1. Page 1 of 31

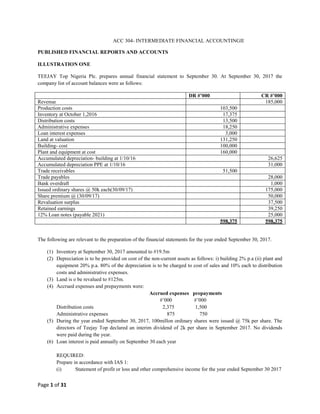

ACC 304- INTERMEDIATE FINANCIAL ACCOUNTINGII

PUBLISHED FINANCIAL REPORTS AND ACCOUNTS

ILLUSTRATION ONE

TEEJAY Top Nigeria Plc. prepares annual financial statement to September 30. At September 30, 2017 the

company list of account balances were as follows:

DR #’000 CR #’000

Revenue 185,000

Production costs 103,500

Inventory at October 1,2016 17,375

Distribution costs 13,500

Administrative expenses 18,250

Loan interest expenses 3,000

Land at valuation 131,250

Building- cost 100,000

Plant and equipment at cost 160,000

Accumulated depreciation- building at 1/10/16 26,625

Accumulated depreciation PPE at 1/10/16 31,000

Trade receivables 51,500

Trade payables 28,000

Bank overdraft 1,000

Issued ordinary shares @ 50k each(30/09/17) 175,000

Share premium @ (30/09/17) 50,000

Revaluation surplus 37,500

Retained earnings 39,250

12% Loan notes (payable 2021) 25,000

598,375 598,375

The following are relevant to the preparation of the financial statements for the year ended September 30, 2017.

(1) Inventory at September 30, 2017 amounted to #19.5m

(2) Depreciation is to be provided on cost of the non-current assets as follows: i) building 2% p.a (ii) plant and

equipment 20% p.a. 80% of the depreciation is to be charged to cost of sales and 10% each to distribution

costs and administrative expenses.

(3) Land is o be revalued to #125m.

(4) Accrued expenses and prepayments were:

Accrued expenses prepayments

#’000 #’000

Distribution costs 2,375 1,500

Administrative expenses 875 750

(5) During the year ended September 30, 2017, 100millon ordinary shares were issued @ 75k per share. The

directors of Teejay Top declared an interim dividend of 2k per share in September 2017. No dividends

were paid during the year.

(6) Loan interest is paid annually on September 30 each year

REQUIRED:

Prepare in accordance with IAS 1:

(i) Statement of profit or loss and other comprehensive income for the year ended September 30 2017

2. Page 2 of 31

(ii) Statement of changes in equity

(iii) Statement of financial position as at September 30 2017.

ILLUSTRATION TWO

The following trial balance has been extracted from the books of LAWANSON PLC as at March 31, 2019.

N’000 N’000

Land at cost 360

Building at cost 750

Equipment at cost 588

Vehicle at cost 852

Goodwill 900

Accumulated depreciation: At April 1, 2018:

Buildings 270

Equipment 228

Vehicles 396

Inventory at April 1, 2018 321

Trade receivables and payables 549 351

Allowance for receivables 24

Bank balances 171

Current taxation 18

Ordinary share of N1 each 600

Retained earnings at April1,2018 1,509

Revenue 4,296

Purchases 1,464

Directors’ fees 450

Wages and salaries 828

General distribution costs 303

General administrative expenses 558

Dividend paid 60

Rent received 90

Disposal of vehicle 30

7,983 7,983

The following information is also available:

1. The company’s non-depreciable land was valued at N on march 31, 2019 and this valuation is to be

incorporated into the accounts for the year ended March, 31 2019.

2. The company’s depreciation policy is as follows: Building, 4% p.a straight line, Equipment, 40% p.a.

reducing balance, Vehicles, 25% p.a. straight line.

In all cases, a full year’s depreciation is charged in the year of disposal. None of the assets had been fully

depreciated by March 31, 2013.

3. On February 1, 2019, a vehicle used entirely for administrative purposes was sold for N30,000. The sale

proceeds were banked and credited to a disposal account, but no other entries were made in relation to this

disposal. The vehicle had cost N132,000 in August 31, 2015. This was the only disposal of a non-current

asset made during the year ended March 31, 2019.

4. . Depreciation is apportioned as follows:

Distribution cost Administrative expenses

Buildings 50% 50%

Equipment 25% 75%

Vehicles 70% 30%

3. Page 3 of 31

5. The company‟s inventory at March 31, 2019 is valued at N357,000.

6. Trade receivables include a debt of N24,000 which is to be written off. The allowance for receivables is to

be adjusted to 4% of the receivables which remain after the debt has been written off.

7. Current tax for the year ended March 31, 2018 was over-estimated by N18,000. The current tax liability for

the year ended March 31, 2019 is estimated to be N90,000.

8. One-quarter of wages and salaries, was paid to the distribution staff and the remaining three-quarters were

paid to the administrative staff.

9. General administrative expenses include bank overdraft interest of N27,000.

Required:

Prepare a statement of profit or loss and other comprehensive income for the year ended March 31, 2019.

ILLUSTRATION THREE

BARAJE NIGERIA PLC has an authorised and issued share capital of #400 million made up of 800 million

ordinary shares of 50k each. The following is the company’s trial balance as at 30th

June 2015.

Trial balance as at 30th

June 2015

DR #’000 CR #’000

Freehold Land 50,000

Short term deposits 100,000

Sundry Receivables 121,640

Cash in hand 21,724

Cash at bank 80,000

Furniture and fittings at cost 89,440

Plant and equipment at cost 328,000

Accumulated depreciation:

Furniture and fittings 22,360

Plant and equipment 65,600

Inventories at 1/7/2014 54,320

Sundry payables 78,840

Bank overdraft 50,000

Wages 194,560

Telephone and postages 4,200

Printing and stationeries 12,120

Auditors remuneration 4,000

Transport and travelling 4,280

Insurance 4,120

Interest paid 8,200

Interest received 2,000

Electricity 7,600

Salaries ( including Directors’ remuneration #2

million)

153,700

Rates 4,280

Purchases 613,664

Revenue/Turnover 1,280,248

Dividends (Interim) 48,000

Statement of comprehensive income 4,800

Share capital 400,000

1,903,848 1,903,848

Additional information:

4. Page 4 of 31

a) The directors recommended that 5% of receivables should be set aside as bad debts

b) Inventories at 30/06/2015 are valued at #57,296,000

c) Unpaid wages at 30/06/2015 amounted to 4,800,000 and electricity accrued was #560,000

d) Depreciation is to be provided as follows: ( i) plant and equipment 10% (ii) Furniture and fittings 5%

e) Sales manager is entitled to sales commission of 2% of gross profit

f) Insurance paid in advanced amounted to #570,000

g) Plant which stood in the book at 1/7/2014 at #16million has been sold for #12 million. in part exchange for

new plant costing #24 million. A new invoice for #12 million had been made in respect of this transaction.

The original cost of the old plant was #20 million. It is the company’s policy to charge a full year’s

depreciation in the year of purchase and non in the year of sale.

h) A final dividend of 8% ( making a total of 20%) was recommended by the directors in respect of the year to

30/06/2015

i) Income tax of 70 million was provided for by the company.

You are required to prepare in a form suitable for publication the following:

1) Statement of comprehensive income for the year ended 30/06/2015.

2) Statement of changes in equity as at 30/062015.

3) Statement of financial position as at 30/062015.

ACCOUNTS OF BANKS

The following is a trial balance of ASIWAJU Bank Nigeria PLC as at 31st

December, 2016.

