Downloaded 22 times

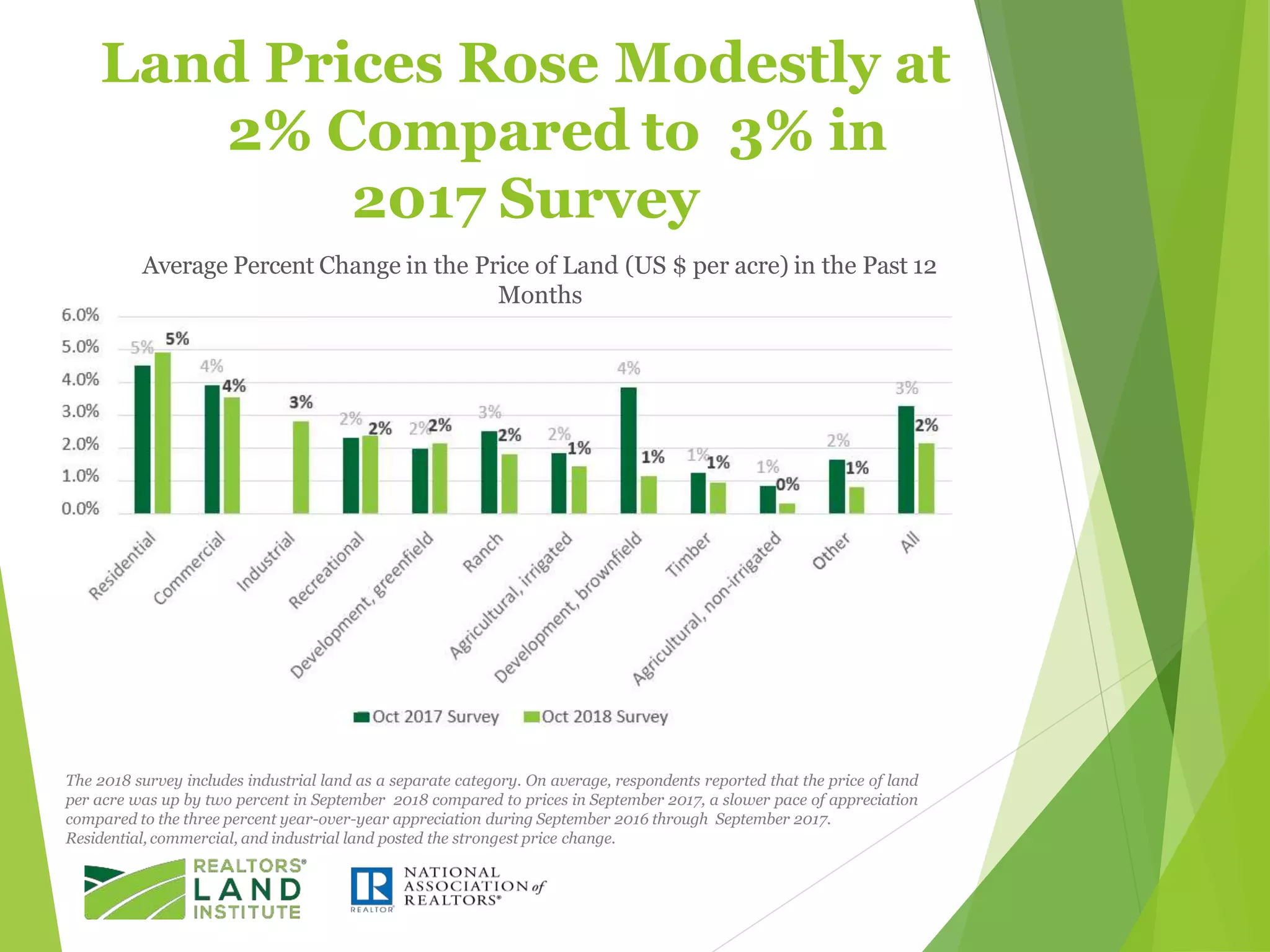

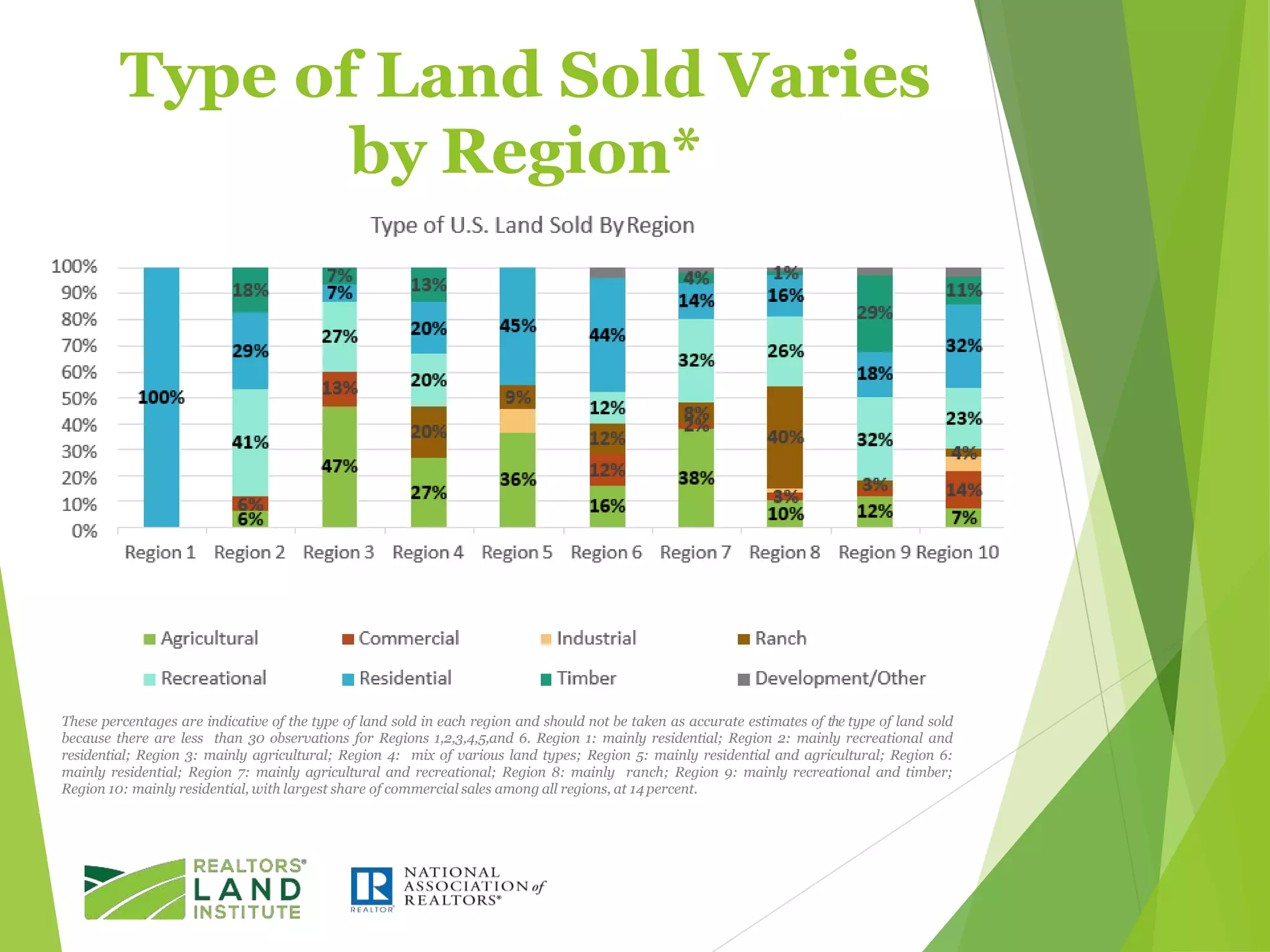

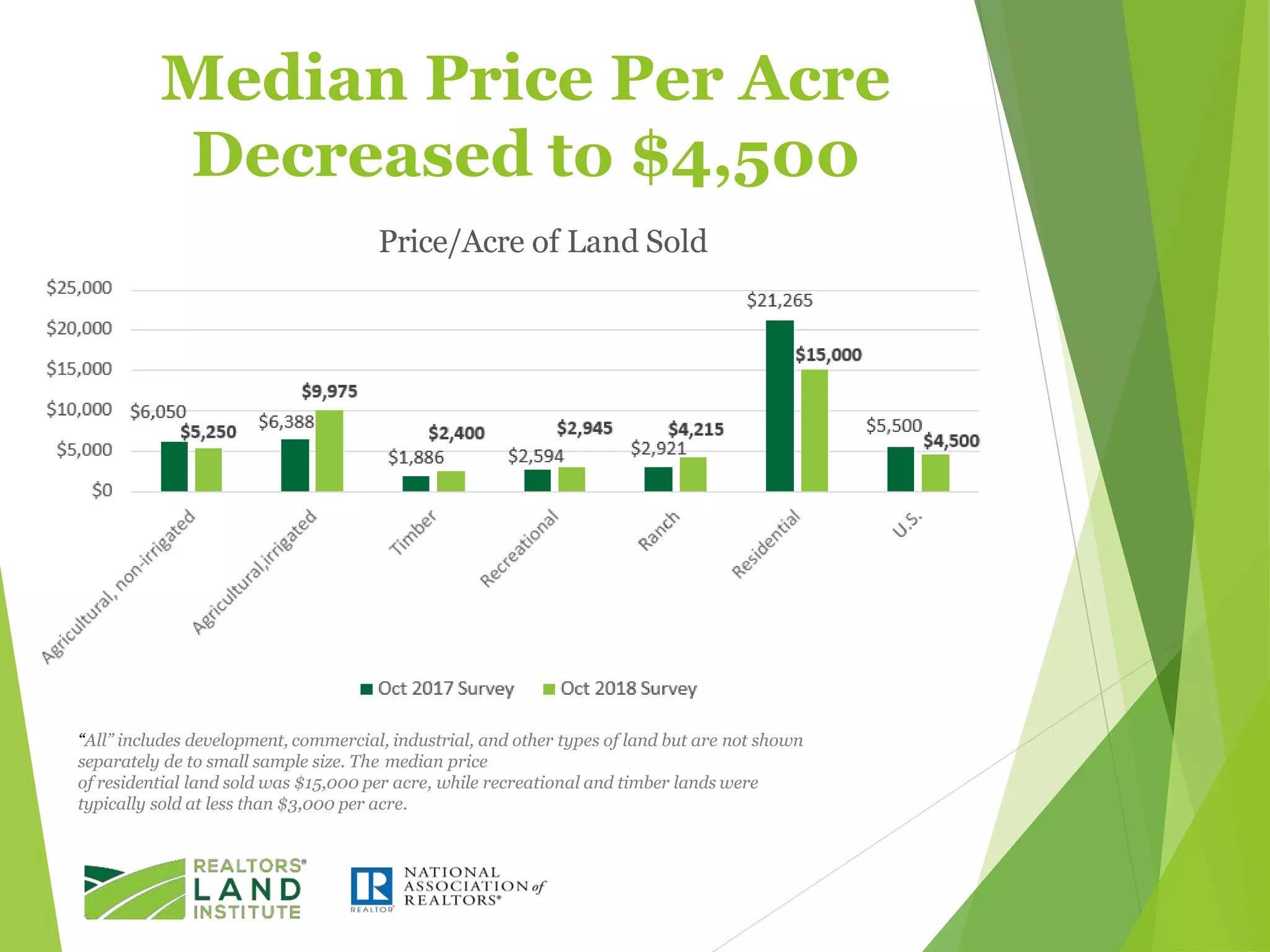

