QSE Rises 1.8% on Gains in Industrials and Banks

•

0 likes•174 views

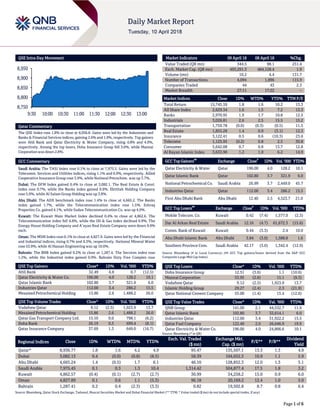

The QSE Index rose 1.8% led by gains in the Industrials and Banks & Financial Services indices. Ahli Bank and Qatar Electricity & Water Company were the top gainers rising 4.8% and 4.0% respectively, while Doha Insurance Group fell 3.6%. Trading activity on the QSE rose significantly compared to the previous day, with value traded up 251.4% and volume up 131.7%.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to QSE Rises 1.8% on Gains in Industrials and Banks

Similar to QSE Rises 1.8% on Gains in Industrials and Banks (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

QSE Rises 1.8% on Gains in Industrials and Banks

- 1. Page 1 of 6 QSE Intra-Day Movement Qatar Commentary The QSE Index rose 1.8% to close at 8,936.8. Gains were led by the Industrials and Banks & Financial Services indices, gaining 2.6% and 1.9%, respectively. Top gainers were Ahli Bank and Qatar Electricity & Water Company, rising 4.8% and 4.0%, respectively. Among the top losers, Doha Insurance Group fell 3.6%, while Mannai Corporation was down 2.8%. GCC Commentary Saudi Arabia: The TASI Index rose 0.1% to close at 7,975.5. Gains were led by the Telecomm. Services and Utilities indices, rising 1.1% and 0.9%, respectively. Allied Cooperative Insurance Group rose 3.9%, while National Petrochem. was up 3.7%. Dubai: The DFM Index gained 0.4% to close at 3,082.1. The Real Estate & Const. index rose 0.7%, while the Banks index gained 0.6%. Ekttitab Holding Company rose 5.0%, while Al Salam Group Holding was up 3.8%. Abu Dhabi: The ADX benchmark index rose 1.4% to close at 4,665.2. The Banks index gained 1.7%, while the Telecommunication index rose 1.5%. Eshraq Properties Co. gained 4.1%, while Sudan Telecommunication Co. was up 4.0%. Kuwait: The Kuwait Main Market Index declined 0.4% to close at 4,862.6. The Telecommunication index fell 4.8%, while the Oil & Gas index declined 0.9%. The Energy House Holding Company and A’ayan Real Estate Company were down 9.9% each. Oman: The MSM Index rose 0.1% to close at 4,827.9. Gains were led by the Financial and Industrial indices, rising 0.7% and 0.3%, respectively. National Mineral Water rose 53.9%, while Al Hassan Engineering was up 10.0%. Bahrain: The BHB Index gained 0.2% to close at 1,287.4. The Services index rose 1.2%, while the Industrial index gained 0.9%. Bahrain Duty Free Complex rose 7.0%, while Seef Properties was up 2.9%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Ahli Bank 32.49 4.8 0.7 (12.5) Qatar Electricity & Water Co. 196.00 4.0 128.2 10.1 Qatar Islamic Bank 102.80 3.7 321.9 6.0 Industries Qatar 112.00 3.4 286.2 15.5 Mesaieed Petrochemical Holding 15.86 2.6 1,488.2 26.0 QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Vodafone Qatar 9.12 (2.5) 1,923.9 13.7 Mesaieed Petrochemical Holding 15.86 2.6 1,488.2 26.0 Qatar Gas Transport Company Ltd. 15.10 0.0 798.1 (6.2) Doha Bank 26.19 0.3 699.4 (8.1) Qatar Insurance Company 37.69 1.3 649.0 (16.7) Market Indicators 09 April 18 08 April 18 %Chg. Value Traded (QR mn) 344.5 98.1 251.4 Exch. Market Cap. (QR mn) 493,291.3 484,128.4 1.9 Volume (mn) 10.2 4.4 131.7 Number of Transactions 4,094 1,896 115.9 Companies Traded 44 43 2.3 Market Breadth 27:11 17:22 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 15,745.59 1.8 1.6 10.2 13.3 All Share Index 2,629.34 1.6 1.5 7.2 13.3 Banks 2,970.95 1.9 1.7 10.8 12.5 Industrials 3,026.81 2.6 2.5 15.5 15.2 Transportation 1,759.78 (0.0) (0.3) (0.5) 11.5 Real Estate 1,855.28 1.4 0.9 (3.1) 12.3 Insurance 3,122.41 0.5 0.6 (10.3) 23.6 Telecoms 1,125.95 (0.2) 0.8 2.5 30.8 Consumer 5,642.08 0.7 0.8 13.7 12.8 Al Rayan Islamic Index 3,633.90 1.2 1.0 6.2 14.9 GCC Top Gainers ## Exchange Close # 1D% Vol. ‘000 YTD% Qatar Electricity & Water Qatar 196.00 4.0 128.2 10.1 Qatar Islamic Bank Qatar 102.80 3.7 321.9 6.0 National Petrochemical Co. Saudi Arabia 26.99 3.7 2,449.0 45.7 Industries Qatar Qatar 112.00 3.4 286.2 15.5 First Abu Dhabi Bank Abu Dhabi 12.40 2.5 4,523.7 21.0 GCC Top Losers ## Exchange Close # 1D% Vol. ‘000 YTD% Mobile Telecom. Co. Kuwait 0.42 (7.4) 1,577.0 (2.3) Dar Al Arkan Real Estate Saudi Arabia 12.16 (4.7) 61,672.3 (15.6) Comm. Bank of Kuwait Kuwait 0.44 (3.3) 2.4 10.0 Abu Dhabi Islamic Bank Abu Dhabi 3.84 (3.0) 1,588.8 1.6 Southern Province Cem. Saudi Arabia 42.17 (3.0) 1,342.4 (12.9) Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the S&P GCC Composite Large Mid Cap Index) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Doha Insurance Group 12.51 (3.6) 1.1 (10.6) Mannai Corporation 53.95 (2.8) 15.1 (9.3) Vodafone Qatar 9.12 (2.5) 1,923.9 13.7 Islamic Holding Group 29.27 (2.4) 2.3 (21.9) Qatar National Cement Company 55.00 (1.4) 15.4 (12.6) QSE Top Value Trades Close* 1D% Val. ‘000 YTD% QNB Group 141.00 2.1 44,532.7 11.9 Qatar Islamic Bank 102.80 3.7 32,614.1 6.0 Industries Qatar 112.00 3.4 31,922.2 15.5 Qatar Fuel Company 122.40 2.0 26,646.9 19.9 Qatar Electricity & Water Co. 196.00 4.0 24,866.6 10.1 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 8,936.77 1.8 1.6 4.2 4.9 95.47 135,507.1 13.3 1.3 4.9 Dubai 3,082.13 0.4 (0.0) (0.8) (8.5) 58.39 104,652.3 10.9 1.1 5.9 Abu Dhabi 4,665.24 1.4 (0.5) 1.7 6.1 46.10 128,852.3 12.0 1.3 5.1 Saudi Arabia 7,975.45 0.1 0.3 1.3 10.4 1,314.42 504,877.4 17.5 1.8 3.2 Kuwait 4,862.57 (0.4) (0.1) (2.7) (2.7) 30.99 34,258.2 15.0 0.9 6.0 Oman 4,827.89 0.1 0.6 1.1 (5.3) 96.18 20,169.2 12.4 1.0 5.0 Bahrain 1,287.41 0.2 0.4 (2.3) (3.3) 0.82 19,502.8 8.7 0.8 6.4 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Market and Dubai Financial Market (** TTM; * Value traded ($ mn) do not include special trades, if any) 8,750 8,800 8,850 8,900 8,950 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 6 Qatar Market Commentary The QSE Index rose 1.8% to close at 8,936.8. The Industrials and Banks & Financial Services indices led the gains. The index rose on the back of buying support from GCC and non-Qatari shareholders