DR CR

#’000 #’000

Earnings-interest 56,209

Service charges, commission and other fees

4,809

Income on bill of exchange, letters of credit

5,296

Rental income from equipment lease

2,565

Other income

70

Interest paid- Bank in Nigeria

8,442

Others in Nigeria

23,003

Operating expenses

14,734

Taxation

349

Dividend payable

1,000

Accruals

5,741

Interest payable

6,403

Income received in advance

4,139

5. Page 5 of 31

Statutory reserve

4,807

Reserve for bonus issue

3,000

Deposit- Demand

48,711

Time 149,080

Savings 290,603

Money at call and short notice from other banks in Nigeria 126,456

Retained profits

2,759

Freehold premises

16,515

Accumulated depreciation- Premises

2,572

Motor vehicles

7,800

Accumulated depreciation- vehicles

2,700

Furniture and Fittings 5,669

Accumulated depreciation- Furniture

2,669

Equipment on lease

4,500

Accumulated depreciation-equipment

2,360

Ordinary share capital of #1 each fully paid

5,500

113/4% preference share of #1 each fully paid

3,000

Loans and advances

279,124

Provision for doubtful loans and advances

7,164

Interest receivable

7,796

Other receivables

2,544

Prepayment

7,123

Quoted investment

1,000

Cash in hand

40

Balance with central Bank of Nigeria

8,316

Money at call and short notice with other banks in Nigeria

3,821

Balances with other banks outside Nigeria

32,921

Treasury Bills

250,000

Special deposit

59,000

Bills Discounted-payable in Nigeria

6. Page 6 of 31

5,614

Customers’ liabilities and liabilities per contra 150,000 150,000

887,962 887,962

Additional information: All figures are in thousand

(1) Operating expenses included depreciation charge of #3,413, Directors fees of #14 and their salaries #150,

and Auditors’ remuneration of #15.

(2) The loans and advances were made up of:

#’000

Secured against real estate 82,687

Otherwise secured 181,307

Unsecured 15,130

(3) Additional bad debts provision of #6,786 is to be made while #43 is to be written off in respect of

unsecured debts

(4) Provide for: (a) A transfer to reserve bonus issue of #1,500 (b) A proposed dividend of #1,500 on ordinary

shares and dividend payable on the preference shares (c) Income tax at 45% on profits for the year #6,229.

A deferred tax of #593 on the excess of capital allowances, over depreciation charge should be provided

for.

(5) The net external assets at 31st

December,2106 amounted to #30,641

(6) The market value of quoted investments at 31/12/2016 was #975

You are required to prepare the statement of comprehensive income for the year ended 31 D ecember 2016 and

the statement of financial position as on that date in a form suitable for publication.

BANK RUPTCY AND LIQUIDATION

The law relating to bankruptcy is the Bankruptcy Act of 1979. A person who cannot meet his financial liabilities as

and when they fall due is said to be insolvent i.e bankrupt. Before a person can be made bankrupt, he must have

committed an act of bankruptcy.

PEOPLE WHO MAY BE DECLARED BANKRUPT

The following people may be declared bankrupt under the bankruptcy laws:

Debtors who are unable to meet their financial obligations

Partnerships (including limited partnership)

Married women

The estate of the deceased debtors

Undischarged bankrupt (who may be declared bankrupt the second time for debts

incurred after the date of the receiving order in the prior bankruptcy)

PEOPLE WHO MAY NOT BE DECLARED BANKRUPT

Companies incorporated under the Companies and Allied Matters Act CAP C20 LFN

2004

Lunatics

Foreigners having no dwelling house in Nigeria, never resided in Nigeria and has no

business connection in Nigeria

Deceased debtors

THE FOLLOWING ARE DEFAULTS CONSTITUTE ACT OF BANKRUPT

7. Page 7 of 31

1.) If a creditor has obtained judgment of final order against a debtor for any execution

thereon not having been stayed, the debtor has committed an act of bankruptcy. If he

has a bankruptcy notice served on him within 14days and thereafter he does not

comply with the requirements of the notice or satisfy the court that he has counter

claim or set off cross demand which equals to or exceeds the amount of the judgment

debt.

2.) If the execution against the debtor has been levied by the seizure of his goods and the

goods have either been sold or held by the bailiff for 21days

3.) If the debtor flies in the court a declaration of his inability to pay his debts or if he

presents bankruptcy petition against himself.

For a group of creditors or a creditor to present a petition against a debtor, the following conditions must hold:

a.) The debt owed by the debtor to the petitioning creditor(s) must not be less than

₦2,000

b.) The debt must be a liquidated sum payable either immediately or at some certain

future time.

c.) The act of bankruptcy on which the petition is based must have occurred within

3months before the date of petition

d.) The debtor must ordinarily resident in Nigeria or within a year before

The date of petition if the debtor has ordinarily resident in Nigeria or has a dwelling

house or place in Nigeria or has carried out business in Nigeria personally or by

means of an agent

PROCEDURES IN BANKRUPTCY

The under listed are the procedure followed before a person or a partnership business is declared bankrupt.

Presentation of petition

A creditor or a group of creditors present a petition to a Federal High Court of the inability of a debtor to pay

his debts and therefore requesting a receiving order to be made against the debtor. This petition must be

accompanied with a sworn affidavit giving all the required information including the fact that the debtor has

committed an act of bankruptcy.

The Receiving Order

Where the court is satisfied with the creditors’ petition that the debtor has committed an act of bankruptcy, a

receiving order will be made in the newspapers and a receiver is appointed by the court to receive the property

of the debtor. At this stage the debtor though not yet declared bankrupt will maintain the ownership of the

property but the possession and control will be with the receiver.

The Bankruptcy Act 1979 requires that the receiver should be a person appointed as Registrar General of

Companies under the CAMA CAP C20 LFN 2004 and acts as an interim trustee until one is appointed, his

functions include:

To investigate the conduct of the debtor and report to the court stating whether the debtor has

engaged in any misconduct to justify being denied a discharge

To conduct the public examination of the debtor at the public hearing to be held by the court

To protect the assets of the debtor

To manage the assets of the debtor if no special manager is appointed

To convene and preside over the first meeting of the creditors

To manage the business if the debtor in line with the mandate given by the creditor or committee of

inspection

Appointment of a Manager

8. Page 8 of 31

The court may appoint a special manager to manage the estate or business of the debtor and exercise such power as

may be entrusted to him by the official receiver, the manager is only appointed by the court if:

At the instance of the official receiver

If the nature of the estate or business of the receivable necessitates such appointment (too large)

The appointment will be for the overall interest of all the payables

Presentation of statement of affairs

A statement of affairs showing the assets and liabilities of a debtor will be prepared and submitted to the official

receiver within 7days of the receiving order if made on the debtor’s petition, or 14 days if made on the creditor’s

petition

First Meeting of the creditors

The official receiver shall call for the first meeting of the creditors after the court has granted the receiving order.

The meeting shall consider the composition or scheme of arrangement as presented by the insolvent person. An

arrangement is an agreement whereby the debtor agrees that his property be transferred to the trustee to be named by

the creditors and after the satisfaction of the creditor claims, the debtor’s property shall be reassigned to him.

‘Composition’ on the other hand is an agreement whereby the creditors agree to lesser settlement of amounts owed

to them. For any of the alternatives to succeed, two third of the creditors must give their approval but where neither

arrangement nor composition succeeds, the next stage of the proceeding is entered into and that is public

examination.

Public Examination

The insolvent person shall be subjected to a public examination under oath, this is conducted to ascertain the:

a.) Affairs c.) Dealings e.) Causes of failure of the insolvent person

b.) Conducts d.) Property

Such public examination may not be conducted if:

a.) The insolvent is mentally disabled

b.) Physically Disabled or

c.) Not in Nigeria.

With satisfaction that all the affairs of the debtor has been examined and investigated, the court shall make an order

declaring that the public order has been concluded.

Adjudication Order

This is the order of the court declaring the insolvent person bankrupt; in this case he trustee in bankruptcy shall now

legally take possession of the property of the bankrupt and shares this to the creditors in accordance with the

provisions of the Act. The bankrupt person henceforth adds “a bankrupt” after his name.

The adjudication order has the following effect on the bankrupt is that he shall not be eligible for:

Election into public office in Nigeria

Appointment as justice of peace

Admission to practice any profession regulated by law

Appointment as a trustee of a trust estate

Appointment of Trustee in Bankruptcy

When the debtor has been adjudged bankrupt, the creditors may pass an ordinary resolution appointing the official

receiver, a creditor or any other qualified person to act as trustee in bankruptcy, however, the creditors at their own

instance could delegate the responsibility for appointing the trustee in bankruptcy to the committee of inspection.

9. Page 9 of 31

Functions of Trustee in Bankruptcy

Where a trustee in bankruptcy is appointed, his functions will include:

To carry on the business of the bankrupt as far as may be necessary for the beneficial winding up

of the business

To institute or defend the any action or other legal proceedings relating to the property of the

bankrupt

To employ a legal practitioner or other professional or agent to carry out any business as

sanctioned by the committee of inspection

To accept as the consideration for the sale of any property of the bankrupt a sum of money payable

at future time as deemed appropriate

To mortgage or pledge any part of the property of the bankrupt for the purpose of raising money

for the payment of his debts

To take compromise or arrangements with creditors as deemed necessary

To keep proper records on the bankrupt’s estate or business

To divide in its existing form amongst the creditors any property that cannot be readily sold

Records to be kept by the trustee in bankruptcy

Cash book for the receipts and payments

Trading account showing the periodic position of the trading activities

A book to record the administration of the estate of the bankrupt

Discharge Order

The bankrupt person may apply for discharge or the discharge application may be at the instance of the following:

a.) Court c.) Trustee in bankruptcy

b.) Receiver d.) Any of the creditors.

The court shall not grant the order in the following circumstances:

The bankrupt has committed act of bankruptcy

Continues trading after being insolvent

Has previously been adjudged bankrupt

He is guilty of any fraud.

Whatever is the case, the bankrupt person shall be freed of the bankrupt after five years, and this shall free him from

civil rights mentioned under the adjudication order.

Statement of Affairs

Within 7 days if made on debtors’ petition, or within 14 days if made on creditors’ petition, the debtor must prepare

and submit a statement of affairs to the official receiver. This statement, which must be prescribed form and verified

by an affidavit, must set out the assets and liabilities of the debtor.

EXPLANATORY NOTES ON THE PAYABLES:

1. Unsecured Payables

The unsecured payables will rank for payment out of available assets after deducting the preferential payables and

payables for rent, their debt has no any form of security (naked) and these may include the following:

Unsecured bank overdraft facility

Bills payable

Rent not recoverable by power of distrain

10. Page 10 of 31

Wages, PAYE in excess of the ones recognized as preferential

2. Fully Secured Payables

The realizable value of the security is offset against the secured debt and any surplus (a) either transferred to the

assets available to settle preferential creditors and unsecured creditors or (b) transferred to the partially secured debt

if this has a second charge on the assets.

On the other hand the realizable value of the security may be less than the secured debt, the deficiency shall rank for

payment as unsecured creditors.

3. Partly Secured Creditors

The surplus arising from the fully secured debt is used in settling the partly secured creditors and any deficiency

transferred to unsecured creditors.

4. Liability on Bills Discounted

This refers to bills receivable discounted with finance houses and any amount that may rank for payment shall be

transferred to the ‘ranking column’

5. Contingent Liabilities

Any contingent liability other than liability on bills discounted shall be treated like the liability on bills discounted

6. Deferred Debts

They are part of unsecured creditors but their debts shall only be paid after the unsecured creditors, this usually

includes:

Loans by a wife to the husband or vice versa for the purpose of trade

Money paid to the debtor under a contract of apprenticeship

An amount due to the vendor of a goodwill sold to the debtor

The sum owed by a partnership firm to any of the partners

Sums borrowed to the debtor for use in his business which attracts share of the profit of the debtor

instead of the normal interest on loan

7. Payables for rents

The landlord has the right to exercise the power of distrain for any rent owed to him before the commencement of

bankruptcy. However if he distrains after the commencement of the bankruptcy, he is only entitled to six months’

rent and the balance shall be considered as unsecured creditors.

8. Preferential Payables

This shall be met directly from the assets realized; the amount involved is only shown on the liability side only to

disclose the gross liabilities it can never rank for payment as the unsecured creditors. Preferential creditors include

the following:

Local rates due 12months before the receiving order

All taxes assesses on the debtor before the receiving order, where there are arrears, the highest

amount of 12 months before the receiving order is chosen as preferential the remaining liabilities

transferred to unsecured creditors.

All PAYE deductions of 12 months before the receiving order and the highest amount being

preferential where many assessment years are involved, the remaining liabilities thrown to the

unsecured creditors

Any VAT outstanding of 12 months before the receiving order

11. Page 11 of 31

Wages or salaries of any clerk, servant or workman for a maximum of 4 months but not exceeding

₦300 per employee. This shall also include all holiday remunerations and sick pay owed to the

servants, clerks and workman

All accrued holiday or bonus payable to the clerks, servants on termination of employment by

reasons of death or receiving the order

reasonable

ILLUSTRATION ONE

The following information relates to BAWASA

N000 Assets N000

Liabilities

Capital 25,000 Freehold premises 50,000

Profit for the year 10,000 Furniture & equip 37,500

35,000 Inventory 12,500

Less drawings 5,000 Current Assets

30,000 Trade receivables 17,500

Trade payables 54,000 Bank 3,000

Bank O/D (secured on freehold premises)37,500 Cash in hand 1,000

121,500 121,500

Additional information

I. The business of BAWASA are estimated as follows: freehold #65,000,000, furniture& equipment

#9,000,000, trade receivables #13,500,000, bank balance #3,000

II. Trade payables included an amount of #3, 750,000 regarded as preferential.

III. BAWASA personal asset include a motor car valued at #5,000,000. A saving account maintain with MFR

ltd standing at #1,875,000. A plasma TV valued at #875,000. His personal liabilities were #500,000 due to

staff and #1,250,000 for unsuccessful football forecast due to his pooled agent.

IV. The value of his asset and liabilities remain unchanged.

You are required to prepare as at 31st

December 2009

(1) Statement of affairs (2) Deficiency/surplus account

ILLUSTRATION TWO

From the following information prepare the statement of affairs of Musa and Okoro as at 30/6/2003 who have just

been declared bankrupt.

Plant and machinery(#30,000)expected to realize #25,000,inventory in trade (12,000)expected to produce #7000,

patent right (#5000)expected to produce #3000,furniture and fittings (#625),expected to realize #400,cash in hand

#10,cash at bank #120,bills receivable #2514(Good),bills payable #4035,loan #20,000 having a first charge on plant

12. Page 12 of 31

and machinery,liabilities for damages awarded for injured workers under workmen compensation act covered by

insurance Act #100,payabless #33,406,#8,000 of which have a second charge on plant and machinery rent owing for

one year #620,rates #85 preferential wages and salaries#80,trade receivables #10,816(Good #7,068 subject to 5%

discount)doubtful #2020,expected to produce 25% and the remaining is bad. .Liability of bills discounted #1856 of

which #104 is expected to rank. .

