Punto de entrada de carga de las Américas: creando crecimiento económico

Vietnam port profile

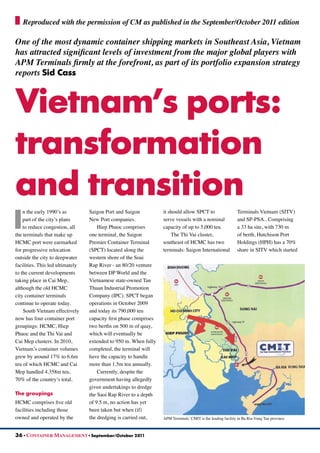

1. I

n the early 1990’s as

part of the city’s plans

to reduce congestion, all

the terminals that make up

HCMC port were earmarked

for progressive relocation

outside the city to deepwater

facilities. This led ultimately

to the current developments

taking place in Cai Mep,

although the old HCMC

city container terminals

continue to operate today.

South Vietnam effectively

now has four container port

groupings: HCMC, Hiep

Phuoc and the Thi Vai and

Cai Mep clusters. In 2010,

Vietnam’s container volumes

grew by around 17% to 6.6m

teu of which HCMC and Cai

Mep handled 4.358m teu,

70% of the country’s total.

The groupings

HCMC comprises five old

facilities including those

owned and operated by the

Saigon Port and Saigon

New Port companies.

Hiep Phuoc comprises

one terminal, the Saigon

Premier Container Terminal

(SPCT) located along the

western shore of the Soai

Rap River - an 80/20 venture

between DP World and the

Vietnamese state-owned Tan

Thuan Industrial Promotion

Company (IPC). SPCT began

operations in October 2009

and today its 790,000 teu

capacity first phase comprises

two berths on 500 m of quay,

which will eventually be

extended to 950 m. When fully

completed, the terminal will

have the capacity to handle

more than 1.5m teu annually.

Currently, despite the

government having allegedly

given undertakings to dredge

the Saoi Rap River to a depth

of 9.5 m, no action has yet

been taken but when (if)

the dredging is carried out,

it should allow SPCT to

serve vessels with a nominal

capacity of up to 5,000 teu.

The Thi Vai cluster,

southeast of HCMC has two

terminals: Saigon International

Terminals Vietnam (SITV)

and SP-PSA.. Comprising

a 33 ha site, with 730 m

of berth, Hutchison Port

Holdings (HPH) has a 70%

share in SITV which started

36 • CONTAINER MANAGEMENT • September/October 2011

One of the most dynamic container shipping markets in Southeast Asia, Vietnam

has attracted significant levels of investment from the major global players with

APM Terminals firmly at the forefront, as part of its portfolio expansion strategy

reports Sid Cass

Vietnam’s ports:

transformation

and transition

Reproduced with the permission of CM as published in the September/October 2011 edition

APM Terminals’ CMIT is the leading facility in Ba Ria-Vung Tau province

2. September/October 2011 • CONTAINER MANAGEMENT • 37

operations in August 2010.

Although it has a 14 m depth

alongside, the access channel

has less than 12 m, since

dredging projects have not

been extended to the facility.

The SP-PSA terminal

is a joint venture between

Saigon Port, Vietnam

National Shipping Lines

(Vinalines) and PSA Vietnam

that started operations in

2009 as Vietnam’s first

deep-sea container terminal.

Strategically located near the

mouth of the Cai Mep-Thi

Vai River, SP-PSA hopes

to become a major hub for

regional transhipment activity.

The terminal currently has

600 m of berth with 14.5 m

water depth (though the access

channel is only 12 m), and a

further 600 m extension is at

the planning stage. When both

phases (1,200 m of berths)

are fully completed, SP-PSA

will have a projected annual

capacity of over 2m teu.

The Cai Mep cluster in

Ba Ria-Vung Tau province

80 kms southeast of HCMC,

comprises three existing

terminals (TCCT, TCIT and

CMIT) and three terminals

currently under construction.

The Tan Cang-Cai Mep

Container terminal (TCCT) is

wholly-owned by Saigon New

Port Company and it began

operations in June 2009. TCCT

has a total berth length of 300

m and a throughput capacity

of 600,000 teu/annum.

Tan Cang–Cai Mep

International Container

Terminal (TCIT) is a joint

venture between Hanjin, MOL,

Wan Hai and Saigon Newport.

The facility, which has a 14 m

depth alongside but only a 12

m access channel, commenced

operations in January 2011.

TCIT has two berths with

a total length of 590 m and

40 ha of container yard, and

is equipped with six post-

Panamax cranes and 20 RTGs.

In early 2011, APM

Terminals opened its Cai Mep

International Terminal (CMIT)

which is claimed to be the only

container facility in Vietnam

capable of handling vessels

up to 15,000 teu capacity

and as a result, it caters for

the majority of the country’s

Europe/US long haul trades.

Representing an investment of

around US$270m, CMIT has

an annual container throughput

capacity of 1.1m teu, with

16.5 m depth alongside and a

14 m channel that is planned

to be dredged to 16.5 m in

the medium term. Currently

equipped with four super

post-Panamax container

cranes, another on order

and the purchase of a sixth

crane under review, CMIT

also offers more than 36

hectares of container yard.

