Railcar Manufacturer's Ability to Remain Profitable

1. December 28, 2016

Investment Thesis

While market sentiment towards the railroad industry, and in turn, the railcar manufactur-

ing industry, has turned exceptionally bearish, we believe Greenbrier’s ability to remain

financially healthy during a soft market environment and its efforts to diversify its product

base and geographical revenue stream enable it to emerge from the industry-wide rout

successful and profitable. We see value in GBX stock for these reasons, despite over-

whelming market fear of low crude oil prices decreasing the volume of oil shipments by

rail.

Thesis Highlights

Strong Fundamentals in a Tough Environment

Depressed oil prices have contributed to a steep, industry-wide earnings decline. Green-

brier’s revenue has fallen from 2015 highs which aligned with the peak of US oil produc-

tion. Despite industry woes, GBX has maintained a very strong balance sheet with a net

debt-to-EBITDA ratio of 0.18, approximately $570 million of cash, and a stable credit re-

volver. It has an industry leading ROIC of 22.95%; management is targeting 25.0% for

the second half of FY2016 (note: management compensation is tied to ROIC).

Diversifying Product Base and Revenue Stream

Greenbrier has established a strong backlog that allows it to operate efficiently through

“softer” markets—the backlog sits at 27,500 units ($3.2 billion), 80% of which is non-

energy related. The growing repairs and leasing businesses stabilize cash flows in times of

slower manufacturing. Last quarter, revenue from Leasing & Services totaled $76.6M, up

116% YoY and accounted for 12.2% of total revenue. Joint ventures and strategic acqui-

sitions have expanded operations into new foreign markets such as Saudi Arabia, Brazil,

and Eastern Europe. The international segment currently brings in 14% of revenues but

management is looking to increase this figure to 20% in the near future.

Industry Concerns may be Unjustified and/or Overstated

We believe the markets are currently overreacting to the lower price of oil and the uncer-

tainty around its future. The decline of oil prices has negatively altered the perception of

US oil production, and therefore one of GBX’s main sources of income. While prices have

declined nearly 50% in the last two years, US domestic oil production has only dropped

about 10% from its peak in early 2015 and has stabilized over the last 4 months at

around 8.5 million barrels a day.

Thesis Risks

Product Base Still Dependent on Oil and Not Yet Fully Diversified

Approximately 80% of Greenbrier’s revenue comes from its manufacturing segment, and

40% of segment revenue comes from tankers, which are primarily used for transporting

oil. Over 90% of its revenue comes from within the US. While GBX is working towards

diversifying its revenue stream on both fronts, short-term profits are exposed to an eco-

nomic shock that would affect US manufacturing or US domestic production of oil. While

President-Elect Donald Trump will likely be a tailwind for US manufacturing, the price and

output of oil is still subject to the negotiations of international bureaucrats.

Must Rise above Struggling Industry

The long-term outlook of the rail industry is underwhelming. Greenbrier must outperform

and out-diversify the industry to demand a higher valuation. Greenbrier has distanced

itself from coal transportation, the segment most likely to struggle in the long term, but it

could still suffer alongside other rail companies if pipelines become more prevalent in the

transportation of oil, as pipelines are shown to be safer despite being considered political-

ly toxic.

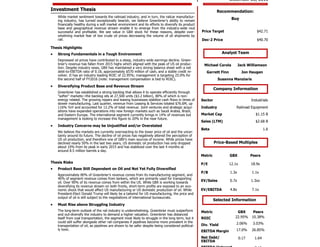

Analyst Team

Company Information

Price-Based Multiples

Price Target $42.71

Dec-2 Price $40.70

Michael Carola Jack Williamson

Garrett Finn Jon Haugen

Susanna Manziaris

Sector Industrials

Industry Railroad Equipment

Market Cap $1.15 B

Sales (LTM) $2.68 B

Beta 1.6

Recommendation:

Buy

Selected Information

Metric GBX Peers

P/E 12.1x 18.9x

P/B 1.3x 1.1x

EV/Sales 0.7x 1.3xx

EV/EBITDA 4.8x 7.1x

Metric GBX Peers

ROIC 22.95% 10.38%

Div. Yield 2.06% 3.03%

EBITDA Margin 17.0% 26.85%

Net Debt/

EBITDA

0.17 1.64

2. December 28, 2016

Business Overview1

Railcar and Marine Vessel Manufacturing

Intermodal Railcars, the most important being the double-stock railcar, which are de-

signed to transport containers stacked two-high on a single platform.

