QNBFS Daily Market Report December 9, 2018

•

0 likes•123 views

The QSE Index rose 0.1% to close at 10,598.4

Recommended

Recommended

More Related Content

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

QNBFS Daily Market Report December 9, 2018

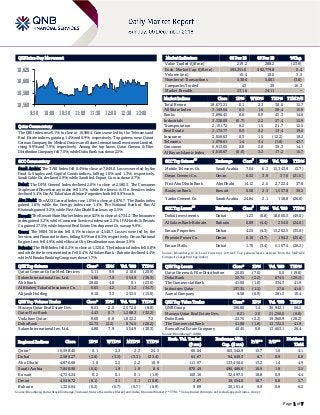

- 1. Page 1 of 7 QSE Intra-Day Movement Qatar Commentary The QSE Index rose 0.1% to close at 10,598.4. Gains were led by the Telecoms and Real Estate indices, gaining 1.4% and 0.9%, respectively. Top gainers were Qatari German Company for Medical Devices and Salam International Investment Limited, rising 9.9% and 7.9%, respectively. Among the top losers, Qatar Cinema & Film Distribution Company fell 7.0%, while Doha Bank was down 2.2%. GCC Commentary Saudi Arabia: The TASI Index fell 0.4% to close at 7,849.0. Losses were led by the Food & Staples and Capital Goods indices, falling 1.6% and 1.3%, respectively. Saudi Cable Co. declined 2.9%, while Saudi Ind. Export Co. was down 2.7%. Dubai: The DFM General Index declined 2.0% to close at 2,580.3. The Consumer Staples and Discretionary index fell 5.5%, while the Invest. & Fin. Services index declined 5.4%. Dar Al Takaful and Union Properties both fell 9.9% each. Abu Dhabi: The ADX General Index rose 1.0% to close at 4,876.7. The Banks index gained 1.8%, while the Energy index rose 1.4%. The National Bank of Ras Al Khaimah gained 3.2%, while First Abu Dhabi Bank was up 2.5%. Kuwait: The Kuwait Main Market Index rose 0.2% to close at 4,734.2. The Insurance index gained 3.2%, while Consumer Services index rose 2.3%. IFA Hotels & Resorts Co. gained 27.5%, while Injazzat Real Estate Development Co. was up 9.0%. Oman: The MSM 30 Index fell 0.1% to close at 4,548.7. Losses were led by the Services and Financial indices, falling 0.5% and 0.3%, respectively. Oman National Engine. Invt. fell 4.9%, while Muscat City Desalination was down 3.9%. Bahrain: The BHB Index fell 0.2% to close at 1,320.0. The Industrial index fell 0.8% and while the Investment index fell 0.4%. Al Salam Bank - Bahrain declined 4.4%, while Al Baraka Banking Group was down 1.7%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Qatari German Co for Med. Devices 5.11 9.9 210.0 (20.9) Salam International Inv. Ltd. 4.80 7.9 554.9 (30.3) Ahli Bank 28.60 4.8 0.1 (23.0) Al Khaleej Takaful Insurance Co. 8.65 4.2 31.2 (34.7) Alijarah Holding 9.10 3.3 253.5 (15.0) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Mazaya Qatar Real Estate Dev. 8.21 2.0 2,572.0 (8.8) Qatar First Bank 4.43 0.7 1,288.3 (32.2) Vodafone Qatar 8.60 0.8 1,032.2 7.2 Doha Bank 22.75 (2.2) 874.5 (20.2) Salam International Inv. Ltd. 4.80 7.9 554.9 (30.3) Market Indicators 06 Dec 18 05 Dec 18 %Chg. Value Traded (QR mn) 219.2 288.2 (23.9) Exch. Market Cap. (QR mn) 595,351.0 592,779.8 0.4 Volume (mn) 10.4 10.0 3.5 Number of Transactions 5,386 5,601 (3.8) Companies Traded 43 39 10.3 Market Breadth 23:16 24:11 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 18,673.21 0.1 2.3 30.6 15.7 All Share Index 3,149.64 0.3 1.6 28.4 15.9 Banks 3,896.45 0.6 0.9 45.3 14.6 Industrials 3,338.09 (0.7) 2.2 27.4 15.9 Transportation 2,151.72 0.2 1.5 21.7 12.5 Real Estate 2,172.77 0.9 2.2 13.4 19.6 Insurance 3,056.63 0.3 1.5 (12.2) 18.2 Telecoms 1,078.61 1.4 3.4 (1.8) 43.7 Consumer 6,913.05 0.0 2.0 39.3 