Vces 2013 - Problems in Implementation by CA Ritul Patwa, Jaipur

Cost Audit-Construction industry

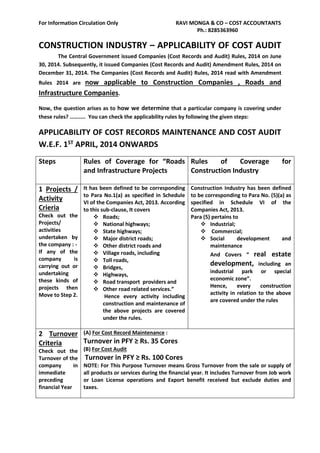

1. For Information Circulation Only RAVI MONGA & CO – COST ACCOUNTANTS

Ph.: 8285363960

CONSTRUCTION INDUSTRY – APPLICABILITY OF COST AUDIT

The Central Government issued Companies (Cost Records and Audit) Rules, 2014 on June

30, 2014. Subsequently, it issued Companies (Cost Records and Audit) Amendment Rules, 2014 on

December 31, 2014. The Companies (Cost Records and Audit) Rules, 2014 read with Amendment

Rules 2014 are now applicable to Construction Companies , Roads and

Infrastructure Companies.

Now, the question arises as to how we determine that a particular company is covering under

these rules? .......... You can check the applicability rules by following the given steps:

APPLICABILITY OF COST RECORDS MAINTENANCE AND COST AUDIT

W.E.F. 1ST APRIL, 2014 ONWARDS

Steps Rules of Coverage for “Roads

and Infrastructure Projects

Rules of Coverage for

Construction Industry

1 Projects /

Activity

Crieria

Check out the

Projects/

activities

undertaken by

the company : -

If any of the

company is

carrying out or

undertaking

these kinds of

projects then

Move to Step 2.

It has been defined to be corresponding

to Para No.1(a) as specified in Schedule

VI of the Companies Act, 2013. According

to this sub-clause, It covers

Roads;

National highways;

State highways;

Major district roads;

Other district roads and

Village roads, including

Toll roads,

Bridges,

Highways,

Road transport providers and

Other road related services.”

Hence every activity including

construction and maintenance of

the above projects are covered

under the rules.

Construction Industry has been defined

to be corresponding to Para No. (5)(a) as

specified in Schedule VI of the

Companies Act, 2013.

Para (5) pertains to

Industrial;

Commercial;

Social development and

maintenance

And Covers “ real estate

development, including an

industrial park or special

economic zone”.

Hence, every construction

activity in relation to the above

are covered under the rules

2 Turnover

Criteria

Check out the

Turnover of the

company in

immediate

preceding

financial Year

(A) For Cost Record Maintenance :

Turnover in PFY ≥ Rs. 35 Cores

(B) For Cost Audit

Turnover in PFY ≥ Rs. 100 Cores

NOTE: For This Purpose Turnover means Gross Turnover from the sale or supply of

all products or services during the financial year. It includes Turnover from Job work

or Loan License operations and Export benefit received but exclude duties and

taxes.

2. For Information Circulation Only RAVI MONGA & CO – COST ACCOUNTANTS

Ph.: 8285363960

.

Duties of the Companies

(in relation to provisions of Section 148 of the Companies Act, 2013

and the rules framed there under)

Steps What to do?

1 Appoint a Cost Auditor within 180 days of the commencement of

every financial year;

2 Inform the cost auditor concerned of his or its appointment;

3 File a notice of such appointment with CG within a period of 30 days

of the Board Meeting in which such appointment is made or within a

period of 180 days of the commencement of the financial year,

whichever is earlier, through electronic mode, in e-form CRA – 2,

along with the fees as specified in Companies (Registration Offices

and Fees) Rules, 2014;

4 Within a period of 30 days from the date of receipt of a copy of the

cost audit report, furnish the CG with such report alongwith full

information and explanation on every reservation or qualification

contained therein, in form CRA – 4 along with the fees as specified in

Companies (Registration Offices and Fees) Rules, 2014;

Consequences for Non-Compliance of Section 148

Section 148(8) states that if any default is made in complying with the provisions of

section 148, the company and every officer of the company who is in default shall be

punishable in the manner as provided in Section 147(1).

Section 147(1) states that the company shall be punishable with fine which shall not be

less than Rs. 25,000 but which may extend to Rs. 5,00,000/- and every officer of the

company who is in default shall be punishable with imprisonment for a term which may

extend to One Year or with fine which shall not be less than Rs. 10,000/- but which may

extend to Rs. 1,00,000/- or with both.

3. For Information Circulation Only RAVI MONGA & CO – COST ACCOUNTANTS

Ph.: 8285363960

Nature of Defaults under section 148

Non- maintenance of cost records;

Cost Auditor has not been appointed by the company;

Late appointment of cost auditor;

Cost auditor appointed but CRA – 2 form has not been filed with MCA;

Cost auditor appointed but cost records were not submitted for Cost Audit;

Non-cooperation regarding the timely completion of cost audit;

Cost Audit report not approved within the specified time limit and

Cost Audit report approved but not submitted to CG by the company.

Feel free to ask any query in respect of above rules or you may ask for a

meeting at the following contacts:

Off. Address : RAVI MONGA & CO – COST ACCOUNTANTS

I – 138, MAHAVIR ENCLAVE,

NEW DELHI – 110045

Phone No. : 8285363960

Mail-Id : rmc.cmaindia@gmail.com

cmaravimonga@gmail.com