1. PART 1- Project objectives and overall research approach - (1000 words)

1.1. Reasons for choosing the project topic area and the particular

organisation that is the focus of the research work

My project topic is “An organization’s budgetary control system and its links

with performance management and decision making” and my project title is

“An evaluation of the budgetary control system of Sur Construction Plc

(Sur) and its support to the company’s performance management and

decision making processes”.

I selected this topic for the following reasons which make me feel more

comfortable with and confident to successfully complete this research

compared to the other ones.

A subject matter, concerning my company, in which I wanted to see

improvement

It is within my area of expertise

I found sufficient amount of relevant literature

My employer found the topic relevant and promised to provide all the

necessary support including access to relevant data and use of office

facilities for this purpose

It gives me the opportunity to demonstrate IT skill

Besides I have observed that in Sur this issue is not given due attention. I

believe that by conducting the research I may come out with relevant findings

that might help my company improve its budgetary practices. Similar

companies in my country (Ethiopia) may also find the work useful.

The focus organisation:

The focus organisation is “Sur Construction Plc”. I selected Sur because:

I have secured permission of access to relevant information and full support

in material, financial and moral from my employer to undertake the research

I could save time and cost of securing relevant information from other

companies and allow me devote more time on analysis of data collected

It would help me demonstrate my capability of doing research relevant to my

company and thus promote myself

1.2. Project objectives and research questions

The objectives of the research are:

To evaluate the budgetary control system of Sur for adequacy in its design

and implementation

1

2. To identify the links of the budgetary control system with performance

management and decision making processes within Sur.

To give recommendation on the system based on findings of the study.

To achieve the objectives stated I would evaluate the budgetary control system

by dividing it in to its components i.e.

Administration

Preparation

Control

Research questions

This study tries to address the following basic questions:

How good was the budget administration in Sur?

How good was the budget preparation in Sur?

How good was the budget control in Sur?

Assessment variables

The following variables which are believed to be indicators of existence of good

budgetary control system and its links with the company’s performance

management and decision making process were considered:

Does Sur have a budget committee, set a budget year, appoint a budget

officer, and conduct follow up?

Does Sur communicate policies, determine key budget factor, prepare

budgets based on key budget factor, coordinate individual budgets, use

approved master budget as a benchmark? What type of budget does Sur

prepare?

Does Sur produce performance reports, perform variance analysis, and how

frequent? Does Sur use feedback for performance evaluation and decision

making?

1.3. Overall research approach

Place of the research

An author (Oliver, 2004, p. 126) has discussed on the necessity of indicating

‘location for the research’. The research is being conducted within the

organisation in my office and for this I have already obtained the necessary

permission from the relevant authority.

Structure of the research Project

The structure followed for the Research Project is the one recommended by the

Oxford Brooks University as it is devised to enable students ‘demonstrate all of

the required technical and professional skills, and graduate skills in sufficient

depth’ (OBU Information Pack, 2008, p. 26); so I do not want to risk this

opportunity by developing another different structure which may or may not

demonstrate the stated quality.

2

3. Scope

The project is limited to Sur Construction plc, covered 2007/2008 budget

year, and only the variables identified above were used to evaluate the

budgetary control system and its contribution to company performance

management and decision making. Capital budgeting and cash budget were

not covered.

Information Gathering

Type of Data used

Only secondary data were collected for my research project and both external

and internal sources of secondary information were used to evaluate the

budgetary control system for its design and implementation and also for its links

with the company’s performance management and decision making activities.

In case secondary data is not available on certain areas of the system

discussion and even oral or written interview with appropriate officials would be

conducted.

It is also necessary to mind that reliance on secondary data is wholly

acceptable by the Oxford Brookes University, so why spend more time in

collecting and evaluating primary data.

Sources of Data

(See Part 2 section 2.1)

Method of collecting

(See Part 2 section 2.2)

Analysis:

Data analysis will be made based on whether:

• Standard costing, i.e. forecasted resource price and usage, and cost

prediction methods were used

• Key budget factor was defined

• All employees participated in preparing the budget

• Activities were coordinated

• Master budget was agreed and authorised

• The budget was used as a benchmark

• Regular performance reports and variance analysis made

• Influence in enhancing performance management and decision making

• Purposes of the system were achieved.

