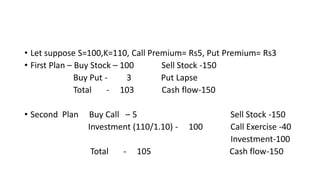

1. • Let suppose S=100,K=110, Call Premium= Rs5, Put Premium= Rs3

• First Plan – Buy Stock – 100 Sell Stock -150

Buy Put - 3 Put Lapse

Total - 103 Cash flow-150

• Second Plan Buy Call – 5 Sell Stock -150

Investment (110/1.10) - 100 Call Exercise -40

Investment-100

Total - 105 Cash flow-150

2. • let us now consider a question involving the put-call parity. Suppose a

European call option on a barrel of crude oil with a strike price of $50

and a maturity of one-month, trades for $5. What is the price of the

put premium with identical strike price and time until expiration, if

the one-month risk-free rate is 2% and the spot price of the

underlying asset is $52?

• Solution: