Download to read offline

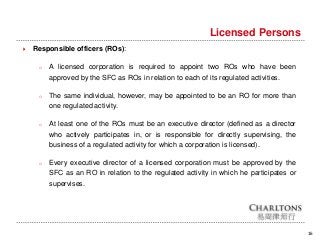

The licensing and registration of persons operating in Hong Kong’s securities and futures market is dealt with in Part V of the Securities and Futures Ordinance (SFO). https://www.charltonslaw.com/hong-kong-law/licensing-regime-in-hong-kong/