Finally Conclusion and Recommendation will follow based on results of the

analysis made above.

3

4. PART 2 - Information gathering and accounting/business techniques-1500

words

2.1. The sources of information from which relevant data obtained

The research mainly requires demonstration of skills of evaluating and

analysing of data collected. Besides, use of secondary data for the research is

acceptable by the Oxford Brookes University. As a result secondary data were

obtained from:

• literature reading materials i.e. books, articles and relevant resources in the

internet listed in the “references” section of this paper. These would be

sufficient enough to set criteria on which to base the evaluation

• internal information on the administration, preparation and control aspects of

the company’s budgetary control system would be sufficient enough to

understand the overall picture of the system and reach conclusion.

In case when secondary data were found to be inadequate or unavailable,

discussions were made with the cost and budget officer, the planning and

monitoring officer, with commercial and construction department heads, and the

general manager.

External Sources of information

Relevant Literature books, articles and internet resources

Internal sources of information

Company organizational Chart (See Appendix A)

Formal letters of instruction to establish budget committee, letters of

appointment issued to individual members of the budget committee and

budget officer

Company budget manual, budget policies, strategic or long-term plan, and

approved master budget for the year 2007/2008

Periodic performance reports (monthly, quarterly and annually)

Variance analysis on performance reports

Minutes of meetings made to follow up budget implementation, to evaluate

performance and to make corrective and review decisions

Documented decisions taken by management (minutes and letter of

instructions)

2.2. A description of the methods used to collect information, including online

access

In collecting information I followed the following steps:

1. Identify locations of sources of information

2. Reach locations to collect the information

3. Arrange appropriate safe custody for information collected

4

5. 4. Return on completion of the research those sources of information back to

their location.

Location for external sources of information

Most of the Literature Books were collected from the British Council Library.

Books from friends and my own texts were also used for the research. The

ACCA Student Accountant was also an important source of published articles

on subjects that provide guidance on how to pass the RAP and on subjects

related to budgetary control and variance analysis techniques.

The internet particularly the www.accaglobal.com and www.google.com websites

were also very helpful locations for sources of relevant information. I have

downloaded The RAP information PACK , an important document that guides

how to approach the research, from the www.accaglobal.com and other internet

resources related to research methods were collected from the www.google.com

Location for internal sources of information

The following were among the most important internal sources of information

for the study:

The commercial department is responsible for getting business for the

company and facilitates the planning and monitoring processes within the

company. Standard prices and usage of resources and total revenue for the

year were determined by this department.

The planning and monitoring division which is under the direct

supervision of the Construction Department, maintained records related to

planning and control information on project contracts, was another major

source of information in relation to project plans and periodic performance

reports.

The cost and budget division which is under the direct supervision of the

Finance Department Manager produced financial reports in relation to cost

of construction of each project contracts. The annual action plan for

2007/2008 was obtained from the finance department manager.

The Human resources department is also an important location of

information sources such as the appointments of the budget committee and

the budget officer. Also sources of information in relation to performance

related pay is located in this department.

Reach locations to collect information

As I am a member of the British Council Library I borrow books for my

research. I have access to broadband internet service in my office.

In order to reach the locations of internally produced information I have formally

obtained permission from the general manager to have access to relevant

5

6. information of the company. I personally discussed with the personnel in charge

of the locations I have identified above and therefore collected information I

needed for my project.

Arrangements were made to meet these individuals to discuss how and when

they could supply me the information I needed. I gave them a note of list of data

that I needed.

Arrange appropriate safe custody for information collected

I arranged a shelf with a locker and safely stored notes of discussions made

with different officials of the company and copies and original documents

obtained many of which I had to return to the providers after completion of the

research. The discussion notes and other documents collected were classified

by nature and location and filed in a box file.

Return of secondary information back to their location on completion of

the research

After completion of the study, I returned all documents and books collected

from the company, the British Council and other sources as promised. I kept

some copies of the aforementioned sources which are not restricted by

copyright for further references.

2.3. A discussion of the limitations of the information gathering

Listed below are some of the major limitations I observed and faced in

connection with the information gathering process i.e. use of secondary data as

source of information:

Accuracy of information collected from the company itself cannot be

guaranteed as they are originally gathered by other people.