A variety of tank cars, including both general and certain pressurized tank cars, which are

designed for the transportation of products such as crude oil, ethanol, liquefied petroleum

gas, caustic soda, urea ammonium nitrate, vegetable oils, bio-diesel and various other

products.

Full line of railcar equipment designed for the transportation of automotive products.

Conventional railcars, such as boxcars, which are used in the transport of forest products,

perishables, general merchandise and commodities. Covered hopper cars, which are used

for the grain, fertilizer, sand, cement and petrochemical industries as well as gondolas for

the steel, metals and aggregate markets. Flat car products include center partition cars

for the forest products industry, bulkhead flat cars and solid waste service flat cars.

Marine Vessels—Greenbrier manufactures a broad range of Jones Act1

ocean-going and

river barges for transporting merchandise between ports within the U.S. including conven-

tional deck barges, double-hull tank barges, railcar/deck barges, barges for aggregates

and other heavy industrial products and dump barges.

Ten (10) Wheels and Parts shops provide complete wheel servicing including recondition-

ing of wheels and axles in addition to new axle machining and finishing and axle downsiz-

ing. Component parts facilities recondition and manufacture railcar cushioning units, cou-

plers, yokes, side frames, bolsters and various other parts. Facilities also produce roofs,

doors and associated parts for boxcars

Leasing and Services

Greenbrier’s relationships with financial institutions, combined with our ownership of a

lease fleet of approximately 8,900 railcars enables it to offer operating leases and “by the

mile” leases to customers. The company frequently originates leases of railcars, which are

either newly built or refurbished by Greenbrier, or bought from the secondary market and

subsequently sold with attached leases to financial institutions. Greenbrier then provides

such institutions with management services under multi-year agreements. Assets from the

lease fleet are periodically sold to take advantage of market conditions, manage risk and

maintain liquidity.

The management services business offers a broad array of software and services that

include railcar maintenance management, railcar accounting services (such as billing and

revenue collection, car hire receivable and payable administration), total fleet manage-

ment (including railcar tracking using proprietary software), administration and railcar

remarketing. The company currently owns or provides management services for a fleet of

approximately 273,000 railcars for railroads, shippers, carriers, institutional investors and

other leasing and transportation companies in North America.

1

Freight Manufacturing 77.70%

Leasing & Services 12.60%

Other 9.70%

Revenue Segmentation

Backlog Highlights

Total manufacturing

backlog

27,500

units

Estimated future reve-

nue (millions) $3,200

Units scheduled for de-

livery in 2017 12,000

Marine backlog

(millions) $114

Covered hopper cars for

use in energy related

sand transportation 3,800 units

3. December 28, 2016

Industry Overview

Rail Manufacturing

The Rail Manufacturing industry manufactures equipment used pri-

marily in the transportation and freight segments. The aggregate

industry is segmented into two main groups, Equipment Manufac-

turing and Servicing. Equipment manufacturing is segmented into

four primary offerings: railcars, tankers, flatbeds, and marine barg-

es. These various equipment offerings are designed to ensure com-

panies are able to transport their goods regardless of being liquid,

or solid across the country, or globe.

Servicing is broken up into three categories, which includes after-

market refurbishment & repairs, management consulting, and leas-

ing.

Industry Valuation

The total industry market capitalization is $14.25 billion, with LTM

revenue totaling $14.04 billion. The average P/E multiple is 18.9x

and EV/EBITDA 7.1x.

From 2011 until 2014 GBX has remained relatively aligned to the

industry EV/EBITDA. Although, in mid-2014 GBX ‘s EV/EBITDA mul-

tiple fell below the industry average. The gap has since widened

over the last two years; this could be indicative of GBX’s relative

value.

Total Market Cap $14.25 B

TTM Revenue $14.04B

Relevant Industry Metrics

Industry Valuation

Metric GBX Peers

P/E 12.1x 18.9x

P/B 1.3x 1.1x

EV/Sales 0.7x 1.3xx

EV/EBITDA 4.8x 7.1x

4. December 28, 2016

Industry Overview (cont.)

Competitors

Greenbrier’s main competitors are Trinity Industries (TRN), American

Railcar Industries (ARII), and FreightCar America (RAIL). Trinity In-

dustries is the largest player in the industry, with a market capitaliza-

tion of $3.27B. Furthermore, TRN has the most diversified business

model along with industry leading margins.

