RPBA Infographic: NHR case-studies - Updated: 09.11.2022

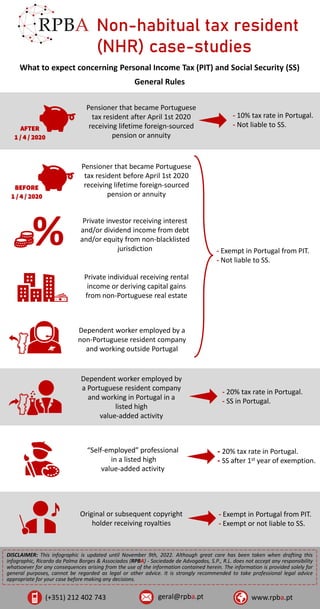

The Portuguese non-habitual tax resident (NHR) regime is granted to individuals who become resident for tax purposes in Portugal. This regime may grant an exemption on certain foreign source income as well as a 20% tax rate on employment and self-employment income deriving from high value-added activities during 10 years. Entrants into the NHR regime that became Portuguese tax residents after April 1st 2020 are subject to a flat tax rate of 10% on foreign-sourced pensions (instead of the previous exemption), as well as on other payments, such as pre-retirement benefits and "lump-sum" payments from pension funds and similar retirement schemes. It targets non-resident individuals who are likely to establish residence in Portugal. View a few standard case studies on this RPBA’s infographic.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to RPBA Infographic: NHR case-studies - Updated: 09.11.2022

Similar to RPBA Infographic: NHR case-studies - Updated: 09.11.2022 (20)

Recently uploaded

Recently uploaded (20)

RPBA Infographic: NHR case-studies - Updated: 09.11.2022

- 1. Pensioner that became Portuguese tax resident before April 1st 2020 receiving lifetime foreign-sourced pension or annuity Non-habitual tax resident (NHR) case-studies What to expect concerning Personal Income Tax (PIT) and Social Security (SS) General Rules Private investor receiving interest and/or dividend income from debt and/or equity from non-blacklisted jurisdiction - Exempt in Portugal from PIT. - Not liable to SS. Private individual receiving rental income or deriving capital gains from non-Portuguese real estate Original or subsequent copyright holder receiving royalties - Exempt in Portugal from PIT. - Exempt or not liable to SS. Dependent worker employed by a non-Portuguese resident company and working outside Portugal “Self-employed” professional in a listed high value-added activity - 20% tax rate in Portugal. - SS after 1st year of exemption. Dependent worker employed by a Portuguese resident company and working in Portugal in a listed high value-added activity - 20% tax rate in Portugal. - SS in Portugal. (+351) 212 402 743 geral@rpba.pt www.rpba.pt % DISCLAIMER: This infographic is updated until November 9th, 2022. Although great care has been taken when drafting this infographic, Ricardo da Palma Borges & Associados (RPBA) - Sociedade de Advogados, S.P., R.L. does not accept any responsibility whatsoever for any consequences arising from the use of the information contained herein. The information is provided solely for general purposes, cannot be regarded as legal or other advice. It is strongly recommended to take professional legal advice appropriate for your case before making any decisions. Pensioner that became Portuguese tax resident after April 1st 2020 receiving lifetime foreign-sourced pension or annuity - 10% tax rate in Portugal. - Not liable to SS. BEFORE 1 / 4 / 2020 AFTER 1 / 4 / 2020