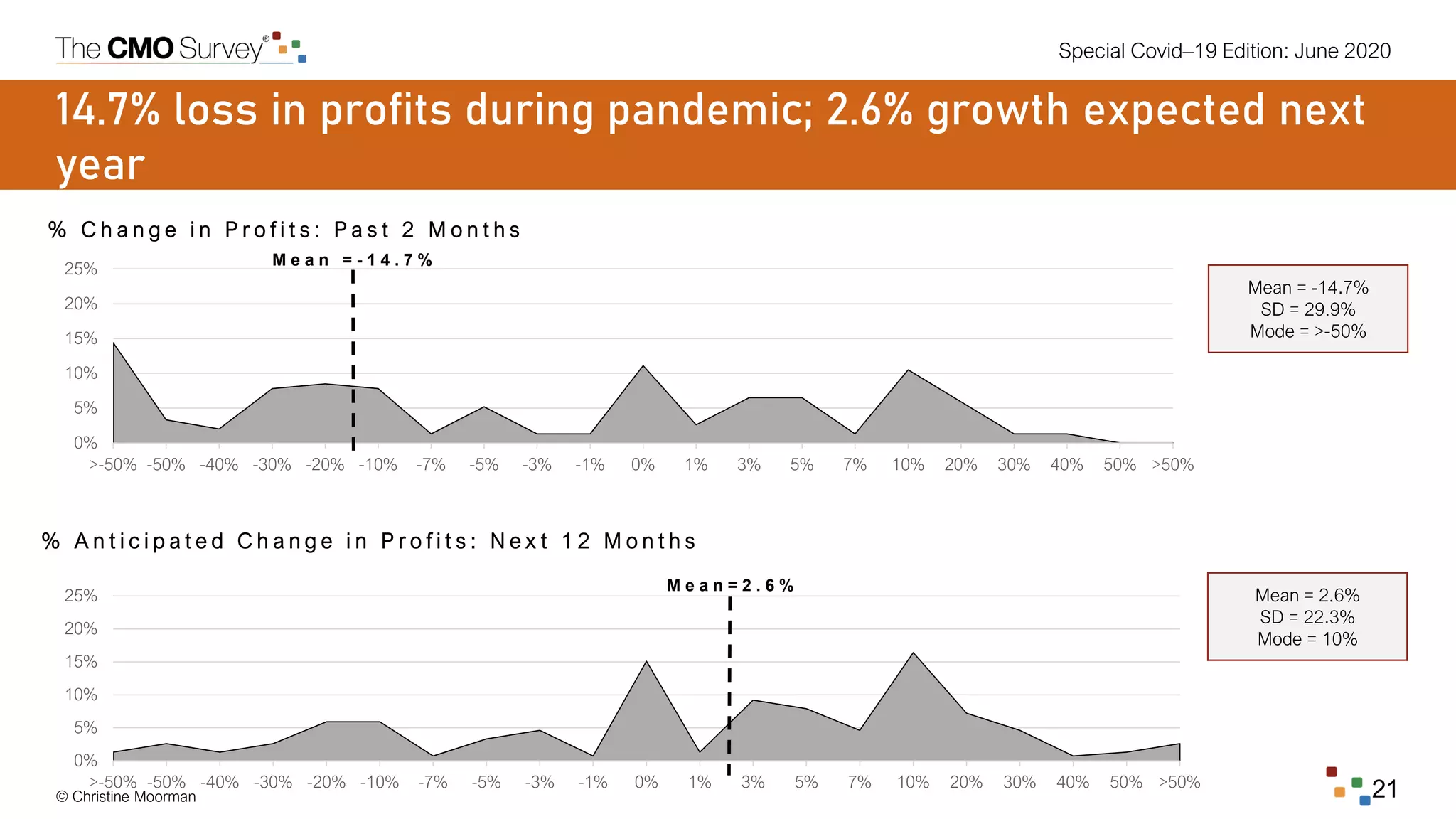

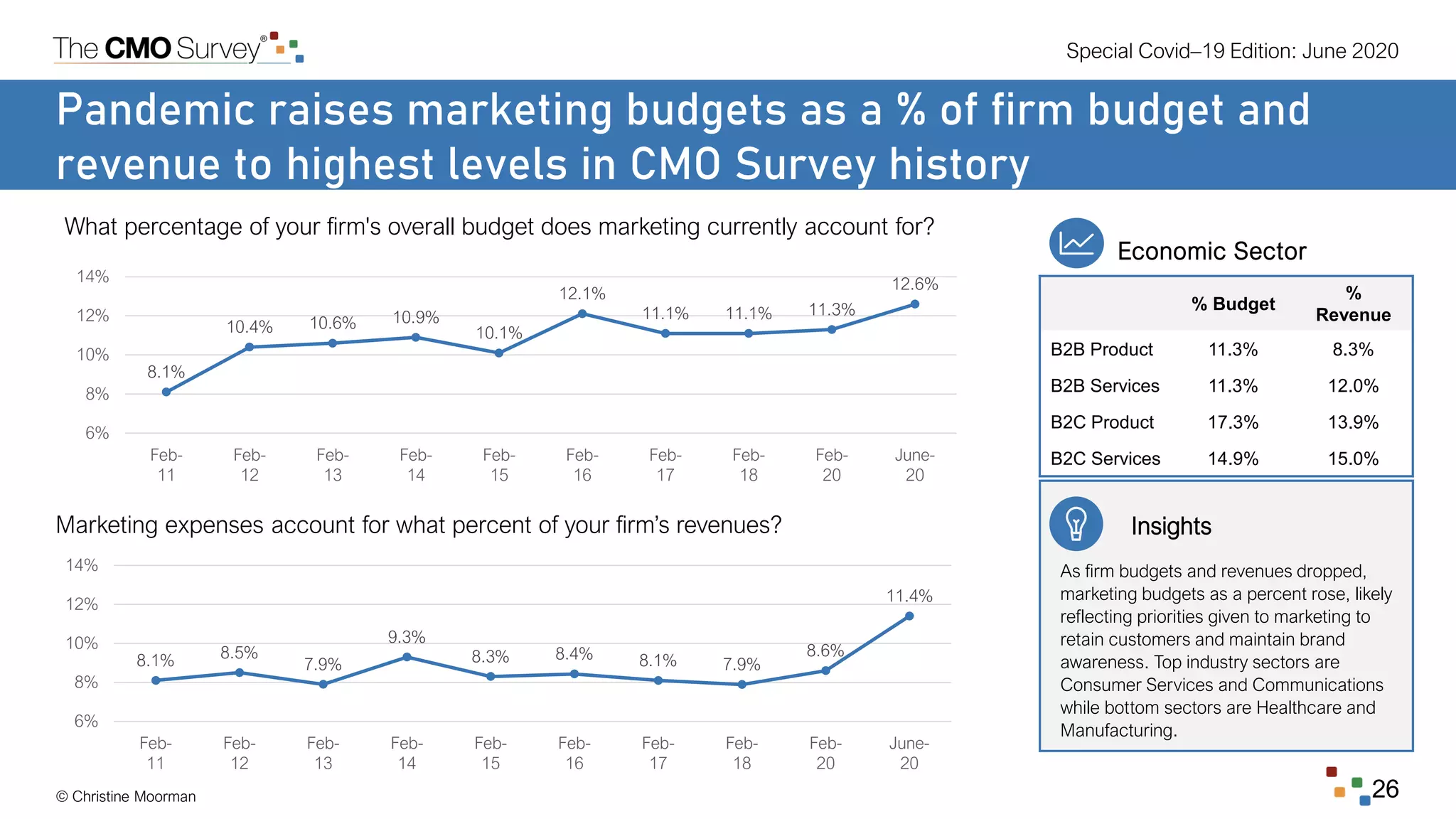

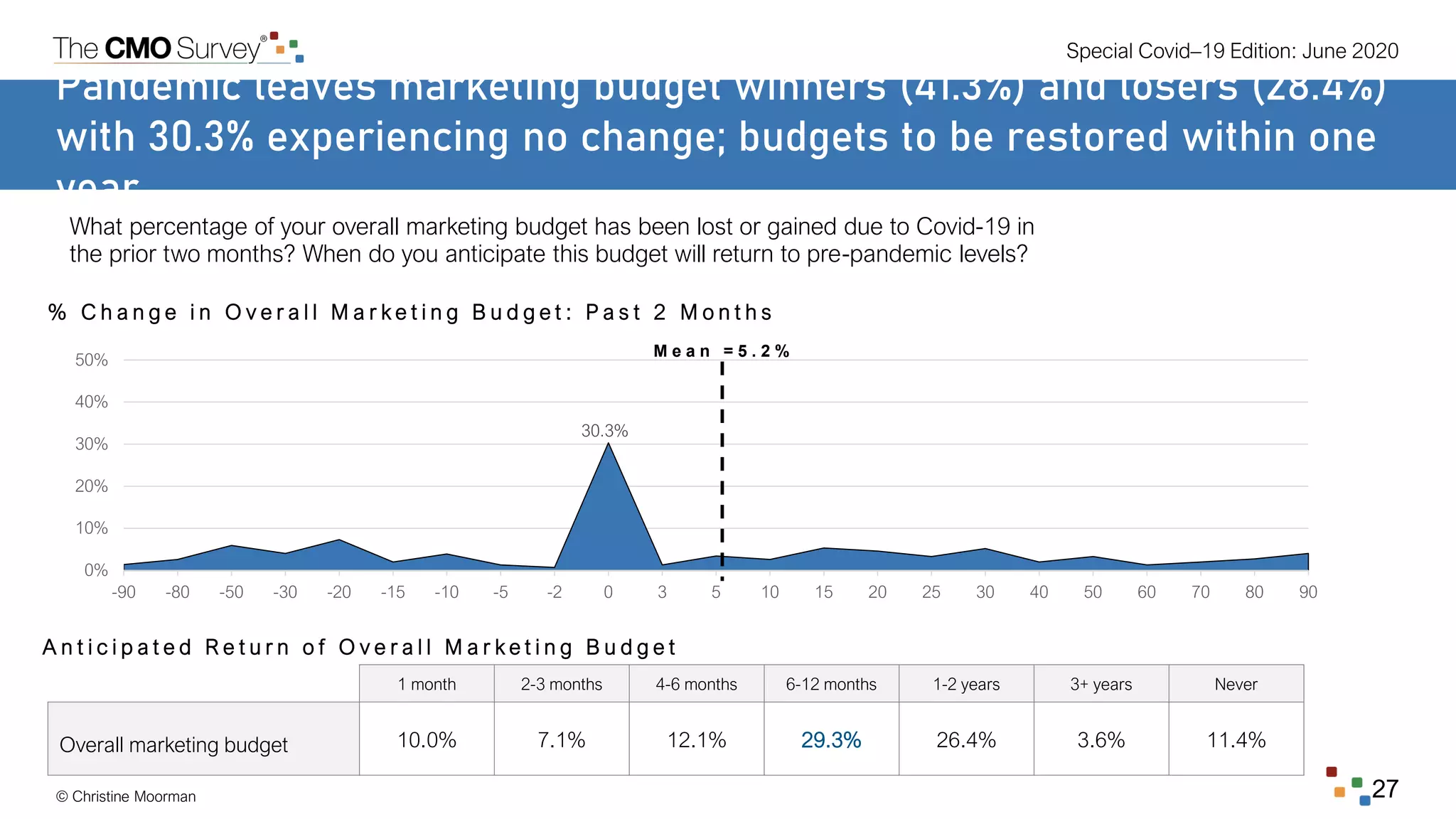

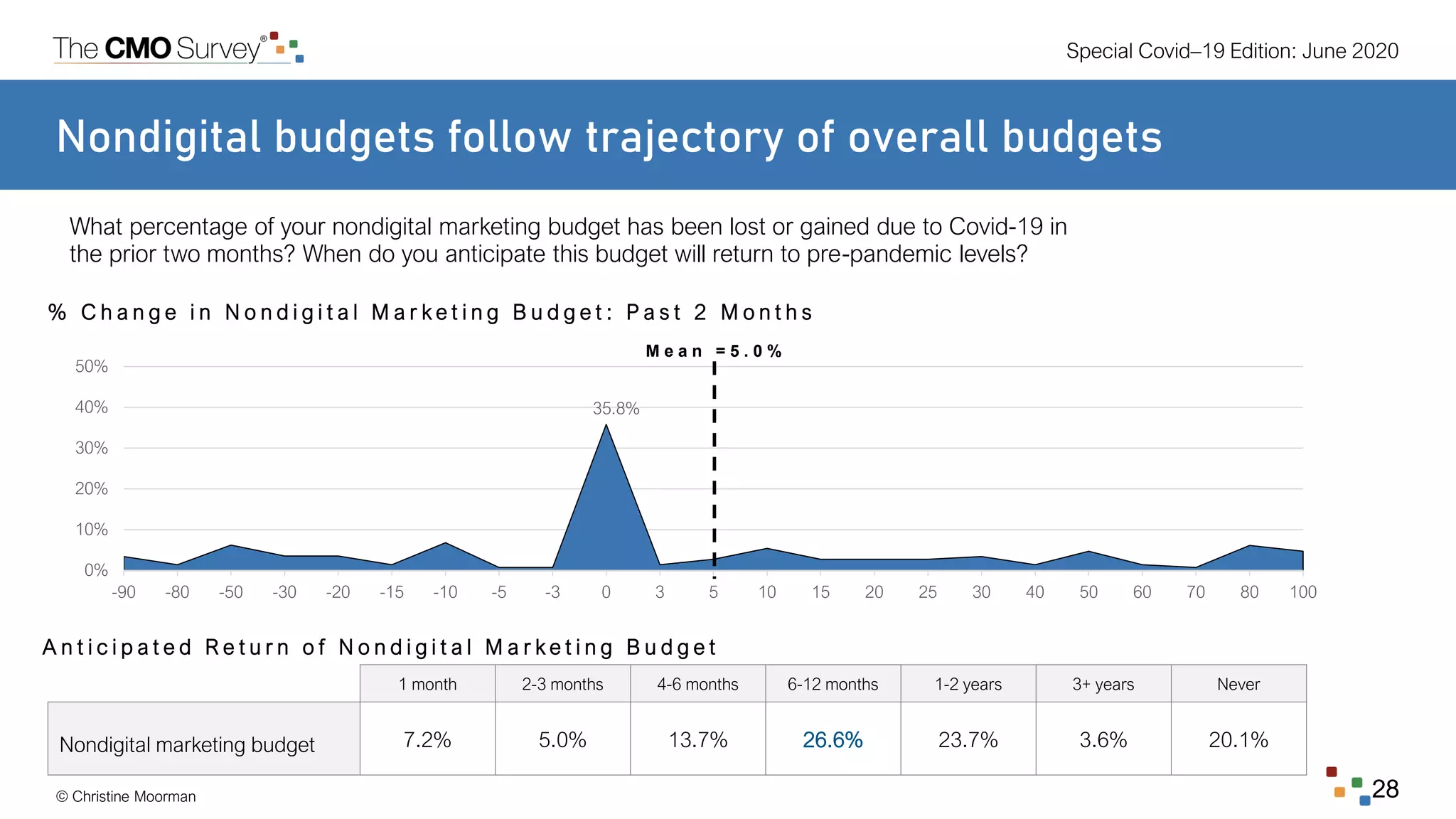

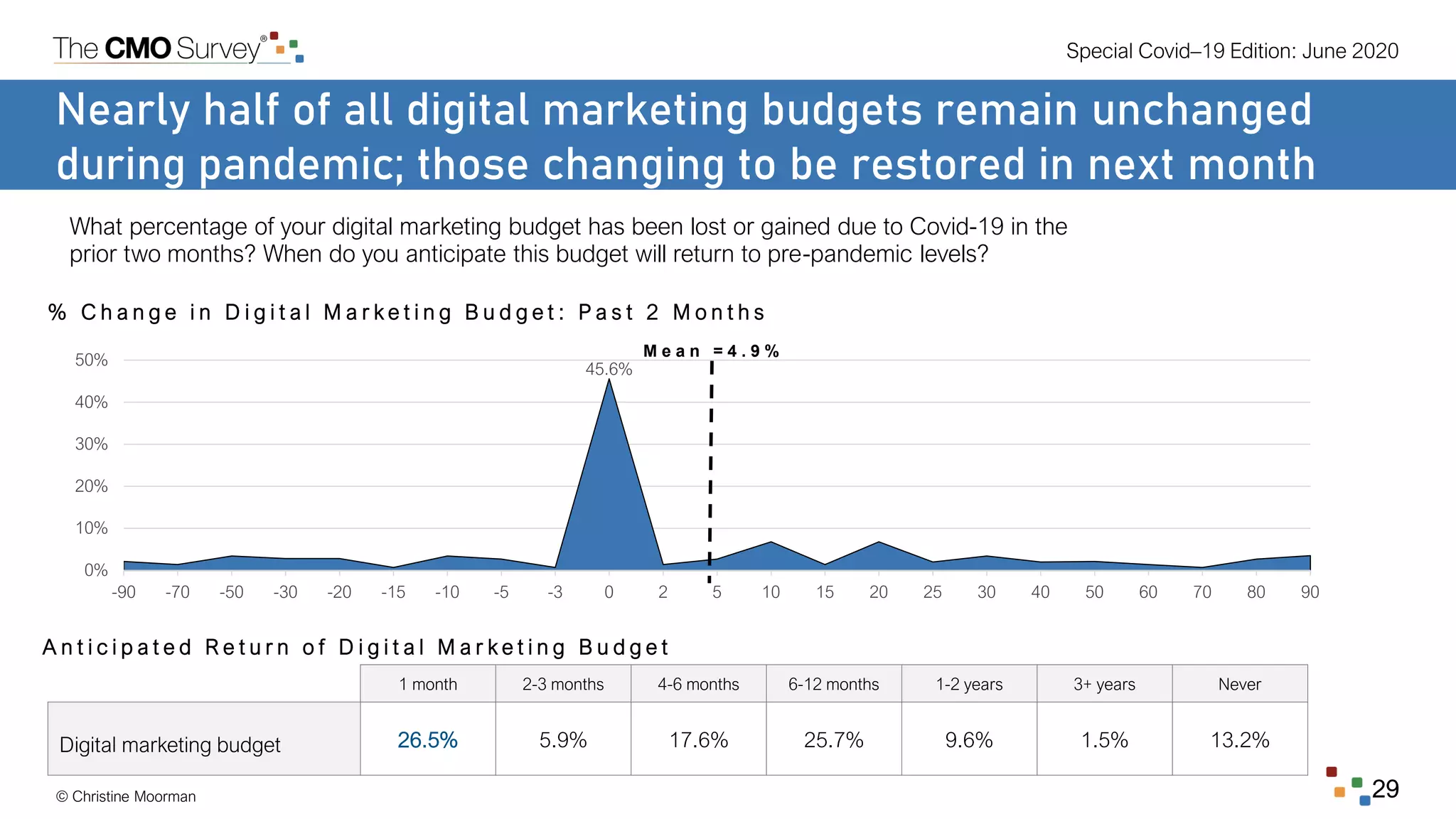

The special edition of the CMO survey from June 2020 explores the significant impact of the COVID-19 pandemic on marketing, highlighting a drop in optimism among marketers to levels comparable to the Great Recession. It reveals shifts in customer behavior towards digital engagement, with increased openness to new digital offerings and a stronger emphasis on companies' social responsibility efforts. The report provides insights into future expectations for marketing performance, spending, and strategies for navigating the ongoing economic challenges.

![The CMO Survey: Highlights and Insights [August 2016]](https://cdn.slidesharecdn.com/ss_thumbnails/thecmosurvey-highlightsandinsights-aug-2016-160823133101-170424115912-thumbnail.jpg?width=640&height=640&fit=bounds)