American Railcar Industries (ARII) has a market capitalization of

$704M. Unlike GBX and TRN, ARII does not have a well-diversified

revenue stream, and as a result is more exposed and correlated to

the tanker and car market. ARII also offers a very limited offering of

intermodal transport, which increases cost associated with inefficien-

cy, and also increases the chances of damage to the products that

are being transported.

FreightCar America (RAIL) has the smallest market capitalization in

the industry. FreightCar America focuses on manufacturing aluminum

and steel bodied freight rail cars. The company also manufactures

parts and refurbishes railcars. FreightCar America’s primary custom-

ers are leasing companies and railroads.

Industry Returns

The graph below compares GBX’s 5-YR Returns (%) to the entire Rail

Manufacturing industry. Between the end of 2011 and the beginning

of 2013 GBX’s returns were below the industry average. In 2013

when oil hit $91.17/ barrel GBX and the industry achieved over 200%

returns. Despite the record high returns, when oil dropped in price

throughout 2014 until present (2016), revenues fell dramatically.

From the graph it can be inferred that Greenbrier and the industry

clearly have a positive correlation to the price of oil.

Competitor Highlights

Trinity Industries (TRN)

Biggest player in the industry

Most diversified business model

Industry leading margins

American Railcar Industries

(ARII)

Relatively more exposure and

correlation to the tanker car

market

Limited intermodal offerings

FreightCar America (RAIL)

All manufacturing

Similar manufactured product

offerings

-50%

0%

50%

100%

150%

200%

250%

300%

GBX 5Y Returns vs. Industry

Sources:

Company 10K

Earnings call

5. December 28, 2016

Management Overview

Chief Executive Officer, William Furman

William A. Furman is Chief Executive Officer and Chairman of the

Board of the Greenbrier. Mr. Furman has served Chief Executive Of-

ficer of the company since 1994, and as Chairman of the Board of

Directors of the company since January 2014. Mr. Furman was Vice

President of the Greenbrier from 1974 to 1994, and he currently

serves as a director of Schnitzer Steel Industries, Inc., a steel recy-

cling and manufacturing company1

.

Management compensation incentives tied to ROIC

Prior to 2014, Greenbrier’s Compensation Committee established per-

formance goals related to adjusted Corporate EBITDA for the purpos-

es of the company’s short-term cash incentive program for executive

officers. Beginning in FY 2014, the Committee adopted Corporate Re-

turn on Invested Capital (ROIC) as an additional financial perfor-

mance measure to determine executive compensation because ROIC

is more closely aligned with shareholder interests2

. ROIC has more

than doubled since the implementation of the plan, resulting in en-

hanced shareholder returns.

William A. Furman $3,025,095

Lorie L. Tekorius $851,545

Mark J. Rittenbaum $1,252,031

Alejandro Centurion $1,483,440

Victoria McManus $988,007

James T. Sharp $433,717

FY 2016 NEO Compensation

-5%

0%

5%

10%

15%

20%

25%

30%

$0

$10

$20

$30

$40

$50

$60

$70

$80

8/31/2006 8/31/2007 8/31/2008 8/31/2009 8/31/2010 8/31/2011 8/31/2012 8/31/2013 8/31/2014 8/31/2015

10YReturns vs. ROIC

Insiders’ Last Transaction

William A. Furman3

-20,450 shares

Lorie L. Tekorius -1,361 shares

Mark J. Rittenbaum -6,250 shares

Alejandro Centurion3

-3,162 shares

Victoria McManus3

-2,383 shares

James T. Sharp -2,996 shares

6. December 28, 2016

Strong Fundamentals in a Tough Environment

The decline of US oil has spared few

US oil production peaked in 2015, and since then, companies with

close ties to oil have seen steep declines in their stock prices. Green-

brier is no stranger to this phenomena; its stock price is down over

50% since September 2014. From 25% and 18% growth in 2014 and

2015, respectively, Greenbrier’s revenue growth grinded to an abrupt

halt in FY 2016, expanding just 2.85% YoY. Analysts expect revenue

to decline by over 20% over the next two years.

Healthy balance sheet will help weather the storm

Greenbrier’s management has kept net-debt levels fairly low at just

18% of LTM EBITDA, well below the industry average. The company

holds approximately $570 million in cash with a stable credit revolver

which allows Greenbrier to be extremely flexible during “softer” mar-

kets like the one the company currently finds itself in. Since Greenbri-

er’s board had implemented an executive compensation structure

tied to Return on Invested Capital, the company has generated an

ROIC of 23%, and management plans to keep this high level of re-

turn stable over the next year by strategically managing costs.