Musa private estate shows an expected surplus of #60 while okoro estate shows a deficiency of #146.capital as

commencement of business is #10,000. Trading for the years are as follows:

Year1 Profit of #1,160.

Year2 A loss of #1,857.

Year3 Profit of #587.

Year4 Profit of #316.

Year5 Loss of #2,872.

Drawings:

Musa #900 per year

Okoro#500 per year

The above Profit or Loss figures are arrived at after charging interest on capital at #500 per year

Required: prepare a statement of affairs and deficiency as at these dates

ILLUSTRATION THREE

The following information relates Mr Adamu (The bankrupt)

Unsecured creditors:

Bills payable 3,713,500

Sundry debt 257,680

Trading account 18,074,580

Fully secured creditors 16,000,000

Secured on the security estimated to realize 18,000,000.

Liabilities on bills discounted #1,115,460, expected to rank 107,020

Payables for unpaid rent ( preferential )#200,000.

Preferential for rent, taxes and wages#245,460

Furniture and fittings (estimated to realize #1,200,000),#2,161,280

Cash in hand 21,260

13. Page 13 of 31

Cash at bank 120,580

inventory in trade{estimated to realise (5,000,000)} 8,121,820

Household, furniture& fittings (estimated to realize 440,000) 901,060

Book debt: Good 5,357,540

Doubtful (1,053,160 ) expected to realize half of the amount.

Bad 775,480

Bills of exchange 475,820

Reqd: Draw up a statement of affairs to be presented to the creditors of the Adamu

ILLUSTRATION FOUR

(a) OMO AGEGE commenced business on 1, January 2010 with a capital of #672m. His

profits for the years to 2014 were #80m; #64m; #36m; #28m and #8m respectively. His

drawings averaged #44m per annum. On 31 December, 2014 a receiving order was made

against him when his affairs were as follows:

#’000

Unsecured payables 400,000

Mortgage on freehold property 80,000

Payables partly secured (life policy estimated to realise #80m) 240,000

Payables for salaries and wages 9,600

Bill receivable discounted and expected to rank 6,400

Plant and machinery (costs #160m) estimated to realise 40,000

Freehold factory (costs #800m) estimated to realise 400,000

Book debts: Good

Doubtful (#40m) to realise

Bad

120,000

12,000,

100,000

Furniture and fittings (costs #16m) estimated to realise 7,000

Inventory (costs #160m) estimated to realise 111,000

Cash in hand 1, 600

You are required to prepare a Statement of affairs and a deficiency/surplus account from the

above information. 8 marks

b i. List three modes of company liquidation (3 Marks)

ii. An undischarged bankrupt may suffer from some legal disabilities. State FOUR of them.

(4 Marks)

RECEIVERSHIP AND LIQUIDATION

14. Page 14 of 31

RECEIVERSHIP

A company or part of a company property may be put under receivership which means the receiver receives the

whole of the company from the management if appointed as a receiver for the whole company or he receives part of

the company’s property if his appointment is restricted to only a part of the company’s property.

Appointment of a receiver manager

Receiver and managers can be appointed either under a power contained in an instrument or by the court.

Appointment by the court

The court may on the application of a person interested, appoint a receiver or receiver and manager of the property

or undertaking of a company if:

The principal money borrowed by the company or the interest is in arrears or

The security or property of the company is in jeopardy S389(1) of CAMA CAP LFN2004

The court has an inherent jurisdiction to appoint a receiver in order to put property in safe hands until the right of

those interested in t can be determined.

Appointment out of Court

By far the most common type of the encountered in the business world arises as a result of an agreement. This type

of agreement is usually one entered into by a company which wishes to borrow money to sue in its business and as a

security for the loan, is prepared to agree that the lender be given the right, in the event of the borrower failing to

adhere to the terms of the loan agreement, of appointing a receiver to take over assets of the company with the main

objective of securing to the lender the repayment of the outstanding loan.

It is to be noted that by S181 of CAMA CAP C20 LFN 2004 that the holder of a fixed charge can only appoint a

receiver whose mandate is to take custody of the specific asset and realize this for the benefit of the debenture

holders. In the same vein, only the holder of a floating charge or a combination of fixed and floating charge may

appoint a receiver and manager, a receiver appointed manager has the power to carry on any business or undertaking

of the company under receivership.

Disqualification from appointment as a receiver

S 387 of CAMA CAP C20 LFN 2004 disqualifies the following from appointment as a receiver:

An infant

Any person of unsound mind

A body corporate

An undischarged bankrupt

A director or auditor of the company

Any person convicted of any offence involving fraud, dishonesty or felony.

Powers and Duties of the Receiver and Manager

Before making any move towards taking control of the assets of the company, the receiver must ascertain from the

debenture holders the precise powers which he is endowed. Receivers and Managers derive their powers from the

main instrument under which they are appointed. The statutory powers are contained in schedule II of CAMA CAP

C20 LFN 2004 and these are:

Power to take possession of, collect and get in the property of the company and for that purpose

to take such proceedings as may be seem to him expedient

Power to sell or otherwise dispose of the property of the company by public auction or private

contract

15. Page 15 of 31

Power to raise or borrow money and grant security thereof over the property of the company

Power to appoint a solicitor or accountant or other professionally qualified person to assist him

in the performance of his functions

Power to bring or defend any action or other legal proceedings in the name and on behalf of the

company

Power to refer to arbitration any question affecting the company

Power to effect and maintain insurance in respect of the business and property of the company

Power to use the company’s seal

Power to do all acts to execute in the name and on behalf of the company a deed, receipt or

other document

Power to draw, accept, make and endorse any bill of exchange or promissory note in the name

and on behalf of the company

Power to appoint any agent to do any business which he is unable to do himself or which can

more conveniently be done by an agent and power to employ and dismiss employees

Power to do all such things (including the carrying on of works) as may be necessary for the

realization of the property of the company

Power to make any payment which is necessary or incidental to the performance of his

functions

Power to carry on the business of the company

Power to establish subsidiaries of the company

Power to transfer to the subsidiaries of the company the whole or any part of the business and

property of the company

Power to grant or accept a surrender of a lease or tenancy of any of the property of the

company, and to take a lease or tenancy of any property required or convenient for the business

of the company

Power to make any arrangement or compromises on behalf of the company

Power to call up any uncalled capital of the company

Power to rank and claim in the bankruptcy, insolvency, or liquidation of any person indebted to

the company and to receive dividends and to accede to trust deeds for the creditors of any such

person

Power to present or defend a petition for the winding up of a company

Power to change the situation of the company’s registered office

Power to do all things incidental to the exercise of the foregoing powers

Statement of Affairs

S 396 (1) of CAMA CAP C20 LFN 2004 requires that within fourteen days of the receipt by the company of the

notice from the receiver advising of his appointment, a statement of affairs of the company is to be prepared and

submitted to the receiver. Power is given to substitute for the fourteen days such longer period as he may allow.

Distributions of proceeds of realization

Receiver’s remuneration, costs and expenses as stated in the deed of appointment

Preferential creditors he is not under any obligation to agree the claims of the unsecured

creditors, he must agree all claims of preferential creditors in order that he may be in a position

to settle this out of his charge realization before making payments to the debenture holders

LIQUIDATION

Introduction

The provisions of CAMA CAP C20 LFN 2004 relate to the processes of the liquidation of companies just as the

provisions of Bankruptcy Act 1979 regulate the bankruptcy processes of individuals and partnership business. The

essential provisions are highlighted below:

16. Page 16 of 31

Modes of company liquidation

The modes of winding – up as stipulated by Section 410 (1) of CAMA CAP C20 LFN 2004 are:

Compulsory winding – up by the court

Members voluntary winding – up

Winding – up subject to the supervision of the court.