Finance and construction departments produced separate profit and lose

statements for 9 months and their reports have differences.

There were two different copies of budget manuals. None of the two

manuals were stamped as final. After a discussion with the finance

department manager this problem was solved.

Differences in figures were also observed on planned project revenues

reported in the three year business plan compared with the annual action

plan.

Annual financial reports were not finalised.

Information gathering from the internet was easy but difficult to determine

the most relevant resource out of bulk of resources. Sometimes it was of

time taking activity compared to its benefit.

Information collecting encountered me with different officials within the

company. Not all were comfortable with providing data to me as many of the

data were prepared by themselves.

Another problem was that there was no formally documented students’

previous work on RAP which could have helped in assessing the overall

effort required and could have helped raise confidence.

6

7. Also there was problem with some staff members in keeping the appointment

date to provide me necessary document. For example, the planning and division

officer was out of office for training.

2.4. Identification of any ethical issues that arose during information

gathering and how they were resolved

The ethical issues involved with my research project were mainly in relation to

integrity and confidentiality of information of the company.

Ethical issues related to integrity

Conducting the research on Sur Construction plc

Using company facilities such as personal computer, stationeries and my

office

Ethical issues related to confidentiality

Disclosing information of Sur in my Research Project which can be accessed

by my examiners at Oxford Brookes University.

Presenting my research to my mentor, an outsider.

Keeping confidentiality of information

These were the ethical issues I tried to properly deal with. I obtained proper

permission from my employer in dealing with disclosure of information with in

my research project and uses of my employer’s resources.

2.5. An explanation of the accounting and / or business techniques you have

used, including a discussion of their limitations.

The accounting techniques and models the company will apply are:

Standard costing: used to set standard costs and usage of resource to

enable prepare plan and evaluate performance against these standards.

Their limitation is that they are subject to changes caused by external and

internal factors.

Responsibility Accounting: help assign tasks to a manager and make the

manager accountable for the task. It is however difficult to accurately

separate one activity of a manager from the other particularly in relation to

overhead costs.

Percentage Completion Method: it is a method of calculating revenue for the

year based on actual costs incurred in relation to contract revenue. But it

has failures in accurately calculating revenue earned for the period because

actual costs incurred may not be equal to plan.

Flexible budget and Variance analysis: help identify causes of deviations

and make accountability easier. Involve complex calculations and may be

are very costly to operate.

7

8. I expect the company uses these techniques in preparing budget and evaluating

actual performances. My job in this case is to investigate whether these

techniques were adequately applied to support the preparation of budget and its

evaluation against actual results. In doing so I use analytical procedures,

comparison and examination methods.

8

9. PART 3 - Results, analysis conclusions and recommendations-4000 words

Background of Sur Construction plc

Sur Construction is a private limited company established in January 1992 G.C.

and engaged in construction industry. The company’s current business involves

road, building and airfield construction. Sur is one of the biggest construction

companies in Ethiopia.

Sur is owned by EFFORT (Endowment Fund for the Rehabilitation of Tigray) a

rehabilitation local institution. At present, the company’s annual turnover is

approximately US$ 35million. It owned nearly US$ 30 million worth of medium

and large size civil construction and earth moving equipment.

Currently the company has 1600 permanent employees and about 6700

workers hired on daily basis. Currently it ran 15 projects, and 3 projects located

within Addis Ababa, the location of the company’s head office. 12 of the

projects are located in different parts of the country out of Addis Ababa.

On 26 March 2008, Sur Construction plc was awarded ISO: 1900:2000 by

Deutsche Gesellschaft fur Technische Zusammenarbeit (GTZ) GmBH, which

certifies quality system to conduct Road, Building, Airfield, Hydro Power,

Irrigation and Water Supply.

In 2007/2008 the company was running 15 different projects comprising of 9

road projects, 5 building projects and an airfield project.

Company mission

To perform its construction activities efficiently and effectively

To understand customers’ need and ensure their satisfaction

To ensure profitability for the owners

3.1. A description of the results you have obtained and any limitations

Information has been gathered in relation to the assessment variables identified

in PART I and the findings are presented in the following sections.

Administration of the budgeting process

The budget period of Sur Construction plc is 1st

July to 30th

of June. The

company has developed a budget manual through consultants known as

Tradesmen Engineering (pvt) LTD, an international company.