14.1 Al Rayan Islamic Index 4,010.67 (0.0) 3.2 17.2 15.7 GCC Top Gainers ## Exchange Close # 1D% Vol. ‘000 YTD% Mobile Telecom. Co. Saudi Arabia 7.04 6.3 15,343.8 (3.7) Oman Cement Co. Oman 0.32 3.9 37.6 (21.5) First Abu Dhabi Bank Abu Dhabi 14.12 2.5 2,722.4 37.8 Boubyan Bank Kuwait 0.58 2.3 1,537.8 39.2 Yanbu Cement Co. Saudi Arabia 24.84 2.1 158.8 (26.6) GCC Top Losers ## Exchange Close # 1D% Vol. ‘000 YTD% Dubai Investments Dubai 1.23 (6.8) 18,000.3 (49.0) Al Salam Bank-Bahrain Bahrain 0.09 (4.4) 254.0 (24.6) Emaar Properties Dubai 4.25 (4.3) 13,202.5 (35.0) Phoenix Power Co. Oman 0.10 (3.7) 194.3 (25.4) Emaar Malls Dubai 1.70 (3.4) 5,107.4 (20.2) Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the S&P GCC Composite Large Mid Cap Index) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Qatar Cinema & Film Distribution 20.05 (7.0) 0.0 (19.8) Doha Bank 22.75 (2.2) 874.5 (20.2) The Commercial Bank 41.00 (1.8) 334.3 41.9 Industries Qatar 137.35 (1.5) 57.8 41.6 Aamal Company 9.58 (0.9) 281.3 10.4 QSE Top Value Trades Close* 1D% Val. ‘000 YTD% QNB Group 196.80 1.4 30,942.1 56.2 Mazaya Qatar Real Estate Dev. 8.21 2.0 21,250.0 (8.8) Doha Bank 22.75 (2.2) 19,960.9 (20.2) The Commercial Bank 41.00 (1.8) 13,722.5 41.9 Barwa Real Estate Company 40.45 0.8 13,663.1 26.4 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 10,598.40 0.1 2.3 2.3 24.3 60.04 163,542.9 15.7 1.6 4.1 Dubai 2,580.27 (2.0) (3.3) (3.3) (23.4) 64.07 94,649.3 8.7 0.9 6.8 Abu Dhabi 4,876.68 1.0 2.2 2.2 10.9 111.97 133,450.6 13.2 1.4 4.9 Saudi Arabia 7,848.98 (0.4) 1.9 1.9 8.6 870.49 496,486.0 16.9 1.8 3.5 Kuwait 4,734.24 0.2 0.1 0.1 (1.9) 100.16 32,497.5 16.8 0.9 4.4 Oman 4,548.72 (0.1) 3.1 3.1 (10.8) 2.07 19,554.6 10.7 0.8 5.7 Bahrain 1,320.04 (0.2) (0.7) (0.7) (0.9) 9.89 20,101.4 8.9 0.8 6.2 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Market and Dubai Financial Market (** TTM; * Value traded ($ mn) do not include special trades, if any) 10,560 10,580 10,600 10,620 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 7 Qatar Market Commentary The QSE Index rose 0.1% to close at 10,598.4. The Telecoms and Real Estate indices led the gains. The index rose on the back of buying support from non-Qatari shareholders despite selling pressure from Qatari and GCC shareholders. Qatari German Company for Medical Devices and Salam International Investment Limited were the top gainers, rising 9.9% and 7.9%, respectively. Among the top losers, Qatar Cinema & Film Distribution Company fell 7.0%, while Doha Bank was down 2.2%. Volume of shares traded on Thursday rose by 3.5% to 10.4mn from 10mn on Wednesday. Further, as compared to the 30-day moving average of 7.1mn, volume for the day was 45.9% higher. Mazaya Qatar Real Estate Development and Qatar First Bank were the most active stocks, contributing 24.8% and 12.4% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 12/6 US Automatic Data Processing, Inc ADP Employment Change Nov 179k 195k 227k 12/6 US US Census Bureau Trade Balance Oct -$55.5b -$55.0b -$54.0b 12/6 US Markit Markit US Services PMI Nov F 54.7 54.4 54.4 12/6 US Markit Markit US Composite PMI Nov F 54.7 -- 54.4 12/6 US Institute for Supply Manag. ISM Non-Manufacturing Index Nov 60.7 59 60.3 12/6 US US Census Bureau Factory Orders Oct -0.021 -0.02 0.007 12/6 US Bureau of Labor