despite selling pressure from Qatari shareholders. Ahli Bank and Qatar Electricity & Water Company were the top gainers, rising 4.8% and 4.0%, respectively. Among the top losers, Doha Insurance Group fell 3.6%, while Mannai Corporation was down 2.8%. Volume of shares traded on Monday rose by 131.7% to 10.2mn from 4.4mn on Sunday. However, as compared to the 30-day moving average of 12.3mn, volume for the day was 17.1% lower. Vodafone Qatar and Mesaieed Petrochemical Holding Company were the most active stocks, contributing 18.9% and 14.6% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Earnings Releases, Global Economic Data and Earnings Calendar Earnings Releases Company Market Currency Revenue (mn) 1Q2018 % Change YoY Operating Profit (mn) 1Q2018 % Change YoY Net Profit (mn) 1Q2018 % Change YoY Almarai Company Saudi Arabia SR – – 481.0 14.3% 344.0 4.9% Hotels Management Co. Int. Oman OMR 4.3 15.7% – – 1.6 32.9% Packaging Co. Ltd.# Oman OMR 2,474.8 8.4% – – 46.4 -86.4% Al Anwar Ceramic Tiles Oman OMR 5.5 -4.0% – – 0.4 -32.9% Source: Company data, DFM, ADX, MSM, TASI, BHB. ( # Values in ‘000) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 04/09 Germany German Federal Statistical Office Trade Balance February 18.4bn 20.1bn 17.3bn 04/09 Germany German Federal Statistical Office Current Account Balance February 20.7bn 22.9bn 20.3bn 04/09 Japan Economic and Social Research Institute Consumer Confidence Index March 44.3 44.5 44.3 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Earnings Calendar Tickers Company Name Date of reporting 1Q2018 results No. of days remaining Status QNBK QNB Group 10-Apr-18 0 Due NLCS Alijarah Holding 12-Apr-18 2 Due QIIK Qatar International Islamic Bank 15-Apr-18 5 Due QIBK Qatar Islamic Bank 15-Apr-18 5 Due QISI Qatar Islamic Insurance Company 16-Apr-18 6 Due MCGS Medicare Group 16-Apr-18 6 Due GWCS Gulf Warehousing Company 16-Apr-18 6 Due MARK Masraf Al Rayan 16-Apr-18 6 Due CBQK The Commercial Bank 17-Apr-18 7 Due QNCD Qatar National Cement Company 18-Apr-18 8 Due QEWS Qatar Electricity & Water Company 18-Apr-18 8 Due DOHI Doha Insurance Group 18-Apr-18 8 Due KCBK Al Khalij Commercial Bank 19-Apr-18 9 Due ABQK Ahli Bank 19-Apr-18 9 Due DHBK Doha Bank 22-Apr-18 12 Due SIIS Salam International Investment Limited 23-Apr-18 13 Due QATI Qatar Insurance Company 24-Apr-18 14 Due QGTS Qatar Gas Transport Company Limited (Nakilat) 24-Apr-18 14 Due QGRI Qatar General Insurance & Reinsurance Company 25-Apr-18 15 Due QIMD Qatar Industrial Manufacturing Company 25-Apr-18 15 Due ORDS Ooredoo 25-Apr-18 15 Due Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 32.18% 45.69% (46,569,505.08) Qatari Institutions 28.40% 26.32% 7,158,267.31 Qatari 60.58% 72.01% (39,411,237.77) GCC Individuals 0.44% 0.64% (693,478.02) GCC Institutions 5.70% 1.99% 12,787,450.10 GCC 6.14% 2.63% 12,093,972.08 Non-Qatari Individuals 6.88% 8.00% (3,866,077.66) Non-Qatari Institutions 26.41% 17.36% 31,183,343.35 Non-Qatari 33.29% 25.36% 27,317,265.69