9

10. With in the manual a number of policies and procedures concerning

administration and preparation of a budget are adopted. This manual also

indicated the necessity of forming a budget committee, a budget controller and

developing and reviewing a budget manual to help proper execution of

budgetary control within the company. However no budget committee as well

as budget controller were formed so far by the company.

Annual Action Plan Preparation

The company did not prepare a budget in 2007/2008 budget year. It rather

prepared company wide annual action plan which included detailed activities

that should be undertaken by each department without expressing the

resources requirement for departments other than the construction department

and the plan was not expressed in terms of money. The preparation process

should have been made following manner as the budget manual has indicated:

10

1. Communication of planning policy

2. Key budget factor

3. Planned sales budget

4. Construction Plan

5. Preparation of individual annual plan

6. Review of individual annual plan

7. Acceptance of the agreed annual plan

8. Submitting the action plan to EFFORT for

final approval

11. 1. Communication of planning guidelines

The commercial department of the company conducted industry analysis and

gathered and recorded information on the market demand for construction,

level of competition, costs of materials, etc which was important for determining

contract cost when tendering for new incoming project contracts and for setting

target revenue and costs for existing projects.

The department organised the preparation of the company annual action plan.

In doing so the department had communicated to all responsible centres:

- the company three year business plan,

- cost targets for each construction activity of both building and road

contract projects. (See Appendix B)

2. Determining the principal budget factor (Key constraint)

Traditionally Sur started its action plan from forecasting the level of revenue to

be generated in the budget period. Therefore sales revenue was considered as

key budget factor. No limiting factor analysis was undertaken.

3. Planned Revenue Target

In its three year business plan the company determined the level of revenue to

be generated for the year 2007/2008. The plan considered:

the information gathered in relation to the industry,

the volume of work at hand,

time of completion of existing project contracts and

expectations of new contracts

completion period of projects

Accordingly the revenue for the year 2007/2008 was forecasted to be

Br.650million which is Br.50million less than the forecast made in the three year

business plan. The decrease in planned revenue was because one project

contract was excluded from the annual plan.

An extract from the business Plan

11

12. Table 1:

Three Years Company Goals on Yearly Basis (Amounts are In Ethiopian Birr)

Figures are in millions (Birr 000,000)

Serial

No. DESCRIPTION

BUDGET YEAR

TOTAL2007/08 2008/09 2009/10

1

PLANNED SALES FOR

EXISTING CONTRACTS 629.63 338.39 0.48 968.51

2

PLANNED SALES FOR

NEW CONTRACTS 70.37 461.61 999.52 1,531.49

TOTAL PLANNED SALES 700.00 800.00 1,000.00 2,500.00

YEARLY SALES GROWTH (%) - 14.29 25.00

3

PLANNED COST FOR

EXISTING CONTRACTS 614.47 318.55 0.44 933.46

4

PLANNED COST FOR

NEW CONTRACTS 63.33 415.45 899.56 1,378.34

TOTAL PLANNED COSTS 677.80 734.00 900.00 2,311.80

5

PLANNED PROFIT FOR

EXISTING CONTRACTS 15.16 19.84 .05 35.05

6

PLANNED PROFIT FOR

NEW CONTRACTS 7.04 46.16 99.95 153.15

TOTAL PLANNED PROFIT 22.20 66.00 100.00 188.20

PROFIT MARGIN (%) 3.17 8.25 10.00 7.53

7

FORECASTED NEW

CONTRACT ENTRIES 500.00 800.00 800.00 2,100.00

Amounts are in Ethiopian Birr

4. Construction Plan

The construction department ran 15 project contracts (9 road, 5 building and

one airfield projects) which were considered as a sub-responsibility centres

and each were accountable to the construction department manager.

Managers of the project contracts had produced and submitted their own action

plan to the construction department manager to be integrated into the

department’s plan.

Therefore construction department prepared the annual action plan that

showed detailed activities to be conducted and the physical resources required

to generate the forecasted revenue based on the revenue and cost targets

determined by the commercial department.

The department had listed all sorts of resources (Machineries of different types

and capacities, materials and manpower) required to execute the construction

12

13. work but not planned as to the timing of delivery and not expressed in terms of

money (See Appendix C).