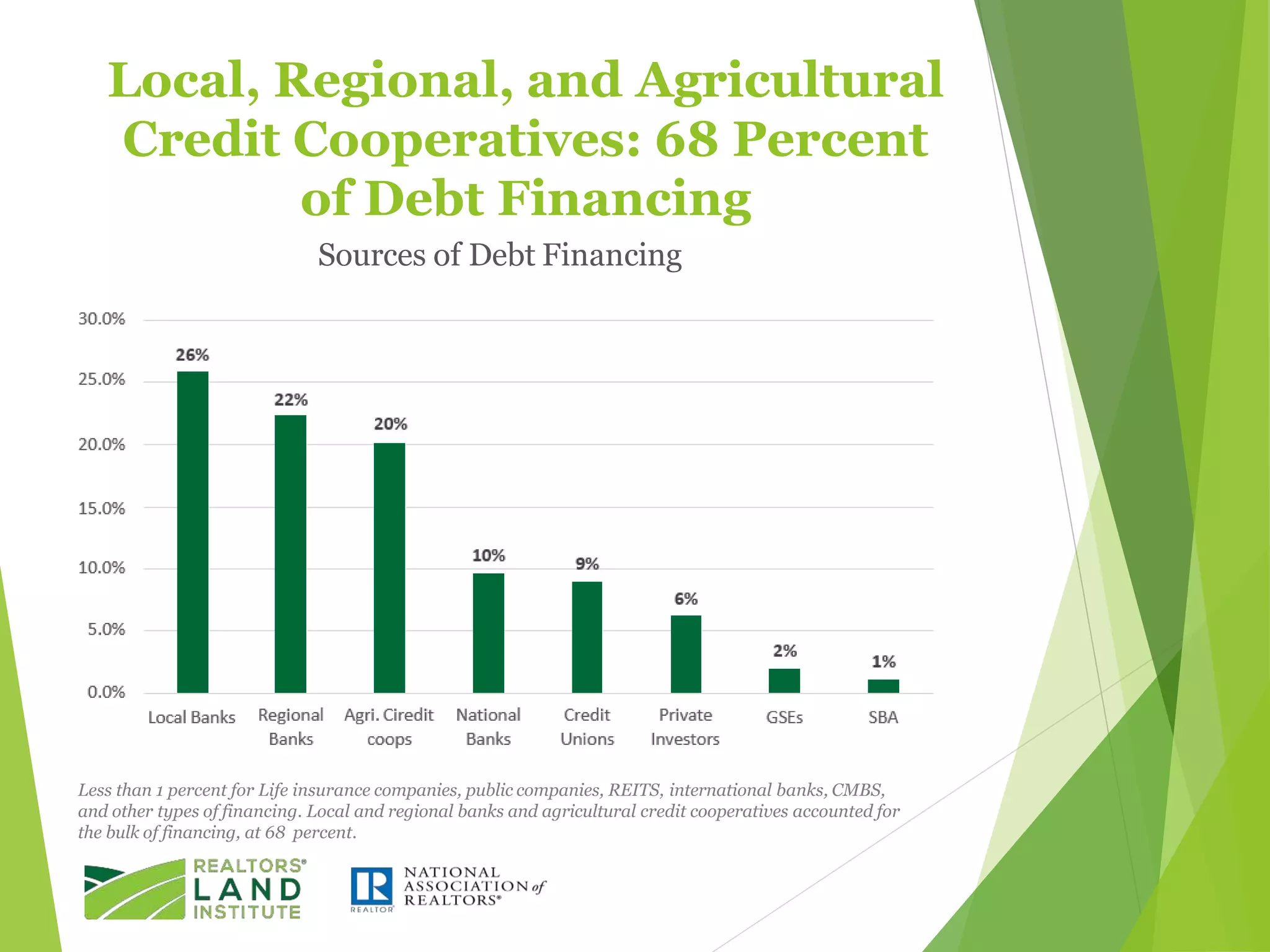

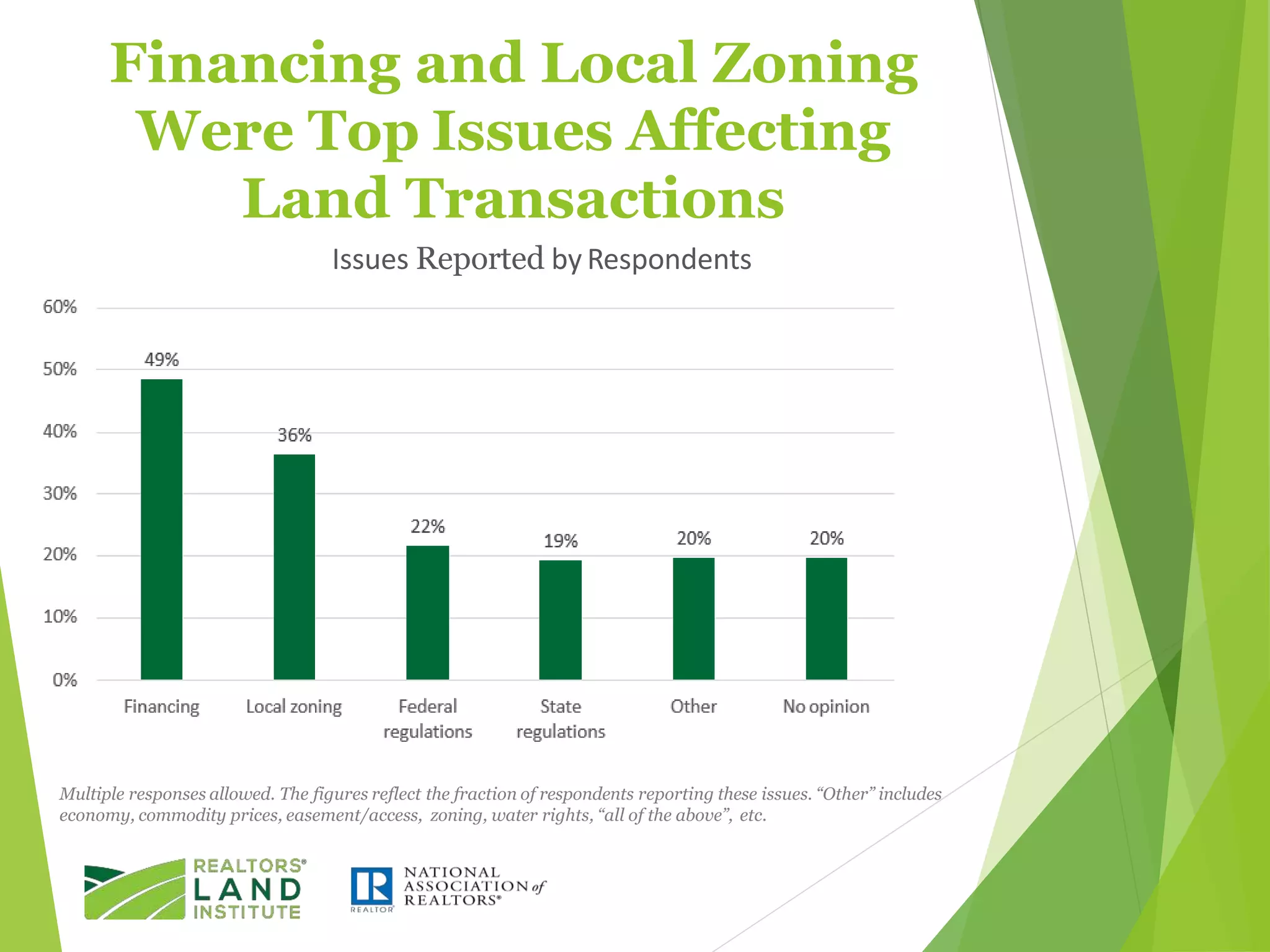

The 2018 Land Market Survey found that while economic growth strengthened in 2018, the land market saw more modest gains. On average, respondents reported a 2% year-over-year increase in land sales volume and a 2% increase in land prices, slower than the prior year. Regions 7-10 accounted for 80% of U.S. land sales. Residential and recreational land made up 55% of sales. Median land price fell to $4,500/acre while typical land transaction value decreased to $238,500. Financing and zoning issues were the primary challenges reported.