Statistics Unemployment Rate Nov 0.037 0.037 0.037 12/6 US Bureau of Labor Statistics Underemployment Rate Nov 0.076 -- 0.074 12/6 US Deutsche Bundesbank Factory Orders MoM Oct 0.003 -0.004 0.003 12/6 Germany Germany Manufacturing Orders Factory Orders WDA YoY Oct -0.027 -0.031 -0.022 12/6 Germany Markit Germany Cons. PMI Markit Germany Construction PMI Nov 51.3 -- 49.8 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar S&P revises Qatar’s outlook to ‘Stable’ from ‘Negative’, affirms ‘AA-/A-1+’ ratings – S&P Global Ratings announced that it has revised its outlook on Qatar to ‘Stable’ from ‘Negative’. “At the same time, we affirmed our ‘AA-/A-1+’ long-and-short-term sovereign credit ratings. The transfer and convertibility (T&C) assessment is unchanged at ‘AA’,” the rating agency noted in a report. “The Stable outlook primarily reflects our view that Qatar will continue to effectively mitigate the economic and financial fallout of the boycott imposed on the country in June 2017, and that Qatar will continue to pursue prudent macroeconomic policies that support large recurrent fiscal and external surpluses over 2018-2021,” the report stated. (Qatar- Tribune.com) IIF: Qatar’s OPEC exit represents a message that Doha wants to chart its own course – Qatar’s exit from OPEC (Organisation of the Petroleum Exporting Countries) represents a symbolic message that Doha wants to chart its own course, according to an US economic think-tank. "Yet this move does not actually lift constraints on Qatar’s natural gas activities, since OPEC does not regulate natural gas," the Institute of International Finance (IIF) stated in a report. However, the move sends a message that the country remains committed to pursuing an independent path and focusing on a sector where it is already vying for position as the world’s largest producer, rather than remaining in an organization that it sees as irrelevant to its growth plan; Qatar is one of the smaller crude producers in the bloc (0.6mn barrels per day), and its production has been falling for a decade. HE Minister of State for Energy Affairs, Saad bin Sherida Al-Kaabi had announced that Qatar will opt out of the oil grouping from January 1, 2019. Qatar is seeking to cement its position as the world’s largest producer of liquefied natural gas (LNG), given its massive reserves and surging global demand. Following three years of small decline in hydrocarbon production, work is expected to start next year to increase production capacity from 77mn tons to 110mn tons over the next five to seven years. (Gulf-Times.com) IIF: External pressure for a resolve to embargo on Qatar mounting – The external pressure for a resolve to the ongoing embargo on Qatar by Saudi-led quartet has been “mounting”, particularly from the US, as the crisis has damaged the GCC growth initiatives to boost regional trade and infrastructure, Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 31.50% 44.41% (28,287,462.55) Qatari Institutions 11.06% 7.61% 7,562,450.59 Qatari 42.56% 52.02% (20,725,011.96) GCC Individuals 1.53% 0.68% 1,861,938.35 GCC Institutions 2.28% 6.26% (8,744,005.31) GCC 3.81% 6.94% (6,882,066.96) Non-Qatari Individuals 12.64% 14.53% (4,142,368.63) Non-Qatari Institutions 41.00% 26.52% 31,749,447.55 Non-Qatari 53.64% 41.05% 27,607,078.92