Following is a brief explanation of how the remaining major departments

prepared their annual plan.

5. Prepare initial annual action plan

In preparing the annual action plan all managers including lower level

managers participated in the planning process, the process followed was

bottom-up approach. The company applied responsibility accounting to

evaluate each department and service manager’s performance.

Each department and service within the company was considered as a

responsibility centre. Therefore each department and service was responsible

for the preparation of their own annual action plan and submitted their annual

plan to the commercial department. The commercial department combining the

individual annual plans together presented to the general manager for review in

the management meeting.

Equipment Management Department

This department established targets such as available hours of machineries,

serviceability of machineries, hourly maintenance cost of machineries,

maximum number of accidents for machineries, and labour costs of involved.

But the plan did not indicate the total number of machineries in different

capacities needed for the year including the resources required in terms of

manpower, spare parts, fuel, etc to operate and maintain the Machineries.

Logistics Department

The action plan of this department focused on setting the purchase and

distribution cycle of local and foreign procurement of materials and services.

That is the days that will be taken to purchase the materials or services

requested and distribute them to user departments. However, program of

purchases and distribution was not made at all. (See Appendix D)

Finance Department

This department had indicated in its annual action plan that Ethiopian Birr 182

million cash deficit for the year 2007/2008 and identified possible sources of

finance. Out of which EFFORT (the owners) were expected to raise Birr

100million and sister companies (other companies owned by EFFORT) were

expected to raise Birr 47.5 million in the form of credit supply and services. Birr

32 million was expected to be obtained from external credit suppliers. The plan

however didn’t show in detail how it arrived at such cash deficit. The plan also

detailed the ongoing accounting activities to be done in the year without

preparing financial statements (See Appendix E)

13

14. Table 2.

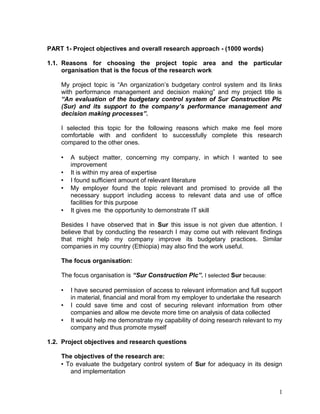

Working Capital Financing for 2007/2008 (Millions of Birr)

No. Type of finance Sources Amount

1 Capital injection EFFORT 100.00

2 Cement Credit Facility Messebo* 30.00

3 Iron-Bar Credit Facility Guna Trading* 15.00

4 Tyre Credit Facility Pirelli-Trans* 1.50

5 Transport credit TEPLCO* 1.00

6 machinery rent credit External Supplier

10.00

7 Other credit supplies External Supplier 10.00

8

Advance lease

purchase agreement

External Supplier

12.00

Total 179.50

Note: * Other Companies owned by EFFORT

The above table presented in a pie chart below:

Source of Working Capital Financing for the year

2007/2008 Amount in Birr (000,000)

147.50

32.00

1 Internal 2 External

Human Resource Department

This department had set targets for manpower recruitment and turnover.

Recruitment duration in days was determined for different levels of positions

and the minimum rate of labour turnover was set.

14

15. 6. Annual action plan submission, acceptance and approval (steps 5 to 8)

Finally after all departments and services delivered their annual plan, an agreed

and approved company annual action plan was produced and it was sent on

20th

of June 2007 to the management of EFFORT, the owner of Sur. EFFORT

approved the plan as final action plan for the year on August 2007.

Control

Performance reports were produced monthly, quarterly, semi-annually and

annually by all responsibility centres.

Construction works were the core tasks of the company. Project managers

were responsible to conduct daily monitoring in all aspects of their project

activities, and reported to each respective department at head office.

Projects’ construction work execution related performance reports were directly

submitted to the planning and monitoring division. Cost and accounting related

reports from projects were submitted to cost and budget division.

The divisions produced separate reports of profit and lose statement of all 15

projects and presented the combined reports to their respective department

managers. The reports produced by cost and budget division did not show

comparison of budget with actual results. It only reported what is actually

incurred cost against revenue calculated based on percentage completion

method.

The planning and monitoring division however produced comparison of actual

against planned works though it did not include detailed variance analysis to

identify causes of variances to support management decision making.