Historical Valuation

Despite the steep fall in Greenbrier’s stock price, the company

maintains its financial health. Management’s conservative use

of debt and its ability to squeeze out high returns out of every

dollar of invested capital have kept the company afloat during

this tough market environment. The overselling of GBX stock

had depressed its EV/EBITDA multiple to a 5-year low by the

end of 2015. Recently, the stock has picked up momentum, but

still trades below it’s 5-year multiple average.

Fundamental Data

Price-Based Multiples

Metric GBX Peers

P/E 12.1x 18.9x

P/B 1.3x 1.1x

EV/Sales 0.7x 1.3xx

EV/EBITDA 4.8x 7.1x

Metric GBX Peers

ROIC 22.95% 10.38%

Div. Yield 2.06% 3.03%

EBITDA Margin 17.0% 26.85%

Net Debt/

EBITDA

0.17 1.64

EBITDA/Interest

Exp.

— 7.19

FCF Yield 19.5% 9.5%

Asset Turnover 1.48 0.58

7. December 28, 2016

Diversifying Product Base and Revenue Stream

Expanding Product Base

GBX has been focusing on growing its intermodal railcar manufacturing seg-

ment. Intermodal units are specifically designed to be moved from railcars,

to trucks, and to large barges. This ensures a more efficient and secure

delivery of a wide range of products due to the ease of transporting the

intermodal unit. Greenbrier’s offering of intermodal railcars has significantly

expanded the company’s product base.

Geographical Diversification

The international rail manufacturing industry had a total revenue of

$14.04B. Domestic countries account for 95% of revenue, while interna-

tional companies only made up 5% of revenue. Greenbrier has the most

internationally diverse revenue stream amongst competitors, with the Unit-

ed States market comprising of 86% of total revenues, and international

businesses totaling 14% of revenues. Greenbrier has been utilizing its buy-

ing power to expand into emerging railcar markets in Europe, Brazil, and

Saudi Arabia. The Europe manufacturing facility uses advanced fabrication

technologies to provide a vast array of high quality railcars to a diverse set

of clients. The manufactured railcars cross a variety of different purposes

ranging from car wagons, all the way to tank wagons. In 2015, Greenbrier

agreed to purchase a 19.5% stake in Brazilian Rail manufacturer Amsted–

Maxion Hortolandia (AMH) for $15 million. The deal also allows Greenbrier

to purchase another 40% before September 2017. AMH controls an annual

70% market share of the South American railroad freight car market. This

could mean significant future growth for Greenbrier in the South American

market.

Leasing stabilizes cash flows

The leasing segment has become a favored revenue segment for rail manu-

facturers. The market typically assigns a higher multiple to companies that

earn a significant portion of their revenue from leasing because companies

that diversify their revenue stream through a leasing segment help manage

cyclical risk.

GBX ARII TRN RAIL

Freight

Manu-

facturing

77.70% 78.70% 84.80% 99.70%

Leasing

& Ser-

vices

12.60% 21.30% 13.80% 0.30%

Other 9.70% 0 1.40% 0

Revenue Segmentation

8. December 28, 2016

Industry Concerns May be Unjustified and/or Overstated

Oil Rigs Online

The US oil rig count has increased in the weeks leading up to the Nov. 30 OPEC meeting. Despite the lower US oil

prices, the industry has remained resilient. Extensive financing has been performed for operations in the Permian Ba-

sin, which is one of the more efficient basins for operations. The Permian rig count is currently up approximately 70%

since the end of April. The more shale basins such as Eagle Ford and Williston have not seen this level of increase,

but this still shows a sign of improvement in US oil production. This growth is likely to continue given the optimistic

agreement from the recent OPEC meeting.

Over-Reaction to Declining Oil Prices

The stock price of GBX has been significantly affected by the price of oil in recent years. The stock has lost much of

its gains from before the US oil production boom. The drop in US oil production due to the declining oil prices has

negatively affected the perception of the US railcar industry given the recent rise in the need for crude by rail trans-

portation. However, while prices have declined approximately 50% in the last two years, US oil production has only

dropped around 10% from its peak in early 2015 and has stabilized at current levels. The market also seems to be

pricing in a severe decrease in the railcar orders market. While we a decline is likely, we believe that the market

seems to be already pricing this drop in and is missing any potential upside.

Continuing Demand for Crude by Rail

Many of the more efficient oil rigs that are successful in a low price environment like we are in today utilize pipelines.