- 3. Page 3 of 7 according to the Institute of International Finance (IIF), a Washington-based economic think-tank. “The external pressure for a resolution, particularly from the USA, is mounting, given the cost it has imposed across the GCC,” IIF said, adding the rift has damaged GCC growth initiatives to boost regional trade and infrastructure, and has hindered capital and financial market development. The rift has given the government additional motivation to put into action its long-term commitment to structural reform and diversification even while oil prices remain high, it said. Highlighting that Qatar’s fiscal footing is sound and has displayed strong trade performance despite the embargo; IIF said the country has sufficient fiscal space to continue with gradual fiscal consolidation even if oil prices decline below $60 per barrel. (Gulf-Times.com) Al Kaabi leads Qatar’s delegation to its last OPEC meeting – HE Saad bin Sherida Al Kaabi, the Minister of State for Energy Affairs, led Qatar’s last delegation to the meetings of the Organisation of the Petroleum Exporting Countries (OPEC), in the aftermath of the State of Qatar’s announcement on withdrawing its membership in the organization. The Minister took part in the 175th meeting of the OPEC ministerial conference, which was held in Vienna to discuss a number of developments related to the oil markets and production levels. The meetings also reviewed a number of reports including the report of the Secretary General on oil market outlook, and the report of the 130th meeting of the Economic Commission Board. Al Kaabi also held a series of talks with OPEC oil ministers on the sidelines of the organization’s meetings. (Peninsula Qatar) Qatar’s real estate deal value in October jumps by 33.2% – Qatar’s real estate market witnessed a remarkable double-digit growth in October 2018 compared to the value of transactions in the previous month. The combined value of real estate deals signed during the month touched QR1.74bn, registering a sharp jump of 33.2% compared to QR1.30bn recorded in the previous month (September). When compared on YoY basis, the October transaction value (of QR1.74bn) was down 73.2% against QR6.52bn in the same months last year, due to several big valued transactions signed during the month, latest official statistics showed. According to the November monthly bulletin released by the Ministry of Development Planning and Statistics, there were 332 real estate transactions inked during the month of October against 349 deals in September 2018. The number of total transactions signed in October 2017 stood at 580. (Peninsula Qatar) QNB Group ‘Strategy Conference’ dwells on expansion plans – QNB Group has recently held its ‘Strategy Conference’ in Qatar with the attendance of its executive management, general managers, and CEOs from across the Group’s international network. During the two-day event, the attendees discussed a number of major topics, including the group’s business plans, remarkable performance, and the progress achieved throughout the year. Additionally, the conference also discoursed strategies to be implemented across the group’s international network to increase and sustain growth to achieve its vision of becoming a leading bank in the Middle East, Africa, and South East Asia by 2020. The conference showcased the group’s key strategic priorities, as well as the identification of potential opportunities available for QNB Group across its growing network. (Gulf-Times.com) The Commercial Bank closes $750mn syndicated senior unsecured term loan facility – The Commercial Bank has successfully closed a three-year $750mn syndicated senior unsecured term loan facility. The mandate was led by Bank of America Merrill Lynch and Mizuho Bank as joint coordinators and mandated lead arrangers. The syndication was launched at an initial value of $750mn. The transaction received strong interest from the market and closed significantly oversubscribed at a value of $975mn, demonstrating investor confidence in The Commercial Bank’s financial performance and management, as well the strength of the Qatari economy. Ultimately, the bank decided to close the facility at its original value of $750mn, reflecting its strong liquidity position. The proceeds from the facility paid a margin of 100 basis points over Libor and will be used to replace a pre-existing facility and used for The Commercial Bank’s general funding requirements. (Gulf-Times.com) QAMCO shares to start trading on the QSE from December 16 – Qatar Aluminium Manufacturing Company (QAMCO), whose QR2.73bn initial public offering (IPO) recently concluded with a 2.5 times oversubscription, will start trading on the Qatar Stock Exchange (QSE) from December 16 (Sunday), thus taking the total number of listed entities to 46. The decision to list QAMCO on the QSE is based on the approval of the Qatar Financial Markets Authority after the company has fulfilled all necessary administrative and technical requirements. Highlighting that the QAMCO will be listed within the industrial sector with a symbol QAMC; a QSE spokesman said as usual, price floatation will be permitted only for the first day of listing but from the subsequent days price fluctuation will be 10% up/down as is the case with other listed companies. The industrial sector will thus have 10 constituents. “On the first day of trading, the standard procedures of IPOs will apply. Brokerage companies will be permitted to enter any buy/sell orders for QAMCO shares in the pre-open session at 8:45 am for the listing morning day only,” the spokesman said, adding the pre-opening session for all other listed companies will remain as business usual at 9.00am. (Gulf-Times.com) Amwaj signs QR141mn, five-year contract with Qatargas – Amwaj, a leading Qatari hospitality and facility management service provider and subsidiary of Gulf International Services, has been awarded a QR141mn, five year contract by Qatargas “for the provision of office waiters, cleaning and pest control services.” This project entails the deployment of almost 600 personnel at various Qatargas locations in Ras Laffan, Al Khor and Doha. (Gulf-Times.com) Qatar Petroleum signs exploration deal marking its first entry into Mozambique – Qatar Petroleum entered into an agreement with an ExxonMobil affiliate to acquire a 10% stake in three offshore exploration blocks in the Angoche and Zambezi basins in Mozambique. The consortium will be made up of ExxonMobil (operator) with a 50% participating interest, Empresa Nacional de Hidrocarbonetos (ENH) with a 20% participating interest, Rosneft with a 20% participating interest and Qatar Petroleum with a 10% participating interest. Commenting on this occasion, HE Saad Sherida Al-Kaabi, the Minister of State for