Comparison was made between plan and actual results, and arrived at

variance. The variance stated in both absolute and relative terms did not

consider changes in volume, price and usage. Therefore it was so difficult to

make managers accountable for failures in achieving plans as the reports were

not detailed enough in identifying causes and responsible managers to specific

variances. (See Appendix F)

Budget Review and corrective action

Actions are taken on an ad hoc basis not based on proper variance analysis

conducted by the company’s staffs. Also managers are not made accountable

for their actions taken.

3.2. A critical analysis / evaluation of your results which includes an

explanation of your significant findings

Budgetary Control

Budgetary control is concerned with ensuring that actual financial results

are in line with targets. An important part of this feedback process is

investigating variations between actual results and budgeted results and

taking appropriate corrective action (Collier, 2003, p. 225).

15

16. A budget is a plan expressed in monetary terms covering a future time

period (typically a year broken down into months). (Collier, 2003, p. 207)

From this definition of a budget it can be concluded Sur didn’t prepare budget

for the year 2007/2008. But prepared a plan of physical activities to be

performed with in the year and divided into monthly action plans.

Budget Administration

‘It is important that suitable administration procedures be introduced to ensure

that the budget process works effectively’ (Drury, 2004, p. 596)

The Company budget manual has clearly stated the necessity of establishing

budget committee and budget controller (officer). It defined the roles and types

of officials that should be members of the committee and the budget officer.

However both the budget committee and budget controller were not appointed

to administer the budgeting process, as a result:

No body within the company considered responsibility to enforce the

preparation and implementation of a budget

Adequate planning couldn’t be enforced and a budget expressed in

monetary terms could have been prepared in the year.

Coordination and communication of activities of departments within the

company could have been achieved

The company failed to set benchmark against which to evaluate actual

performance

Budget Preparation

It was made clear above that Sur did not prepare a budget for the year

2007/2008. However, it was necessary to evaluate the existing budgetary

control system of the company based on literature.

Sur had prepared an annual action plan for the year 2007/2008 and analysis is

made on the information gathered to reach conclusion and give

recommendation.

♦ Policy Communication

The long-term plan is the starting point for the preparation of the

annual budget. Managers responsible for preparing the budget must

be aware of the way it is affected by the long-term plan so that it

becomes part of the process of meeting the organisation’s objectives.

(BPP Professional Education, 2006, p. 168)

Three year business plan and standard cost, an estimated unit cost built up of

standards for each cost element and usage of resources were communicated

to construction department and other departments to be used as a basis for the

preparation of their annual plan.

16

17. ♦ Key budget factor and sales forecast

‘In every organization there is some factor that restricts performance for a given

period’ (Drury, 2004, p. 597)

This factor is known as limiting factor or key budget factor. Sur had not

conducted constraint resources analysis to identify the limiting factor before it

started preparing its annual plan. It determined sales to be the limiting factor as

a matter of traditional practice. However, during the budget year Sur faced

serious cash shortage and could not buy essential asphalt machineries and

construction materials as needed. This caused to the company both financial

and reputation damage.

Had proper limiting factor analysis been conducted and the limiting factor

identified and the annual plan was based on the identified factor Sur would

have been able to revise its forecasted revenue to a more realistic forecast

reducing its commitments to the maximum level of cash resources Sur could

have generated and also would spend the limited cash resource on activities

that give highest contribution per unit of limited resource.

As a result the forecasted revenue of Birr 650 million for the year was much

exaggerated compared to the actual revenue achieved Birr 425 million, which is

only 65%, as reported by the construction department in the annual report (See

Appendix G).

♦ Construction plan

When the sales budget has been completed, the next stage is to prepare

the production budget. This budget is expressed in quantities only and is

the responsibility of the production manager. The objective is to ensure that

production is sufficient to meet sales demand and that economic stock

levels are maintained. (Drury, 2004, p. 604)

Normally units of construction works are measured by types of activities such

as excavation and earth work, concrete ancillaries, masonry work etc relevant to

building construction and clearing and grubbing, drainage, demolishing, removal

etc relevant for road (see Appendix H) involved in each construction types-

road, building and airfield.