However, there will always be a need for crude by rail. Pipelines do decrease costs, but the political fallout can be

endless as we are currently seeing from the DAPL situation and have seen from the axing of the Keystone Pipeline.

Crude by Rail will be heavily relied for crude transportation from the Midwest to the gulf and transports to each coast.

Regulation

A new rule has been put in place that requires the retirement of DOT-111 tanker cars by 2017-2018. As of 2013, DOT

-111 tanker cars made up about 69% of the American tanker car fleet and about 80% of the Canadian tanker car

fleet. This is due to the high profile disasters that can follow any crude by rail accident considering the flammable

contents and the speed at which they travel. Greenbrier is set up well for this move, as its DOT-117 car was dubbed

“The Tank Car of the Future”. The Canadian transport minister has pushed the retirement deadline of DOT-111 cars

up 6 months due to the country’s reliance of crude by rail because of the nixing of the Keystone pipeline. Despite

these regulations Greenbrier has yet to see many orders come to fruition most likely due to the struggling operations

of oil producers. It seems that many of Greenbrier’s customers are merely kicking the can down the road since declin-

ing oil production has seen a decrease in tanker car orders.

9. December 28, 2016

Product Base Still Dependent on Oil and Not Yet Fully Diversified

Connection to Oil

The shale revolution and increase in US oil production brought upon unprecedented railcar orders for

Greenbrier in correlation with the crude by rail phenomenon. Railroads needed tanker cars and sand cars

in order to meet the rising production at many of the oil fields in the US. However, prolonged low crude

oil prices have forced many of the less efficient production operations to shut down. This is not a good

thing for Greenbrier as many of the more efficient oil rigs and basins utilize pipelines to transport oil.

Lacking Revenue Diversification

Currently, 80% of Greenbrier’s revenue comes from its manufacturing segment and 40% of this segment

revenue comes from tankers. Greenbrier does not break out what percentage of the tankers are crude

tanker cars, but it can be assumed that it has been a sizable portion in recent years. Also, the company

currently has 80%-90% of its revenue coming from the US meaning that it is very susceptible to any

economic shock that could worsen the decline of US oil production or US manufacturing.

Order Cancellations

During the last earnings call, Greenbrier announced the settlement on the order cancellation of 1,200

sand cars. This is worrisome because it points to the struggle of current fracking operations due to its

reliance on sand transports. Greenbrier states that they do not allow order cancellations, but say that

they work with their customers to find fitting accommodations during tough environments like we are

seeing today. This brings concern to how much can Greenbrier rely on its backlog, which is marketed as

very strong.

11. December 28, 2016

Must Rise above the Struggling Industry

▪ Expanded market share increases risk

Railcar manufacturing as an industry has stagnated after the boom in 2014-

2015 and will likely decline in the near future. Greenbrier is expecting this

but is not immune to industry wide concerns. In order for Greenbrier to be a

value pick, it must excel within the industry. In recent years, Greenbrier has

done just so, increasing its backlog market share from 13% to 30% and

maintaining a positive net income where its competitors have failed. This

increased market share does mean that Greenbrier is more susceptible to

industry wide risk and limits its ability to function as a niche supplier and

avoid macro issues. This is partially mitigated by Greenbrier’s new tankers

being some of the best for conforming to DOT 117 specification regulations,

as a decrease in demand will have less of an affect on Greenbrier. Tankers

in general are the second most common type of car behind covered hoppers

and make up 21% of all railcars currently being operated.

▪ Dependent on backlog staying healthy

A large part of Greenbrier’s potential upside comes from the fact that they

have a very strong backlog in tough market environment. This backlog cur-

rently sits at over 27,500 units valued at over $3.2 billion. If this backlog

were to shrink via canceled orders, Greenbrier would lose a significant

amount of future revenue and would lose one of its distinct advantages over

its competitors from an investor’s perspective. A significant loss of backlog is

unlikely as has never happened to Greenbrier to date, but it is possible if the

rail transportation industry severely underperforms or if Greenbrier’s reputa-

tion among its customers were to worsen for any reason. The primary con-

cern is that much of their future earnings are dependent on orders in the

future that can be canceled, although it is much more likely for orders to be

delayed rather than canceled.

▪ Not outperforming means possible heavy downside

There is a larger inherent risk when investing in a company within a strug-

gling, volatile industry. We believe Greenbrier has qualities that allow it to

be a value pick despite industry woes, but nevertheless, the company must

significantly outperform the competition in order for us to see real upside. If

it simply performs or even underperforms then the losses will likely be high-

er for Greenbrier than they would be for an investment in a similar relative

position within a different industry.