- 4. Page 4 of 7 Energy Affairs, and President & CEO of Qatar Petroleum, said, “We are pleased to sign this agreement, with our long-time partner ExxonMobil to participate in exploring these frontier offshore basins in the Republic of Mozambique. This is a milestone for Qatar Petroleum as it marks its first foray into Mozambique’s promising offshore basins”. (Peninsula Qatar) Qatar’s Itlaq and Oman’s Tsaheel sign MoU - The second edition of ‘Made in Qatar’ exhibition to be held outside the country, witnessed the signing of a MoU between the Doha- based Itlaq Business Management Company (Itlaq) and the Omani Center for Businessmen Services (Tsaheel) in Muscat. The agreement was signed by the CEO of Itlq Dr Latifa Ali Al Darwish and Tsaheel’s CEO Mohamed Fadl Al Baloushi, on the sidelines of the four-day expo. The cooperation agreement aims to help both sides’ companies willing to set up SMEs in Qatar and Oman. (Peninsula Qatar) Ooredoo announces date to pay interest to bondholders – Ooredoo announced that Ooredoo International Finance Limited (OIFL), its wholly-owned subsidiary, pursuant to the Terms and Conditions of the Notes and the Final Terms. It will pay Note-holders $23,625,000.00 on the interest payment date falling due on December 10, 2018, and will pay Note-holders $9,375,000.00 on the interest payment date falling due on December 24, 2018. (QSE) International G20 ‘ever more important’ for global economic governance, says QNB Group – As large emerging market (EM) economies catch up and continue to grow faster than major advanced economies, the G20 dynamics evolve, making it an ever more important arrangement for global economic governance, QNB Group has said in an economic commentary. The recent detente in bilateral trade between the US and China, agreed last week during the G20 Summit in Buenos Aires, is just the latest expression of both the new dynamics and overall importance of the forum. “The G20 has indeed gone a long way from its origins in the late 1990s and is set to become even more central as global economic convergence takes place. Our analysis focuses on the underlying economic factors behind the G20 growing influence,” QNB Group stated. The G20 is an international forum for the governments and central bank governors of some of the largest economies in the world, deemed of systemic significance for the international financial system. Membership includes 19 countries and one bloc, the European Union, represented by the European Commission and the European Central Bank. Member countries are comprised of the traditional G7 countries (Canada, France, Germany, Italy, Japan, the UK, and the US), Brics countries (Brazil, Russia, India, China, and South Africa), MIST countries (Mexico, Indonesia, South Korea, and Turkey), Argentina, Australia as well as Saudi Arabia. (Gulf-Times.com) US job growth slows in November; monthly wage gains modest – US job growth slowed in November and monthly wages increased less than forecast, suggesting some moderation in economic activity that could support expectations of fewer interest rate increases from the Federal Reserve in 2019. The slowdown in hiring reported by the Labor Department is likely the result of worker shortages. The Fed in its “Beige Book” report this week stated most business contacts in its 12 districts said “that employment growth leaned to the slower side of a modest to moderate pace” because of labor shortages. The labor market is considered near or at full employment. Non-farm payrolls increased by 155,000 jobs last month, with construction companies hiring the fewest workers in eight months, likely because of unseasonably chilly temperatures. The moderation in job gains in November also fits in with other data showing a rise in layoffs in recent weeks and a decline in a measure of services sector employment last month. Data for September and October were revised to show 12,000 fewer jobs added than previously reported. Economists polled by Reuters had forecast payrolls increasing by 200,000 jobs in November. The unemployment rate was unchanged at near a 49-year low of 3.7% as 133,000 people entered the labor force. Average hourly earnings rose six cents or 0.2% in November. October wage gains were revised down to 0.1% from the previously reported 0.2%. In the 12 months through November, wages increased 3.1%, matching October’s jump, which was the biggest gain since April 2009. (Reuters) US trade deficit hits 10-year high; job growth slowing – The US trade deficit jumped to a 10-year high in October as soybean exports dropped further and imports of consumer goods rose to a record high, suggesting the Trump administration’s tariff- related measures to shrink the trade gap likely have been ineffective. Other data showed private employers hired fewer workers than expected in November, pointing to a moderation in the pace of job growth. That was reinforced by another report showing a small decline in the number of Americans filing claims for unemployment benefits last week. The reports added to weak housing and business spending on equipment data in signaling a slowdown in economic growth. Concerns over the health of the economy have roiled financial markets in recent days. The Commerce Department stated the trade deficit increased 1.7% to $55.5bn, the highest level since October 2008. The trade gap has now widened for five straight months. Data for September was revised to show the deficit rising to $54.6bn instead of the previously reported $54.0bn. (Reuters) US factory orders post largest drop in more than a year – New orders for US-made goods recorded their biggest drop in more than a year in October and business spending on equipment appeared to be softening, suggesting a slowdown in activity in the manufacturing sector. Factory goods orders fell 2.1% amid a decline in demand for a range of goods, the Commerce Department stated. That was the largest decrease in orders since July 2017. Data for September was revised lower to show factory orders rising only 0.2% instead of the previously reported 0.7% increase. Economists polled by Reuters had forecast factory orders declining 2.0% in October. Orders increased 8.3% on a YoY basis in October. An Institute for Supply Management survey of manufacturers published showed an improvement in business conditions in November. Manufacturers across nearly all industries, however, complained that worker shortages and the Trump administration’s import tariffs were disrupting operations. (Reuters) Eurostat confirms Eurozone GDP, employment growth slows in third quarter – The Eurozone economy grew at its slowest pace in four years in the third quarter of 2018, while employment