The construction department failed to prepare plan of total units of construction

activities for 2007/2008. This hindered reasonably accurate determination of

materials, machineries and labour usage for the year.

However, the department had determined the total quantities of usage of

materials, machineries and labour needed for the year without indicating how it

arrived at such quantities of resources requirements. Also it did not indicate the

level of ending inventories required during the year for each type of resources.

17

18. ♦ Direct Materials Purchase Plan

‘The raw materials budget is necessary to ensure adequate materials are

available to meet the production needs on a timely basis’ (Berry, 2006, p. 226)

The logistics department did not prepare material purchase plan. The possible

reason could be as the logistics manager explained the material requirements

prepared by the construction department were not time scheduled and their

accuracy was not reliable because there was no proper plan of the unit volume

of construction works.

It was also difficult to prepare direct labour and overhead budgets because

unit volume of construction work was not determined. However, selling and

administrative costs were planned based on past performance.

As a result the total material usage forecasted by the construction department

remained unchanged into monetary requirements. Therefore sufficiently

detailed and integrated company annual plan (master budget) could not be

produced in the 2007/2008 budget year and financial performance indicators

such as ROCE percentage, profit margin, and liquidity ratios could not be

determined to evaluate the company’s financial performance.

Control

At this point the budgetary control system would be evaluated for its links with

the company’s performance management and decision making.

Existence of appropriate budgetary control system would have helped to

provide benchmarks to be achieved in terms of financial and physical objectives

with in the budget period; and helped financial objectives to be expressed in

absolute terms as well as in relative terms. Amount of sales volume and profit

level could have been determined and then a budget prepared. Relative

measures such as financial ratios could have been set for that year to measure

managements’ performance.

Budgetary control could have been helped to set measures in terms of physical

targets such as kilometers of roads, materials and labour usages. Based on

such measures the budgetary control system, supported by adequate cost

accounting records, would have provided benchmark against which managers’

performances would be measured. In that the system would have served as

part of the performance management system.

By giving feedback on deviations it would have supported management to

focus on problem areas (management by exception) rather than try to control

all aspects of operations that went smooth. The feedback from a budgetary

control system would have contributed a lot to management decision making

either by enabling them to enhance or correct future performances.

18

19. The two separate main performance reports used for control were one

produced by construction department and the other by finance department.

Periodic revenue and cost performance reports produced by construction

department were made based on engineers’ estimated executed construction

works. The same report produced by finance department was based on

percentage completion method. These reports for the same period had material

differences in amounts. The construction department relied on its own records

in producing information on revenue and cost, and produced its own profit and

loss statement for each project contracts and never used the cost accounting

records of finance department believing that it did not produce accurate

information.

Flexible budget enable us make a more valid comparison between the

budget (using the flexed figures) and the actual results. Key differences,

or variances, between budgeted and actual results for each aspect of the

business’s activities can then be calculated (Atrill and McLaney, 2007, p.

213).

However the comparisons of plan versus actual performance made by the

construction department did not assume changes in volume and price.

Therefore flexible budgeting was not applied by the company in comparing

actual results with plan. Also variance analysis was not used at all. Therefore

no valid comparison of actual against planned performance could be made and

the planning process of the company failed to support performance

management and decision making of the company.

The company’s finance department produced reports only on actual revenue

and costs because there was no budget prepared for comparison.

3.3. Your conclusions about your research findings and how well you have

met your project objectives and research questions

Strength

The company developed a budget manual, which contains detailed policies and

procedures on budget administration, preparation and implementation.

The company also obtained experience in developing a three year business

plan for the budget years 2007/2008, 2008/2009 and 2009/2010. Standard

costs and usage of resources were also established for the year 2007/2008 and

communicated to all departments and services. Though the business plan and

the standards set failed to serve their purpose in helping the planning and

control process.

Weakness

The budget manual was not implemented at all. And the annual plan was full of

assumptions that never based on the company’s reality in terms of available

resources in the short term; as it did not perform scarce resource (limiting

19

20. factor) analysis to identify the company’s reality in terms of the limiting factor

and make best use of scarce resources.

Also unit volume of construction work for the year was not determined by the

construction department. Even the haphazard forecast of total resources

requirement included in the annul plan of the construction department was not

planned as to their timing when they should be made available to the

department causing other departments not to properly plan their support

activities to the construction department. For example, the logistics department

could not determine materials purchase plan (budget) and the finance

department could not determine the level of financial resources to be made

available at the right time and in the level of amount required.