The terminal is a 49%/51%

venture between APM

Terminals and local state-

owned companies Vietnam

National Shipping Lines

(Vinalines) and Saigon Port

and it handled its first vessel

in March 2011 with the call

of the 11,388 teu CMA CGM

Columba which to date, is still

the largest container vessel

to call at a Vietnamese port.

In August, 2011 the 9,038

teu capacity Grete Maersk was

the first Maersk Line vessel to

call at CMIT on its route from

Asia to North America. With

this first direct “Transpacific

6” (TP6) call, Maersk Line

officially became a business

partner of its sister company

APM Terminals, one of the

three main investors in CMIT.

Meanwhile, US-based

operator SSA Marine has

invested in the SP-SSA

International Container

Terminal (SSIT) at Cai Mep.

SSIT is a joint venture between

Saigon Port, SSA International

Holdings – Vietnam and

Vinalines. Construction work

is now under way on the new

1.2m teu capacity facility,

which will have two berths

on a 600 m quayline able to

accommodate 10,000+ teu

vessels (with 600 m allocated

as dedicated barge berths).

The terminal will have 14

m depth alongside, and

will be equipped with four

ship-to-shore super post-

Panamax container cranes

and 16 eRTGs. Operations

are scheduled to commence/

end 2011/early 2012.

Why are major global

operators scrambling to

invest in Vietnam’s ports?

Malcolm Gregory, CMIT’s

head of marketing reasons that

double-digit annual growth

business profile

The 9,038 teu capacity Grete Maersk was the first Maersk Line vessel to call at CMIT

3. since 2004 has now doubled

throughput to more than 4.3m

teu and growth is forecast

to continue at between 15%

and 18% annually to 9m teu

by 2015. “This is mainly

due to US and European

manufacturers and importers

diversifying their production

and supply lines from China

to Vietnam as China becomes

increasingly more expensive.

Vietnamese labour is highly

competitive, intelligent,

productive and very resilient:

GDP is growing around

7.5% a year and has been for

many years despite the global

recession and it is a well-

balanced market in terms of

imports/exports with imports

primarily from Asia and

exports to US/Europe,” he said.

Until the development of

facilities beyond HCMC no

deepsea mainline container

vessels were able to call at

Vietnam. “Until two years

ago, the largest vessels to

call at Vietnam were around

1,500 to 1,800 teu whereas

today for example, CMIT is

now receiving vessels up to

11,500 teu with the potential

to handle vessels up to 15,000

teu.,” Gregory added.

Safe investments and

political will

Investment in Vietnam seems

to be relatively safe although

there are still high levels of

bureaucracy which can cause

frustrations and significant

delays. However, according to

Gregory, APMT has enjoyed

good working relationships

with all levels of government,

“And any problems that we

experience are dealt with to

our satisfaction,” he said.

This is a far cry from

the mid-early 1990s when

the then called P&O Ports

International outlined the

difficulties of investing in

Vietnam, citing that the lead-

time from preparation of tender

documents through concession

award to eventual start-up was

normally between two and

three years. Proceedings were

often delayed by a combination

of lack of confidence on the

part of government officials,

political considerations,

lack of an appropriate legal

framework, or simply a lack of

will on the part of government

to complete the process.

P&O Ports, in fact, was

initially invited by The Ho

Chi Minh People’s Committee

to tender for a joint venture

in Ben Nghe Port and was

eventually chosen from six

bidders after a long period

of deliberation. After a

year of getting nowhere

during which P&O Ports

had not even reached the

stage of completing the

first document, let alone

a management contract or

joint venture agreement in

which ‘unacceptable risks

and returns were proposed’,

the company cancelled its

interest in the concession..

The experience of P&O

Ports was not unique, as

demonstrated by the Mitsui

joint venture in Ho Chi Minh

City which overran its budget

by two and a half times, due

to bureaucratic delays.

“Today’s change in

government approach has

largely come about through

successive governments’

recognition that ports are a

strategic necessity and are vital

for the future development of

the country,” said Gregory.

“The need is to reinforce

an international perception

that inward investments are

safe and that the government

must be seen to deliver on

its promises that Vietnam is

a secure and reputable place

in which to do business. If

foreign investors are frightened

or cannot make a sensible

return on their investments

there will be no more foreign

investment which would be

catastrophic for the country.”

Learning curve

“We have been very impressed

with the quality of available

labour which is educated and

hard working and we have

been surprised at how easy

it has been to find those with

the skills and willingness to

learn. The crane drivers for

example, have been trained in

CMIT simulators and at other

APMT’s facilities around the

region but what we of a certain

age have to remember, is that

the youngsters of today grow

up with electronic games

and computers and so forth

and they adapt to simulators

like ducks to water, unlike

some of us oldies, he said”

The biggest problem for

APMT is trying to instil safety

into the mindset of labour. It

is not part of the culture, as

can be seen by a walk around

any town and observing how

people ride their motorbikes

or cross the road, for example.

“Significant company attention

is continually focussed on

safety and while there have

been no problems or safety

issues, it is an aspect that needs

constant attention. However,

this is more than offset by

a lack of labour militancy,

flexibility and reliability,”

Gregory concluded. n

38 • CONTAINER MANAGEMENT • September/October 2011

business profile

Since 2004 throughput doubled to more than 4.3m teu and 15% and 18% annual

growth is forecast to continue to 9m teu by 2015

Malcolm Gregory, CMIT’s head of

marketing