- 5. Page 5 of 7 growth also eased during the period, data released by the European Union statistics agency showed, confirming earlier estimates. Eurozone GDP rose by 0.2% in the July-September period, Eurostat reported, confirming its earlier preliminary estimates. This was the slowest rate of economic growth since the second quarter of 2014 and a marked slowdown from 0.4% growth in the second quarter. On the year, the GDP growth rate in the 19-country currency bloc was 1.6%, Eurostat said, revising down its earlier estimate of a 1.7% expansion. The economy of Germany, the Eurozone’s largest, contracted by 0.2% on the quarter, France’s was 0.4% stronger, while Italy’s GDP shrunk by 0.1%. In a separate release on Friday, Eurostat confirmed its previous estimates on employment growth in the Eurozone. The number of people employed in the Eurozone increased by 0.2% QoQ and by 1.3% YoY, compared with rates of 0.4% and 1.5% respectively in the second quarter. (Reuters) German industry output falls unexpectedly in October – German industrial output fell unexpectedly in October, data showed, adding to signs that a cooling trend in Europe’s largest economy will continue in the fourth quarter. Data from the Statistics Office showed industrial output fell by 0.5%, confounding a Reuters forecast for an increase of 0.3%. The figure for September was revised down to a rise of 0.1% from a previously reported increase of 0.2%. A breakdown of the data showed that activity in the manufacturing, energy and construction sectors had contracted. (Reuters) Japan firms see trade war, sales tax pressuring economy in 2019 – Most Japanese firms expect flat or weaker domestic growth next year and are even more pessimistic about global growth amid concerns over the impact of the US-China trade war and a planned sales tax hike at home, a Reuters poll showed. Japan’s export-driven economy, which hit a rough patch in the most recent quarter, has generally been chugging along. And Tokyo stocks are set to notch a seventh straight year of gains since Prime Minister Shinzo Abe came to office in late 2012. But in a sign that growth may be leveling off, the Reuters Corporate Survey found 55% of companies predicted that Japan’s economic growth would remain about the same as this year’s 1% projection, while 31% see it slowing. Only 14% believe it will accelerate. The Sino-US trade war and a planned sales tax increase in October to 10% from 8% currently were considered two major risks to their growth outlook. Others saw Japan-US trade negotiations, capital flight in emerging markets and geopolitical issues in the Middle East, as risks to growth. (Reuters) China's November export, import growth shrinks, showing weak demand – China reported far weaker than expected November exports and imports, showing slower global and domestic demand and raising the possibility authorities will take more measures to keep the country’s growth rate from slipping too much. November exports only rose 5.4% from a year earlier, Chinese customs data showed, the weakest performance since a 3% contraction in March, and well short of the 10% forecast in a Reuters poll. Analysts say the export data showed that the “front-loading” impact as firms rushed out shipments to beat planned US tariff hikes faded, and that export growth is likely to slow further as demand cools. The customs data showed that annual growth for exports to all of China’s major partners slowed significantly. Exports to the US rose 9.8% in November from a year earlier, compared with 13.2% in October. (Reuters) Regional OPEC, Russia agree to slash oil output despite Trump pressure – OPEC and its Russia-led allies agreed to slash oil production by more than the market had expected despite pressure from US President Donald Trump to reduce the price of crude. The producer club will curb output from January by 0.8mn bpd versus October levels while non-OPEC allies contribute an additional 0.4mn bpd of cuts, in a move to be reviewed at a meeting in April. Oil prices jumped about 5% to more than $63 a barrel as the combined cut of 1.2mn bpd was larger than the minimum 1mn bpd that the market had expected. Saudi Arabia has faced demands from Donald Trump to help the global economy by refraining from paring supplies. An output curtailment also would provide support to Iran by increasing the price of oil amid attempts by Washington to squeeze the economy of OPEC’s third-largest producer. (Reuters) OPEC yet to agree final deal as Iran seeks exemptions – Iran appears to be the main obstacle for an OPEC oil output deal as the group’s leader Saudi Arabia is yet to agree exemptions for sanctions-hit Tehran, OPEC sources said. On December 6, OPEC failed to agree concrete parameters for a deal to restrict output. (Reuters) GCC fiscal reforms seen progressing at a measured pace in 2019 – Fiscal reforms are expected to progress at a ‘measured’ pace in the Gulf Co-operation Council (GCC) in 2019, having slowed this year, according to Fitch, an international rating agency. The recovery of oil prices has lessened some of the pressure, and socio-political considerations will continue to weigh on implementation of the reforms, the rating agency stated in a report. “Given our forecast for lower oil prices, we expect that fiscal authorities will need to continue efforts to introduce or boost taxation and to enact other measures such as public- sector pay reforms,’ it suggested. (Gulf-Times.com) Fitch forecasts ‘Stable’ outlook for GCC Islamic banks in 2019 – Stronger economic growth, led by higher oil prices, and its expected contribution to credit fundamentals have encouraged Fitch, a global credit rating agency, to forecast a ‘Stable’ outlook for the Gulf Cooperation Council (GCC) Islamic banks in 2019. “Credit growth will remain weak at about 5% – still above financing growth at conventional banks – and will increase from 2018 levels in most countries,” Fitch stated, expecting liquidity to remain strong. “We expect capital levels to remain mostly unchanged in 2019. Earnings will remain high, benefiting from increasing interest rates in most countries,” it added. (Gulf-times.com) IATA: Middle East carriers see 4.4% demand rise in Oct – Middle East carriers experienced a 4.4% rise in demand in October compared to last year, International Air Transport Association (IATA) stated in its passenger traffic data for October. Although lowest among the regions for the seventh time in the last one year, it was, however seen an increase over the 3.3% increase in September. The capacity of the region’s carriers increased 6.4%, and load factor slid 1.3 percentage points to 69.8%, lowest among regions. “Carriers have been buffeted by policy measures and geopolitical tensions in recent years,