The planning and control process was weak in that adequate benchmark could

not be put in place. The support that would have been provided by the

budgetary control system in enhancing the company’s performance

management system and decision making process failed to be achieved.

Effect

The company failed to enforce adequate preparation and implementation of a

budget by not giving due management attention to the issue and by not

appointing budget committee and budget accountant who could have facilitated

this. Therefore the company could not produce a budget in the year 2007/2008.

This in turn resulted in disintegration of the activities of the departments

causing each department to mind only its own activities rather than coordinating

to achieve common company goals. Also causes disputes among departments.

For example, there were instances in which it was difficult to identify

responsible manager for a delay in supply. Such an environment also created

lack of motivation in many of the managers in the company.

Lack of scarce resource analysis also caused the company to forecast an

exaggerated volume of sales compared to its available financial resource and

skilled and capable manpower (e.g. poor planning). This was another source of

less management motivation as the revenue target was unachievable.

Not exercising proper monitoring and control activities also caused

management not to access proper feedback on performance resulting weak

decision making and poor performance management. This was substantiated

by the poor cost-revenue relationship.

Conclusion

In conclusion the company’s budgetary control system was weak in its design

and implementation and failed to achieve the very purposes of the system such

as compel planning, facilitate communication and coordination and managers’

motivation.

20

21. As a result the system as part of Sur’s performance management failed to

enhance managers’ performances and decision making.

The information gathered and analysed were sufficient enough to answer my

research questions on the selected three main criteria i.e. administration,

preparation and control. The conclusion reached also was based on the

findings observed therefore I believe my research objectives were reasonably

answered.

3.4. If appropriate, recommendations on specific courses of action to

identified individuals within your chosen organisation.

Recommendations

To the company’s General Manager

Budget Administration

Appropriate management attitude and attention would help design and

implement adequate budgetary control system in the company.

Preparation

The general manager has to make sure timely preparation of budgets, as

chairman of the budget committee.

Control

Enhancement in the budget administration and preparation would improve

control. Attention has to be given to improve the cost accounting records.

The improvement in the budgetary control system is to aid the general

manger’s ability to manage performance and make informed decision.

Therefore it is necessary for the general manager to emphasize in adopting

adequate budgetary control system.

21

22. References

Atrill, P. and McLaney, E. (2007) Management Accounting for Decision

Making. Madrid: FT Prentice Hall –Financial Times.

Berry, Leonardo Eugene. (2006) Management Accounting DeMYSTiFied.

USA: McGraw-Hill Companies.

BPP Professional Education. (2006) Financial Management and Control-2.4.

Great Britain: BPP professional Education.

Collier, M. Paul. (2003) Accounting for Managers. Great Britain: John Wiley &

Sons Ltd.

Drury, C. (2004) Management and Cost Accounting. China: Thomson

Learning.

Oliver, P. (2004) Writing your thesis. Great Britain : SAGE Publications.

Bibliography

Charles T. Horngren, Srikant M. Datar and George Foster. (2003) Cost

Accounting a Managerial Emphasis. New Jersey: Pearson Education

International

Charles T. Horngren, Gary L. Sundem and William O. Stratton. (2002)

Introduction to management Accounting. New Jersey: Pearson Education Inc.

Eddie McLaney and Peter Atrill. (2005) Accounting an Introduction. Madrid:

Pearson Education Limited.

FTC Kaplan Limited. (2007) Advanced Performance Management (APM):

Paper P5. Great Britain: KAPLAN Publishing.

Graham Holt. (2003) ‘Research and Analysis: a formula for success’, Student

Accountant, October, pp. 24-26.

Shane Johnson. (2005) ‘Beyond Budgeting’, Student Accountant, March, pp.

68-71.

Shane Johnson. (2005) ‘how not to rap’, Student Accountant, June/July,

pp.26-28.

Swetnam, Derek. (2004) Writing your Dissertation. Trowbridge, Wiltshire:

How To Books Ltd.

Internet Sources Used

Chapter objectives

www.accaglobal.com

www.socialresearchmethods.net/kb/

22