Dividend Distribution Tax in India has been abolished by the Finance Act 2020 and what does it mean for the US investors / parent co is captured in a single slide.

1. Taxability of Repatriation of funds from India

India Budget for Fiscal Year 2020-21 proposes to eliminate Section 115-O, ie Dividend Distribution Tax (“DDT”)

payable by Indian Company on the distribution of its income by way of dividends. Dividend income shall now be

taxed classically in the hands of the recipient/ shareholder from April 2020 onwards.

Mechanics

• Dividend income will now be taxed at tax treaty beneficial rates for non-residents (~15% in case of US Parent

co); and

• Recipient (US Parent co) can claim the credit in resident country (ie USA) for the taxes paid in India on such

dividends

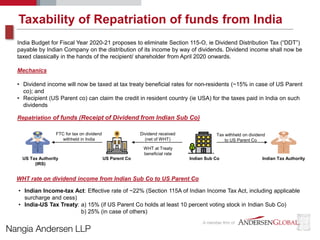

Repatriation of funds (Receipt of Dividend from Indian Sub Co)

Indian Sub CoUS Parent Co Indian Tax AuthorityUS Tax Authority

(IRS)

Dividend received

(net of WHT)

Tax withheld on dividend

to US Parent Co

WHT at Treaty

beneficial rate

FTC for tax on dividend

withheld in India

WHT rate on dividend income from Indian Sub Co to US Parent Co

• Indian Income-tax Act: Effective rate of ~22% (Section 115A of Indian Income Tax Act, including applicable

surcharge and cess)

• India-US Tax Treaty: a) 15% (if US Parent Co holds at least 10 percent voting stock in Indian Sub Co)

b) 25% (in case of others)

2. Points to Ponder

1. What would be the tax treatment of dividends in the US for the dividends received from Indian Sub Co,

assuming that the Indian Sub Co is substantially owned (> 90 percent) by the US Co?

2. What would be the mechanism of claiming Foreign tax credit (FTC) for the withholding done by Indian Sub Co

on payments of dividends to US Co?

3. Would the tax treatment/ mechanism be different if the US shareholder is an individual or a PE investor and not

a corporation?

4. How should the Federal Agency (Internal Revenue Service) be looking at this move of the Indian Government

of shifting the tax incidence on dividends to the shareholders?

5. In case there is an excess withholding done by the Indian Sub Co as per the tax treaty provisions vis-à-vis tax

applicable to the US shareholder as per US domestic tax laws, would such excess tax be available as a refund

to the US shareholder in the home country (ie the US) or would that be a sunk cost?

6. Broadly, what would be the local tax filing/ reporting compliances for the US shareholders (corporations,

individuals or PE) in case of such dividend repatriation from India?