- 6. Page 6 of 7 including the ban on portable electronic devices and travel restrictions. However, volatile passenger volumes are trending up solidly in seasonally-adjusted terms,” IATA noted. (Gulf- Times.com) Saudi Arabia’s Saad Group and creditors select advisors in bid to resolve debt dispute – Saad Group and bank creditors of the Saudi Arabian conglomerate have both selected advisors in a bid to try to reach a deal that could help end the Kingdom’s largest and longest running debt dispute, financial sources said. The appointments of the London-based Orchard Corporate Strategy by Saad and Ernst & Young (EY) by creditors, is the latest attempt to reach an agreement that will be complicated by an ongoing auction of the company’s assets. Creditors were seeking to engage with the court overseeing an auction process to try to avoid a fire sale of assets and disorderly liquidation of the company in order to secure a better deal for creditors, sources said. (Gulf-Times.com) Saudi Arabia November Whole Economy PMI 55.2 vs 53.8 in October – In a release by Emirates NBD and IHS Markit, the purchasing managers’ index (PMI) for Saudi Arabia’s whole economy rose to 55.2 in November 2018 from 53.8 in October 2018 and 57.5 in November 2017. This is the highest reading since December 2017. (Bloomberg) Saudi Arabia eyes lower duties to boost exports – Saudi Arabia is looking at reducing customs duties on value added products to boost exports, Al-Eqtisadiah reported, citing Fahad Al-Skeet, head of the local content and private sector development unit Namaa. The discussions are underway between the unit and exports development authority. The initiatives to boost Saudi Arabia’s exports are expected to be launched by the end of the year. (Bloomberg) Saudi Arabia’s oil exports at 7.7mn bpd in December – Saudi Arabia’s oil exports may be around 7.7mn bpd in December, down from 8.3mn bpd in November, the Kingdom’s Oil Minister Khalid Al-Falih said. The Kingdom proposed a moderate oil- production cut from OPEC and its allies; “We in the kingdom are going to be advocating something adequate to balance the market,” Al-Falih said. Saudi Arabia’s November oil output was 11.1mn bpd and the supply to the market was 11.3mn bpd, he said. (Bloomberg) Saudi Arabia’s oil premium drops to 15-year low as fuel profits crash – Saudi Arabia’s crude pricing in the world’s biggest oil market is reflecting tumbling profits from making cleaner fuels in Asia. State-run Saudi Aramco slashed the premium of its Extra Light grade to its Heavy crude to the lowest since 2003, data compiled by Bloomberg showed. When lighter varieties of oil are refined, they typically yield more of relatively clean products such as gasoline and petrochemical ingredient naphtha. The market for such fuels has been mired in a glut over the past two months. While the world’s biggest oil exporter cut pricing on all its grades for January sales to Asia in a bid to take back market share lost to the likes of Russia and the US, the significant reduction in the premium for its lighter varieties shows that the Kingdom is probably taking into account the shrinking margins in the region for cleaner fuels as well as focusing on tackling competition from other sellers. (Gulf-Times.com) UAE November Whole Economy PMI 55.8 vs 55 in October – In a release by Emirates NBD and IHS Markit, the purchasing managers’ index (PMI) for UAE’s whole economy rose to 55.8 in November 2018 from 55 in October 2018 and 57 in November 2017. This is the highest reading since July 2018. (Bloomberg) Abu Dhabi meets bond investors in non-deal roadshow – Abu Dhabi held meetings with international bond investors in a so- called non-deal roadshow before a potential bond issue next year, sources said, as a recent drop in oil prices might prompt Gulf countries to borrow soon. Governments in the GCC region have raised billions of Dollars in the international debt markets over the past few years to offset budget deficits caused by lower oil prices. Representatives of the Abu Dhabi government met investors in Frankfurt, London, Boston and New York about a week ago, sources said. Abu Dhabi, which raised $10bn last year in bonds, has been in talks with investors at various stages this year, banking sources previously said, but a rise in oil prices meant that the Emirate felt no urgency to borrow. (Reuters) Kuwait to be added to S&P Dow Jones Indices’ Global Benchmark Indices with EM classification – Kuwait’s stock market will be added to S&P Dow Jones Indices’ Global Benchmark Indices with an emerging market classification, Kuwait’s market regulator stated citing the index provider. This comes ahead of MSCI’s decision next year on whether to reclassify its Kuwait index from the current frontier-market status to its widely used emerging-market benchmark. In a statement, cited by the Capital Markets Authority, S&P DJI stated that it has recognized the progress Kuwait had made in trade clearing and settlement, including changing to a T+3 settlement cycle, meaning trades are settled within three days of execution, and establishing a delivery versus payment system. It stated that the move will be effective before the market opens on September 23, 2019. (Reuters) Kuwait cancels Wataniya Airways operating license – Kuwait’s aviation regulator has canceled Wataniya Airways operating license after the carrier failed to improve its business following a series of flight disruptions, Al-Jarida newspaper reported. The license was suspended in September for three months to revamp the business, a spokesman for Kuwait’s Directorate General of Civil Aviation told Al-Jarida. (Bloomberg)