Compulsory winding – up:

Circumstances under which compulsory winding-up may occur are:

i.) Resolution by members of company requesting the court to liquidate the company compulsorily

ii.) Default in making statutory reports or holding of statutory meetings

iii.) Where the members of the company has been reduced below the statutory minimum of two

iv.) Where the company is insolvent

v.) Where in the opinion of the court it is just and equitable to do so.

Members’ voluntary winding-up:

The following circumstances may warrant member’s voluntary winding-up:

i.) A special resolution passed to that effect by members of the company

ii.) On expiration of term fixed by the memorandum and articles of association

iii.) Occurrence of an event predetermined in the memorandum and articles of association.

Liquidation subject to court supervision:

This is also members voluntary winding-up, the members may pass a resolution requesting the court to supervise the

liquidation process hence it is called winding-up subject to court supervision.

Petition for winding up of A Company

By section 401(1) of CAMA C20 LFN 2004 an application to the court for the winding up of a company may be

made either by:

The company

A payable, including a contingent or prospective payables of the company

A contributory

The Corporate Affairs Commission

A trustee in bankruptcy to, or a personal representative of a creditor or contributory

By all or any of those parties together or separately

Appointment of official Receiver by the court (S 419)

The official receiver who is appointed in a company court winding up shall be a deputy Chief Registrar of The

Federal High Court and his appointment is covered by S419 of CAMA CAP C20 LFN 2004. His functions are

covered by S421 of the Act and these include:

1.) To submit a preliminary report to the court

i.) As to issued, subscribed and paid up, and estimated amount of assets and liabilities and

ii.) If the company has failed, as to the cause of the failure and

iii.) Whether, in his opinion, further inquiry is desirable as to any matter relating to the

promotion, formation or failure of the company.

2.) The official receiver may if he thinks fit, make further reports stating the manner in which the company

was formed and whether in his opinion fraud has been committed by any person in its promotion or

17. Page 17 of 31

formation, or by any officer of the company in relation to the company since its formation and the reports

may include any other matter which, in his opinion, is desirable to bring to the notice of the court.

Appointment of Liquidators (S 422)

The appointment of liquidators is covered by S422 of CAMA CAP C20 LFN 2004 in a compulsory winding up by

the court that has the following powers and duties as stipulated by S 425(1) and (2)

i.) To bring or defend a court action on behalf of the company

ii.) To appoint a legal practitioner or other professionals to assist him in his functions.

iii.) To make any calls in respect of any class of share capital that has calls outstanding

iv.) To compromise the debts owed the company or accept securities for the discharge of the debts

v.) To take out, in his official name, letters of administration to any deceased contributory and to take

any other action necessary to obtain payment of any amount due from a contributory or his estate

vi.) To carry on the business of the company as may be necessary for the purpose of winding up

vii.) To sell the property of the company

viii.) To draw, accept make and endorse any bill of exchange on behalf of the company

ix.) To enter into contracts on behalf of the company and to use the company’s seal for that purpose

x.) To prove, rank, claim and receive dividends on behalf of the company in the bankruptcy of a

contributory for any sum due from the latter’s estate to the company

xi.) To raise any money required and pledge the assets of the company as securities for the sum raised

xii.) To make a compromise or arrangement with creditors of the company

xiii.) To pay creditors of the company

xiv.) To appoint an agent to perform tasks that he is unable to perform himself

COMMITTEE OF INSPECTION

Sections 433 CAMA CAP C20 LFN 2004 allows the appointment of the committee of inspection

which comprises of representative of the contributories and creditor and their function is to assist

the liquidator in carrying his assignment.

Final Accounts prepared on liquidation

The following are the final accounts prepared on liquidation:

Statement of affairs

Receiver’s receipt and payment account

Liquidator’s receipt and payment account

Deficiency accounts (which may include initial and final deficiency)

Record of proceedings at meetings

Statement of Affairs

On liquidation, a statement of affairs in a prescribed form must be submitted by the directors, secretaries or officers

of the company within 14 days of the winding up order or of the appointment of a provisional liquidator. The

statement of affairs will contain the assets and liabilities of the company.

Before a company can go into voluntary liquidation, there must be sufficient assets to pay all debts in full otherwise

the directors will suffer heavy penalties if they are found guilty.

The Assets

These shall be separated as to

1.) Those that are not specifically pledged

2.) Those that are specifically pledged from which the secured payables will be deducted.

18. Page 18 of 31

Liabilities

The liabilities must b stated in the following orders

a.) Secured payables

b.) Preferential payables

c.) Liabilities secured with a floating charge on the assets of the company

d.) Unsecured payables

e.) Shareholders

Preferential Payables

1.) All local rates and charges due from the company at the relevant date, and having become due and payable

within 12 months next before that date, and all Pay-As-You-Earn tax deductions, assessed taxes, land tax,

property or income tax assessed on or due from the company up to the annual day of assessment next

before the relevant tax date, and in case PAYE tax deductions, not exceeding deductions made in respect of

one year of assessment and, in any other case, not exceeding in the whole one year’s assessment

2.) Deductions under the National Provident Fund Act 1961 which by Pension Act 2004, all relevant pension

contributions to an employee’s retirement savings account with a recognized pension fund administrator

3.) All wages and salaries of any clerk or servant in respect of services rendered to the company

4.) All wages of any workman or labourer whether payable for time or for piece work, in respect or services

rendered to the company

5.) All accrued holiday remuneration becoming payable to any clerk, servant, workman or labourer (or in the

case of his death to any person in his rights) on the termination of his employment before or by the effect of

the winding up order or resolution

6.) All payments under the Workmen’s Compensation Act.

ILLUSTRATION ONE

Okoro Nig.ltd got into financial difficulties on 30/09/2009. The directors passed a resolution that the company be

wound up voluntarily. The trial balance of the company as at that date is presented below.

#’000 #’000

Plant& Machinery 200,600

Freehold Building 305,000

Motor Vehicle 96,300

inventory 149,280

Receivables 106,700

payables 168,800

Call in arrears/advance 2,500 6,000

Cash in hand 14,650

10% debentures 100,000

Debenture Interest (30/09/09) 5,000

Trading loss for the year 22,520

19. Page 19 of 31

Bills payable 36,000

Bank overdraft 120,800

Retained profit 62,550

Taxation (2007 56,400 2008 42,000) 98,400

Ordinary share of #1 each 200,000

3% preference share of #1 each 100,000

897,550 897,550

ADDITIONAL INFORMATION

A. The assets are estimate to produce as follows

Plant & Machinery 124,600

Freehold Building 378,900

Motor Vehicle 62,400

inventory 89,700

Call in arrears 1,280

Receivables: 48,600

Doubtful 44,400

Bad debt 13,700

The doubtful debt will produce 25k in the naira value

B. payables consist of: Local taxes {16 month 9600} payee deductions {Jan-September 2009 26800, NPF

contribution #10000, loan for settlement of staff salaries #50400} 168800

Sundry trade payables #72000

Sundry trade payables are to be settled at an interest rate of 10k per naira in the event of liquidation.

