Downloaded 120 times

![195

Measurement of listenership

remained an issue

Listenership measurement remains a challenge- except

for the four metros where Radio Audience Measurement

(RAM) data is available, listenership measurement is the

biggest pressing challenge in other cities. At present,

the segment is using social media platforms and their

own surveys to overcome the absence of a credible

measurement system. In order to overcome issues in

measuring listenership, MRUC in association with AROI

is inviting proposals to form an independent body that

will measure listenership in the top few markets. Initially

the plan is to cover 21 markets and the methodology

for research will be similar to what IRS uses now.

16. http://pib.nic.in/newsite/PrintRelease.aspx?relid=187301

17. Industry discussions

Future outlook

Growth will accelerate in 2019

Ad spends in the upcoming general and state

elections, non-FCT revenues and firming of ad rates

in regional markets will fuel growth in 2019.

Radio brands will be leveraged more

Radio will enable more growth through brand

leverage, across concerts, branded content, digital

content and delivery, events and activations,

podcasts, etc. The industry would drive up to 20%17

of topline from non-FCT revenues by 2021.

Radio and audio streaming will

increase collaboration

Radio companies will focus on building communities on

[radio + digital] media, to understand consumers better,

end enable brands to connect with their audiences directly.

Combinations between radio players and streaming apps will

be tried to increase fill rates on streaming audio platforms

and sell segmented audiences to advertisers. There will

be an increase in multi-media offerings to advertisers.

News was finally permitted on

private FM, but with heavy caveats

Private FM was finally permitted to air news, but only in

the form or replays of news broadcasts created by Prasar

Bharti, without any modifications16

. No such restrictions

exist on other media like television, digital or print in India.](https://image.slidesharecdn.com/ey-a-billion-screens-of-opportunity-190312110559/85/Ey-a-billion-screens-of-opportunity-195-320.jpg)

![Expert

speak

The unique ability of radio to seamlessly integrate with

emerging digital platforms has driven innovative and path

breaking programming in radio content. Brands have

recognized the potential of radio by using it along with

other mediums like TV and print. Owing to the change in

consumption patterns and growing GDP as compared to last

year, radio will certainly witness a double digit growth.

Ashit Kukian

CEO, Radio City

In 2019, the radio segment will emerge as a much stronger

medium. Radio is constantly innovating and integrating

its content with digital. The sector needs to change the way

it sells and [radio plus digital] is a potent combination for

advertisers.

Nisha Narayanan

COO & Director, Red FM

I am confident FM radio will the fastest growing traditional

media in the years to come. Radio brands will also diversify

and become multi media content producers, reaching

audiences through radio, video, SM all.

Prashant Panday

Managing Director & CEO, Entertainment Network

(India) Ltd.

M&A will be the only way to ensure double digit topline

and EBITDA growth in a tough media market overall. In

the absence of new licenses, radio players will enter digital

music streaming to improve reach.

Vineet Hukmani

MD and CEO, Radio One](https://image.slidesharecdn.com/ey-a-billion-screens-of-opportunity-190312110559/85/Ey-a-billion-screens-of-opportunity-200-320.jpg)

![Media and entertainment

Recent major develop-

ments in the M&E sector

Privacy and Data Protection

2018 has been a watershed year for privacy and data

protection jurisprudence in India. A summary of the

recent key developments in this space is provided below.

Right to Privacy Judgement

In Justice K S Puttaswamy (Retd.) & Anr. v. Union of India &

Ors., dated August 24, 2017 (“Right to Privacy Judgment”)

a Constitution Bench comprising of nine judges of the

Supreme Court of India (“SC”) unanimously upheld the

right to privacy as a fundamental right guaranteed under

Part III of the Constitution of India (“Constitution”).

Perhaps more importantly, the SC ruled that informational

privacy forms part of the right to privacy, confirmed that it

was a horizontal right (i.e., a right capable of being applied

against private persons) and required the formulation of

comprehensive legislation to protect rights of individuals1

.

Justice Srikrishna Committee on Personal

Data Protection

The Ministry of Electronics and Information Technology

(“MEITY”) constituted a Committee of Experts on July 31,

2017 under the Chairmanship of Justice B.N. Srikrishna

(Retd.) (“Committee”) to recommend a data protection

framework in India, and propose a draft data protection

bill. Pursuant to its mandate, the Committee released the

draft of the Personal Data Protection Bill, 2018 (“PDP

Bill”) along with its corresponding report in July 2018.