- 7. Contacts Saugata Sarkar, CFA, CAIA Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa QNB Financial Services Co. W.L.L. Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. W.L.L. (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (Q.P.S.C.). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange. Qatar National Bank (Q.P.S.C.) is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns) 45.0 70.0 95.0 120.0 Nov-14 Nov-15 Nov-16 Nov-17 Nov-18 QSEIndex S&P Pan Arab S&P GCC (0.4%) 0.1% 0.2% (0.2%) (0.1%) 1.0% (2.0%)(2.5%) (1.5%) (0.5%) 0.5% 1.5% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,248.35 0.9 2.1 (4.2) MSCI World Index 1,965.24 (1.3) (3.7) (6.6) Silver/Ounce 14.62 1.0 3.0 (13.7) DJ Industrial 24,388.95 (2.2) (4.5) (1.3) Crude Oil (Brent)/Barrel (FM Future) 61.67 2.7 5.0 (7.8) S&P 500 2,633.08 (2.3) (4.6) (1.5) Crude Oil (WTI)/Barrel (FM Future) 52.61 2.2 3.3 (12.9) NASDAQ 100 6,969.25 (3.0) (4.9) 1.0 Natural Gas (Henry Hub)/MMBtu 4.51 1.6 (2.2) 27.4 STOXX 600 345.45 0.7 (2.7) (15.9) LPG Propane (Arab Gulf)/Ton 73.50 3.2 7.3 (24.8) DAX 10,788.09 (0.1) (3.5) (20.8) LPG Butane (Arab Gulf)/Ton 74.25 3.5 14.7 (29.7) FTSE 100 6,778.11 0.6 (3.1) (17.0) Euro 1.14 0.0 0.5 (5.2) CAC 40 4,813.13 0.8 (3.1) (14.1) Yen 112.69 0.0 (0.8) 0.0 Nikkei 21,678.68 0.7 (2.2) (4.9) GBP 1.27 (0.4) (0.2) (5.8) MSCI EM 981.37 0.2 (1.3) (15.3) CHF 1.01 0.2 0.7 (1.7) SHANGHAI SE Composite 2,605.89 0.1 1.9 (25.4) AUD 0.72 (0.4) (1.3) (7.7) HANG SENG 26,063.76 (0.4) (1.5) (12.9) USD Index 96.51 (0.3) (0.8) 4.8 BSE SENSEX 35,673.25 0.0 (3.6) (6.2) RUB 66.40 (0.7) (0.9) 15.2 Bovespa 88,115.07 (0.5) (1.8) (1.7) BRL 0.26 (0.7) (1.0) (15.2) RTS 1,157.94 2.1 2.8 0.3 83.3 79.6 78.5