C. The 10% debenture is secured on the freeholds building while the bank overdrafts have a floating charge on the

asset

D. The cost and expenses of liquidation and legal cost #22400 and the liquidation fees #10000 plus 5% of the

amount distributed to ordinary shareholders

E. The preference shareholder are to be settle at a 8k per share before the ordinary shareholders

F. There is a contingent liability of #5600 on bill discounted to rank @ #4200

Prepare statement of affairs and deficiency account as at 30/09/09

20. Page 20 of 31

ILLUSTRATION TWO

INAKUNA Nigeria Limited got into financial difficulties and on 30/6/2015, a receiver was appointed by debenture

holders with floating charge; and a liquidator was appointed on 31st

October 2015. On the date of receiver’s

appointment, the trial balance of the company was as follows:

Trial balance

N’000 N’000

Plant and equipment 305,000

Inventory 183,750

Receivables and payables 102,500 178,750

Mortgage loan 20,000

Taxation (2013 N65,000000; 2014 N30,000,000) 95,000

10% debentures 120,000

Debenture interest accrued (30/6/2015) 6,000

Motor vehicles 94,800

Profit or loss accounts 80,000

Cash in hand 20,200

Capital reserves 11,500

5% preference shares of N1 each full paid 30,000

Ordinary shares of N1 each fully paid 250,000

Ordinary share of N 1 each 60k paid up 75,000

786,250 786,250

Additional information:

(1) payables consist of: N

Paye tax deductions (January to June 2015) 18,400,000

NPF contribution 7,600,000

Local rates (16 months to 30/6/2015) 4,800,000

Loans for settlement of staff salaries 47,450,000

Sundry trade payables 100,500,000

178,750,000

Sundry trade payables have agreed to accept a dividend of 92k in the naira value in full settlement.

(2) The mortgage loan was secured on a fixed plant with a book value of N40,000,000 but was realized by the

receiver for N31,800,000

(3) The receiver also realized the remaining plant and equipment for N228,600,000 and the motor vehicles for

N49,950,000. The expense of the receiver was N9,840,000, while the remuneration was agreed at

N6,000,000 plus 3% of the amount realized. On 31/10/2015, he made all his obligatory payments and

transferred to the liquidator the balance of cash in hand.

(4) The liquidator realized the inventories for N102,226,000 and collected only 65% of the book receivables.

His expenses and remuneration were N12,300,000 and #25,440,000 respectively.

(5) The preference shareholders were to be settled at a premium of 10 kobo per share before the ordinary

shareholders.

You are required to:

Prepare the final accounts of:

(i) The receiver 10 marks

(ii) The liquidator 10 marks

ILLUSTRATION THREE

21. Page 21 of 31

Oluwo Ltd passed a resolution at the extra ordinary general meeting on January 1st

, 2010 to close business

voluntarily. The following is the balance sheet of the coy as at that date

N 000

Fixed assets

P & M 1,280,000

inventory 620,000

Receivables 1,011,000

Cash 9,000

Profit or Loss account 415,000

3,335,000

Share capital

Ordinary share capital 1,200,000

5% preference share of cash fully paid 650,000

6% Debentures 350,000

payables 1,135,000

3,335,000

Additional information

The Plant & Machinery including inventory on 1st

january 2010 realized N1,811,000,000 and receivables other than

N42,000,000 which was considered irrecoverable were received in full.

The payables were paid in full; N34,000,000 of the total sum was regarded as preferential creditors.

The debentures were repaid with half year outstanding interest of N10,500,000, on 31st

match 2010.

Stated in the articles of association was a clause which confers on the preference shareholders the right to have their

capital and arrears at the date of commencement of winding up (but not thereafter) paid in priority to ordinary

shareholders. The arrears of such preference shares on 31/12/2009 was N81,250,000.

The liquidator’s remuneration was agreed at 21

/2% on the amount realised and 21

/2% on the dividend paid to the

shareholders. The liquidator’s expenses were N38,450,000.

Required:

I Prepare the liquidators receipts and payments account. show all workings .

II Outline five examples of preferential debts.

FOREIGN BRANCH ACCOUNT

22. Page 22 of 31

Foreign branches are those situated outside the foreign country where the head office is located. They are usually

self- accounting and transactions are denominated in the currency of the host nation.

TRANSACTION METHODS FOR FOREIGN BRANCHES

For the purpose of translating foreign branches, the methods that can be used are

Temporal method

Closing rate method

Monetary and non monetary method

1.Closing rate method

Under this method, all assets and liabilities are translated at the rate ruling at the statement of financial position date.

This method is also referred to as the current rate method.

2. Temporal method

Under this method, current assets and liabilities are translated at the rate ruling at the statement of financial position

date and noncurrent assets and liabilities are translated at the applicable historical rate at the dates they were

acquired or incurred. This method is sometimes referred to as current and noncurrent method.

3. Monetary and non monetary method

Under this method monetary and non monetary assets and liabilities are translated at the rate ruling at the statement

of financial position dates and non monetary assets and liabilities at the historical rates ruling at the dates they were

acquired or incurred. Assets and liabilities are regarded as monetary if their nominal values are fixed. All other

statement of financial position items are classified as non monetary.

EXCHANGE RATE

The exchange rate to use for each transaction under the following method is translated below.

TRANSACTIONS TEMPORAL METHOD CLOSING RATE METHOD

Inventories The actual rate ruling on the

acquired date of purchase or transfer

The closing rate, if acquired by

branch or at actual value, if

acquired by head office.

Non- current asset At actual rate ruling on the date of

purchase or transfer.

Rate ruling on the statement of

financial position date.

Current asset and current liabilities Rate ruling on the statement of

financial position date.

Rate ruling on the statement of

financial position date.

Profit or loss items Average rate of exchange for the

year.

Rate ruling on the statement of

financial position date.

Head office current account Actual rate Figure in the head office book.

23. Page 23 of 31

ILLUSTRATION 1

Malami plc opened a foreign branch in Japan on 1 January 2011, supplying necessary funds on that date. Non-

current assets costing 80,000 yen and inventory costing 36,000 yen were purchased on 1st

January 2011 leaving the

branch with a cash balance of 24,000 yen. The trial balance of the branch at 31st

December 2011 is given below. No

provision has yet been made for depreciation on the non-current assets, which have an estimated useful life of 10

years and a new residual value. The closing inventories of the branch are valued at 54,000 yen. The exchange rates

are as follows:

1 January 2011 8 yen to ₦1

31 December 10 yen to ₦1

Average for the year 9 yen to ₦1

Rate applicable to closing inventory 9.6 yen to ₦1.Malamiplc branch trial balance as at 31/12/2011.

Yen Yen

Head office current account 140,000

Non-current assets. Cost 80,000

Revenue 540,000

Purchase 450,000

Opening inventory 36,000

Expenses 81,000

Trade receivable 45,000

Trade payable 33,000

Cash 21,000

713,000 713,000

REQUIRED

Prepare the branch trading and statement of comprehensive income and statement of financial position in naira ready

for consolidation with head office results. Using temporal method.

ILLUSTRATION 2

The following information relates to kudi, a foreign subsidiary of ego plc. Statement of financial position as at

31/12/12.

Cedi

24. Page 24 of 31

Non- current assets at cost 2,250,000

Less depreciation (900,000)

1,350,000

Inventory 900,000

Receivables 450,000

2,700,000

Ordinary shares 450,000

Retained profit 1,260,000

1,710,000

Loans 495,000

Payables 247,500

Taxation 247,500

2,700,000

Statements of comprehensive income for the year ended 31st

December 2013.

Cedi

Profit before tax 720,000

Tax 360,000

360,000

Other relevant information

(a) Exchange rate value

(I) C75 to ₦1 when the company was incorporated.

(ii) C62.5 to ₦1 when this company acquired its assets

(iii) C50 to ₦1 at January 2011.

(Iv)C40 to ₦1, average rate during the year ending31/12/2013.

(V) The exchange rate at 31/12 2013 was C25.