The PDP Bill requires that all data fiduciaries (entities

responsible for determining the purpose of processing of

data), process personal data of individuals in a fair and

reasonable manner, respecting the privacy of the individual,

and only for lawful specific purposes. Further, personal

data is permitted to be collected and stored only to the

extent, and for the period, necessary to fulfill the purpose

of its collection. Additionally, the PDP Bill prescribes the

implementation of ‘privacy by design’ that is every data

fiduciary will have to design their information technology

architecture and processes in a manner that will anticipate

and avoid harm to the data principal. Interestingly, the

PDP Bill has defined a ‘child’ to mean any data principal

who is below the age of eighteen years. This is significant

as the PDP Bill provides for the classification of data

fiduciaries whose websites or services are directed at

children or those data fiduciaries who process large

volumes of personal data of children as ‘guardian data

fiduciaries’, and prohibits them from profiling, tracking,

monitoring of, or targeting advertising at, children.

The PDP Bill also contemplates the creation of a sector

agnostic regulator called the Data Protection Authority of

India with wide powers of monitoring and enforcement,

standard setting, grievance redressal and adjudication.

While personal data may be transferred outside India

under specific conditions, a live, mirror copy of the data

must be stored within India. Moreover, the PDP Bill also

provides that ‘critical personal data’ (to be notified by

the Central Government) must only be stored in India.

Aadhaar Judgement

The SC pronounced its judgement on the Aadhaar

(Targeted Delivery of Financial and Other Subsidies,

Benefits and Services) Act, 2016 (“Aadhaar Act”) on in

Justice K S Puttaswamy (Retd.) & Anr. v. Union of India &

Ors., dated September 26, 2018 (“Aadhaar Judgement”)2

which has a significant impact on privacy law in India.

The judgment has far reaching consequences for businesses

(especially those that are mandated to undertake KYC

under applicable law), as it read down Section 57 of the

Aadhaar Act and therefore, removed the ability of companies

and individuals to seek to authenticate the identity of

personnel on the basis of contractual provisions. However,

the Court left intact the portion of Section 57 which

enables the collection of Aadhaar information to establish

the identity of a person for a purpose backed by a law.

Intermediary Guidelines

MEITY released the draft Information Technology

[Intermediaries Guidelines (Amendment) Rules], 2018

(“Draft Rules”) on December 24, 2018, under Section 79

of the Information Technology Act, 2000 (“IT Act”) for

public consultation and feedback. The Draft Rules propose

an entity localization requirement for all intermediaries with

above five million users and entities specifically notified

by the Government. Accordingly, intermediaries who fall

within the criteria outlined above will now need to comply

with all relevant statutory obligations, such as inter alia,

regulatory compliance and filings under the Companies Act

and labour law compliances. Crucially, this will also trigger

attendant tax obligations because such incorporation will

create a ‘permanent establishment’ for the purposes of

taxation. Furthermore, the Draft Rules would also require

intermediaries to deploy technology based automated tools

or appropriate mechanisms, with appropriate controls,

for proactively identifying and removing or disabling

public access to unlawful information or content.

1. Justice K S Puttaswamy (Retd.) & Anr. v. Union of India & Ors., (2017) 10

SCC 1.

2. Writ Petition (Civil) No. 494 of 2012.](https://image.slidesharecdn.com/ey-a-billion-screens-of-opportunity-190312110559/85/Ey-a-billion-screens-of-opportunity-272-320.jpg)

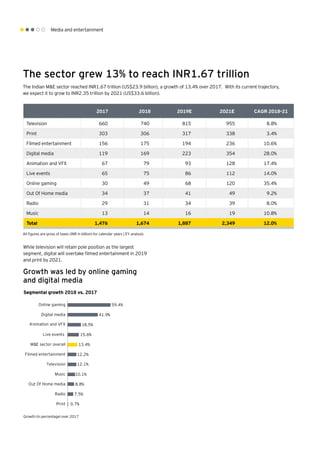

The media and entertainment sector in India grew 13.4% in 2018 to reach INR1.67 trillion. Digital media saw the highest growth of 59.4% followed by online gaming which grew 41.9%. Advertising grew faster than subscription with advertising growing 12.7% and subscription growing 11.2%. Digital subscription grew significantly by 262% as more Indians started paying for online content. The demand for original digital content also increased. Traditional sectors like television and films grew around the industry average. Overall, the sector continued to outperform India's nominal GDP growth.