12. December 28, 2016

Valuation—Perpetuity Growth Method

Revenue Growth

Our conservative discounted cash flow model forecasts negative rev-

enue growth over the next four years. Analysts expect revenues to

decline nearly 20% YoY in 2017 and 2018. Based on Greenbrier’s

healthy backlog that management believes is stronger than it was

during the last “soft” market environment eight years ago, we expect

revenues to bottom out at $1.3bn in FY 2020. We do not foresee

much difficulty in Greenbrier’s ability to beat the extremely low ana-

lyst and market forecasts. Transportation by rail has been and will

continue to be a mainstay of American infrastructure, and so we be-

lieve growth will eventually normalize. President-Elect Donald

Trump’s effect on the industry’s growth is unclear. Investment in do-

mestic infrastructure should be a tailwind to manufacturers, but the

Republican controlled Congress may prove to be friendly to oil pipe-

lines, an obvious risk to railroad companies for the reasons we previ-

ously outlined.

Terminal Value

Our Terminal Value calculation considers Greenbrier’s excess returns

and it’s industry-leading return on invested capital using the formula

below:

Our selected perpetuity growth rate of 1.6% is intended to reflect the

growth rate at a normalized point in the business cycle, which we

estimate to be around the rate of inflation. Again, this conservative

number should not be difficult to beat.

Discount Rate

Greenbrier’s forecasted cash flows and terminal value are discounted

at 11%, it’s weighted average cost of capital according to Bloomberg.

Valuation

Our DCF model returned a value of $42.71 per share of GBX stock.

Discount Rate 11.03%

5Y Revenue CAGR -7.65%

5Y Avg. EBITDA Margin 11.97%

Perpetuity Growth Rate 1.6%

Reinvestment Rate 6%

Key Assumptions

Summary

Enterprise Value 1,612 M

Less: Non-Equity In-

terests (224 M)

Equity Value 1,388M

Equity Value Per

Share $42.71

Current Price $40.70

Upside/(Downside) 5%

Comparable Companies

Company

Forward EV/

EBITDA

Forward

P/E

Greenbrier 7.7x 21.8x

Trinity 7.4x 22.8x

American

Railcar 7.4x 14.0x

FreightCar 9.4x 61.7x

Average 8.0x 28.9x

GBX Implied

Share Price $58.37 $45.50

Upside/

(Downside) 43.92% 11.79%

13. December 28, 2016

Value Risks to the Downside

Revenue

Oil prices stay lower for longer and fewer drillers are produc-

ing oil

As oil rigs come back online, the time between discovery and

oil in the barrel takes longer than anticipated

A potentially friendly stance towards oil pipelines by the

Trump administration

Oil pipelines continue to capture market share from rail trans-

portation

An interest rate hike, and in turn a stronger US dollar, puts

downward pressure on oil prices

Inflationary concerns, sparked by the election of Donald

Trump, materialize, resulting in higher oil prices to the point

where producers have trouble remaining competitive

Costs

Unfulfilled backlog orders can result in potentially large inven-

tory write-downs.

A stronger US dollar dampens the advantages of sourcing rev-

enue from oversees, creating foreign exchange losses

Terminal Value

The terminal value used in our DCF makes up 60% of our val-

uation

Management could have difficulty in reaching their 25% ROIC

target

Our selected perpetuity growth rate (1.6%) is a highly subjec-

tive figure

Higher than anticipated revenue declines will negatively im-

pact terminal year cash flow and therefore terminal value

Discount Rate 11.03%

5Y Revenue CAGR -7.65%

5Y Avg. EBITDA Margin 11.97%

Perpetuity Growth Rate 1.6%

Reinvestment Rate 6%

Key Assumptions

Summary

Comparable Companies

Company

Forward EV/

EBITDA

Forward

P/E

Greenbrier 7.7x 21.8x

Trinity 7.4x 22.8x

American

Railcar 7.4x 14.0x

FreightCar 9.4x 61.7x

Average 8.0x 28.9x

GBX Implied

Share Price $58.37 $45.50

Upside/

(Downside) 43.92% 11.79%

Enterprise Value 1,612 M

Less: Non-Equity In-

terests (224 M)

Equity Value 1,388M

Equity Value Per

Share $42.71

Current Price $40.70

Upside/(Downside) 5%