Depreciation is at the rate of 12% P. A

(b) The opening inventory of kudi plc was C 540,000

(c) Ego plc acquired all the shares capital of kudi plc for 8,000 when the reserve of the latter was nil.

25. Page 25 of 31

You are required to show for inclusion in the consolidated accounts of the group

(i) The translated statement of financial position of kudi plc as at 31/12/12

(ii) The translated statement of comprehensive income using the closing rate method.

ILLUSTRATION THREE

Lekwot Enterprise operates in Nigeria with a branch in Ghana, Dudu Enterprise.

The financial statements prepared in Cede (Ghana Currency) were as follows:

Dudu Enterprises

Statement of Profit or Loss for the year ended 31st December, 2016

Turnover

Less cost of sales

Opening inventory

Add purchases

Closing inventory

Gross profit

Depreciation

Operating expenses

Net profit

Cedi

355,750

120,500

476,250

(206,420)

18,000

142,820

Cedi

850,000

(269,830)

580,170

(160,820)

419,350

Dudu Enterprises

Statement of Financial Position as at 31st December, 2016

Non-current assets (Net

Book Value)

Furniture and Fittings

Motor Vehicles

Cedi

562,000

120,000

Cedi

682,000

Current asset

Closing inventory 206,420

Account receivables 110,000

Cash at bank 85,000

401,420

Current liabilities

Current account 128,500

26. Page 26 of 31

Account payables 140,000

(268,500) 132,920

814,920

Financed by:

Retained profit 634,700

Long term debt 180,220

814,920

Additional information for the period was given as follows:

i. The head office current account and the tangible assets were agreed at when the

exchange rate was ₦0.20/1cedi on 01/01/2014.

ii. On 1/1/2016 the retained earnings was ₦23,500

iii. The exchange rates for cedi during the period were:

1/1/2016 ₦0.56/1cedi

31/12/2016 ₦0.73/1cedi

Required:

Translate the financial statement of Dudu Enterprises into Naira using temporal method

INFLATION ACCOUNTING

Introduction

Conventional accounts are based on historical cost that is assets are valued in the balance sheet as their cost of

acquisition. Expenses are also charged against revenues in the determination of profit based upon the historical cost

of the assets used up in generating the revenue. The system was developed long ago during decades of relatively

stable price levels and continued to be used before the consequences of inflation on the preparation of financial

accounts were recognized. Post war (11) reconstructions witnessed an ever increasing rate of price changes and

since then academic as well as practicing accountants have been paying particular attention to the need to formally

adjust for the effect of inflation in publishing accounts. Limitations of historical cost accounting

Histo rical cost accounting has five main limitations and these are:

1. Depreciation inadequate for the replacement of fixed assets:- Historical cost accounting seems to write off the

cost of fixed assets over their useful lives.it does not set out to provide a fund from which the fixed assets can be

replaced at the end of their lives. Nevertheless, in a period of stable prices, sufficient cash could be set aside over the

life of an asset to replace it at its original cost. In times of inflation, insufficient fund is provided in this way to

enable the business replaces its assets.

27. Page 27 of 31

2. Cost of sales understated:-In historical cost accounts, stock consumed and sols is charged against sales at its

original cost, rather than at the cost of replacing it. But, in order to retain the same stock level, the company has to

finance the difference (and used to do so entirely out of profits after tax until introduction of stock relief).

3. Need for increase in other working capital not recognized:-In most companies, debtors are greater than creditors,

so, on an unchanged volume of business, “debtors minus creditors “increase with inflation, requiring extra money to

be provided for working capital. Historical cost accounts fail to recognize that this extra working capital is necessary

to maintain the operating capacity of the business and that it has to be provided for the business to retain its going

concern.

4. Borrowing benefits not shown:- Borrowings are shown in monetary terms, and if nothing is repaid, and nothing

further is borrowed, borrowing appears stable. This is a distortion of the picture because a gain has been made at the

expense of the lender (since in real terms the value of the loan has declined): some schools of thought feel that this

gain ought to be reflected in the accounts.

5. Year on year figures not comparable:-in addition to being overstated due to ;

a. Inadequate provision for depreciation

b. Understated cost of sales

c. No provision for increase in other working capital,

Profits are stated in terms of money which has itself declined in value. Similarly, turnover and dividends are not

comparable with those of other years, because they are expressed in naira of different purchasing power. The

reporting of profit inflated naira gives a far too rosy impression of growth in profitability. This tends to lull both

managers and shareholders into thinking that their company is doing very much better than it really is, it encourage

unions and employees to expect wage increases that are unmatched by real (as opposed to reported) profit growth,

and it also can does encourage government measures that are very harmful to the long- term prosperity of the

company, e.g. the imposition of price controls, or excess profit tax made on a completely false impression of

profitability.

Having discussed the limitations of historical cost accounting on published financials statements, we shall now look

at the various attempts made to date to bring the effect of inflations into the annual historical financial statements.

These are:

1. Current purchasing power (CPP)

An exposure draft, ED 8-Accounting for Changes in the purchasing power of Money-was issued in 1973

(which became provisional SSAP 7 in 1974)recommending that company adopt what came to be known as

current purchasing power(CPP). The main features of ED 8 were that;

a. Companies could continue to keep their record and present their basic account in historical terms, i.e.

in terms of the value of naira at the time of each transaction or revaluation.

b. In addition, all listed companies would present to their shareholders a supplementary statement in

terms of the value of the naira at the end of a period to which the account related.

c. The conversion of the figures in the basic accounts into figure in the supplementary statement should

be by means of a general index of purchasing power of the naira(the retail price index)

d. Directors should provide in a note to the supplementary statement an explanation of the basis on which

it has been prepared, and should comment on the significance of the figures.

CPP accounting was concerned solely with removing the distorting effects of changes in the general

purchasing power of money on accounts prepared in accordance with established practice(i.e. on

28. Page 28 of 31

historical cost basis).it did not deal with changes in the relative values of non-monetary items(which

can and do occur in the absence of inflation).

CPP accounts were criticized on a number of grounds. Among these were:

a) Shareholders were faced with a choice between two sets of figures which frequently gave very

different results. Both could not be correct.

b) CPP accounting enhanced the profits of companies which were heavily borrowed, particularly

those showing low profits on an historical basis. These were assumed by CPP to be increasing in

value in line with inflation (i.e maintaining their real value), while the money borrowed to acquire

them was declining in real value. The more heavily borrowed the company, the more profits

became boosted by CPP.

Basics of CPP Accounting

With CPP accounting, the figures in the historical costs are adjusted in order to take account of

changes in the purchasing power of money during the period covered by the historical cost

accounts. Profit is recognized only when the capital has been maintained in real terms (purchasing

power of the share capital must be maintained).

The mechanics of CPP

To prepare CPP, we first start with a set of historical costs are adjusted in order to take account of

changes in the purchasing power of money during the period covered by the historical cost

accounts. Profit is recognized only when the capital has been maintained in real terms (purchasing

power of the share capital must be maintained).

Basics of CPP Accounting

With CPP accounting. The figures in the historical cost are adjusted in order to take account of

changes in the purchasing power of money during the period covered by the historical cost

accounts. Profit is recognized only when the capital has been maintained in real terms (purchasing

power of the share capital must be maintained)

Advantages of CPP

1. Simplicity- once a set of historical accounts has been prepared, it is quite simple to prepare a set of CPP.

2. Objectivity- it is objective since it is prepared on actual transactions and there is no element of subjectivity

in choosing an index since a specific index is used as Retail Price index.

3. Cheapness- it is a cheap system to implement since very few additional records need to be kept.

4. Concern with shareholders capital- CPP accounting is designed to show if shareholders capital is

maintaining its purchasing power. Only when the capital has been maintained can the company be said to

be making profit.

5. It is a system of inflation accounting- since it does not adjust the basis of valuing assets but only adjusts the

measuring units (Naira). Also it does differentiate monetary and non-monetary assets which are an

important factor in accounting for inflation

Disadvantages of CPP

1. Subjectivity- since the figure are based on historical cost, the disadvantages of historical costs are passed

over especially weaknesses in producing the historical cost accounts.

2. Unrealistic assets value- since a general index is being applied to the assets, the assets value which appears

in the accounts are unrealistic.

3. Confusing unit of measurement- the naira unit of measurement on both historical accounts may be implied

by readers as same for subsequent years.

4. Its concept of profit- the concept adopted for capital maintenance is not very useful.

29. Page 29 of 31

5. Gains/losses on monetary items- there is controversy over whether gains and losses on monetary items

should be regarded as profits or losses.

6. Use of general index- there is a general argument that the use of General index is irrelevant when

measuring the effect of inflation on companies, that the general index may be useful as to supermarkets but

not useful to a company buying heavy machineries.

CURRENT COST ACCOUNTING

Provisional SSAP 7 was issued in May 1974 on CPP accounting, however the Sandilands Reports in accounting for

inflation in September 1975 came out in favour of Current Cost Accounting (CCA) therefore the provisional SSAP 7

was withdrawn in October 1978.

Its features and Advantages

According to SSAP 16 on Current Cost Accounting, the basic objective of current cost accounting is to provide

more useful information that that available from the historical cost of accounting alone, for the guidance of

management of the business, the shareholders and others on such matters as the financial viability of the business,

returns on investment, pricing policy, cost control and distribution decisions and gearing.

The main features of SSAP 16 are as follows:

1. Current cost information should be published in addition to historical cost information as part of the annual

financial report.

2. The current cost accounts should consists of an income statement and a balance sheet with explanatory

notes.

3. The current cost income statement should show the current cost operating profit or loss. This is derived by

making three adjustments to historical cost profit before interest and taxation in respect of depreciation,

cost of sales and monetary working capital. The nature of these adjustments is discussed in detail later on in

this chapter.

4. The current cost income statement should also include a figure which is attributable to shareholders. This is

derived by making a gearing adjustment to the current cost operating profit.

5. Current cost earnings per share based on the current cost profit attributable to the shareholders should be

disclosed.

6. The current cost balance sheet should include fixed assets and inventories at their value to the business. The

balance sheet may be shown in summary form and should include a separate current cost reserve showing

the effects of three elements:

(i) Revaluation surplus or deficits arising from price changes in respect of fixed assets and

inventories.

(ii) The monetary working capital adjustment

(iii) The gearing adjustment.

Advantages of CCA

No doubt to convince the accounting fraternity further of the benefits of CCA, the IASG’S introduction

carefully spells out the advantages of this form of accounting as follows:

(a) Calculating depreciation on the basis of the value to the business of fixed assets will provide a more

realistic measure of resources used in the period.

(b) Calculating the cost of sales on the basis of the cost of replacing goods at the time they were sold will

help maintain the value of the entity in real terms.

30. Page 30 of 31

(c) The introduction of the appropriation account will bring together revaluation surplus and current cost

profit, which will help directors in their retention and dividend intention.

(d) Assets will be shown at their current value in the balance sheets.

(e) A statement of the changes in equity interest, after allowing for changes in the value of money. Will

show how the company has performed in real terms during inflationary periods.

(f) The effects of holding monetary items of gains or losses will be highlighted.

(g) Both management and users of accounts will be provided with more realistic information on such

things as the value of assets, cost, and profit, and thus on real returns on assets and capital.

(h) It clearly distinguishes between gains made from operations and gains made from holding assets.

MONETARY WORKING CAPITAL ADJUSTMENT (MWCA)

The term monetary working capital includes trade receivables, bill receivable, prepayment, trade

payables, bills payable, accruals, cash and banks balances and bank overdrafts. The method

employed is to convert opening and closing monetary working capital from a historical basis to a

current cost basis by the use of appropriate index numbers. The excess of the historical cost figure

over the current cost constitutes the MWCA. capital instead of being included in stock subject to

COSA. In arriving at the figure of monetary working capital, only item noted above which are

purely employed in the day – to – day operating activities of the business are included, e.g.

receivables and payables relating to acquisition of non current assets and disposals are excluded

from MWC also some cash and bank balances and overdrafts which are regarded as a component

of net borrowings.

Monetary working capital is an operating asset which must be maintained to allow the operating

capability of a business to remain unimpaired. The MWC represents the variations in finance

needed for monetary working capital purposes as a result

QUESTION ONE

DEBARE was formed on 1 January 2006 with a fully subscribed share capital of N200, 000. On

the same date a loan of N100, 000 was raised.

On 31st

2006, storage facilities with a twenty-year life no residual value were purchased for N 150,

000. On the same date 1,000 stock items were purchased for N100, 000. On 30th

June 2006, 600 of

the stock were sold for N90, 000. Expense of N10, 000 was paid on 30 June 2006. All transactions

were for cash.

The company provides a full year’s depreciation in the year of acquisition of an asset.

A general price index moved:

1 January 2006 660

31 January 2006 715

30 June 2006 780

31 December 858

Assuming straight line depreciation, you are required to:

(a) Prepare historical cost accounts for the year to 31 December 2006

(b) Prepare current purchasing power (CPP) accounts for the year to 31 December 2006

(c) State the advantages of CPP.

QUESTION 2

Mr. Giwa Jikolo sent his company’s latest financial statements shown below under historical cost

basis to Mr. Field Grass, a friend , residing in united states and to seek financial assistance from

31. Page 31 of 31

him. The assistance is to purchase machines and equipment to replace the old ones, presently in

use. Mr. Grass faxed back the accounts requesting that the accounts should be more realistic by

showing the present values adapted to price index, current purchasing power or current cost:

nothing that the value of money is not constant especially in Nigeria where the Naira fluctuates

widely against major rule foreign currencies. He insist that his bank requires these to grant the

loan he has applied for on behalf of jikolo and sons Ltd.

JIKOLO AND SONS LTD

PROFIT OR LOSS ACCOUNT FOR THE YEAR ENDED 31ST

DECEMBER 2005

N000 N000 N000

Sales 15000

Less: cost of sales:

Opening stock 2,650

Purchases 10,490

13,140

Closing stock 2,960 10,180

Gross profit 4,820

Less: depreciation:

Buildings 220

Plant and equipment 956 1,176

Other expenses 2,614 3,790

Net profit 1,030

JIKOLO AND SONS LTD

STATEMENT OF FINANCIAL POSITION AS AT 31ST

DECEMBER 2005

N N

Equity and Liabilities: Non current assets:

Ordinary shares 70,000 land & building 44,600

Profit/ loss 22,000 plant& Equipment 77,400

92,000 122,000

Mortgage loan 50,000

142,000

Current liabilities: current assets:

payables 13,000 inventory 29700

Taxation 8,500 Receivables 15300

Dividend 5,500 cash 2000

169,000 169000

REQUIRED:

(a) Redraft the financial statements using the current purchasing power basis. The price index at

the beginning of the year was 100 while the index at the end of the year was 120. All revenue

transactions during the year are stated at an average index of 110.

(b) Advise on the use as against historical cost of :

(a) Price index

(b) Current purchasing power.

(c) Monetary unit.

Outline the major requirements jikolo and sons Ltd. Might provide to meet the conditions for obtaining foreign

loan.