- 3. Page 3 of 6 UDCD United Development Company 29-Apr-18 19 Due MERS Al Meera Consumer Goods Company 29-Apr-18 19 Due QOIS Qatar Oman Investment Company 29-Apr-18 19 Due AKHI Al Khaleej Takaful Insurance Company 29-Apr-18 19 Due QFLS Qatar Fuel Company 29-Apr-18 19 Due Source: QSE News Qatar Aamal Medical signs agreement with Turkish healthcare firm to supply medical equipment – Aamal Medical, a fully owned subsidiary of Aamal Company, signed an agreement with Simeks Medical, the Turkish healthcare company to supply medical equipment with advanced medical technologies. (QSE) QIIK to disclose its 1Q2018 financial results on April 15 – Qatar International Islamic Bank (QIIK) announced its intention to disclose its 1Q2018 financial results on April 15, 2018. (QSE) QATI to disclose its 1Q2018 financial results on April 24 – Qatar Insurance Company (QATI) announced its intention to disclose its 1Q2018 financial results on April 24, 2018. (QSE) UDCD postpones its disclosure date of 1Q2018 financial results to April 29 – United Development Company (UDCD) announced the postponement of its intent to disclose its 1Q2018 financial results to April 29, 2018 from April 25, 2018. (QSE) Fitch affirms Doha Bank’s long-term issuer default rating at ‘A’ – Global credit rating agency, Fitch affirmed Doha Bank’s long- term issuer default rating (IDR) at ‘A’. The bank’s IDRs, support rating (SR) and support rating floor (SRF) reflect Fitch’s expectation of an extremely high probability of support from the Qatari authorities for domestic banks in case of need. This reflects Qatar’s strong ability to support its banks, as indicated by its rating, combined with Fitch’s belief that there would be a strong willingness to do so. The latter is based on a strong track record of sovereign support to the banking sector as the government owns stakes in all Qatari banks. According to Fitch, Doha Bank’s ‘bb+’ VR continues to benefit from an established domestic franchise in Qatar, where it is the fifth largest bank with market shares of about 6%-7% in loans and deposits at end-2017. (Gulf-Times.com) Turkey’s Metcap, Qatar’s Fusion Dynamics to invest $5.2bn in Turkey – Turkey’s Metcap Energy Investments (Metcap) and Qatar’s Fusion Dynamics will invest a total of $5.2bn in Turkey. The 50%-50% held joint venture, Metcap Petrochemicals, will build and operate $4bn natural gas-based chemical facility in the Thrace region. The venture will also invest $1.2bn in natural gas power stations in the northwestern Kirklareli province and central Karaman province. Turkey’s President Recep Tayyip Erdogan announced a series of incentives for 23 projects in petrochemicals, pharmaceuticals, agriculture and health, valued at $32bn. It’s the government’s latest move to spur growth and employment. The joint venture shows that the private sector and the market have confidence in Qatar and faith in the Turkish market as well, Fusion Dynamics’ Chairman, Mohammed Awajan Al Hajri said. Moreover, Turkish Grand National Assembly passed a bill to ratify the maritime transport agreement with Qatar, signed December 2, 2015. (Gulf-Times.com, Bloomberg) Growth in exports from India to Qatar estimated at more than 50% in 2017 – There has been a substantial growth in exports from India to Qatar since the economic blockade on this country more than ten months ago, according to Indian Ambassador to Qatar, P Kumaran. The envoy said the growth in exports from India to Qatar is believed to be more than 50% in the last one year. However, it is too early to say if the growth in exports is owing to the movement of the vessels carrying goods directly to Qatar, which used to call on another major port of the region. The concerned section at the embassy is evaluating the data and the final figures would be available shortly. The Ambassador said India has been the third largest trade partner of Qatar, with the bilateral trade exceeding $9bn last year and in the wake of the developments since June 5, 2017, there has been a steady growth in the imports from India, especially of such goods as foodstuffs and construction materials. (Gulf- Times.com) Qatar, India seeks to boost direct shipment capacity – Qatar and India are seeking to enhance the frequency of the current direct shipment as part of efforts to strengthen the economic and business relations between the two countries. “To increase the frequency of the current direct shipment capacity, an exclusive session will be held on ‘Doing Business in Qatar’ from a logistics point of view, addressing relevant issues related to this subject,” said K M Varghese, President of the India Business and Professionals Council (IBPC), which is organizing the first Qatar India Business and Investment Conference (QIBIC) next week. Qatar and India are working on finding new direct shipping routes between the two historically friendly counties. Ten days after the blockade, the Ministry of Transport and Communications launched a new direct maritime line between Qatar and India, India Qatar Express Service, linking Hamad Port with Mundra and Nhava Sheva Port. (Gulf-Times.com) Czech Republic offers promising opportunities to Qatari businessmen – Czech Republic offered promising investment opportunities to attract Qatari businessmen, requiring further cooperation between both the countries’ private sector, according to Qatar Chamber’s Vice Chairman, Mohamed Bin Towar Al Kuwari. Trade relations between Qatar and Czech Republic have been growing rapidly in the past few years, adding that the Central European country is keen to review its ties with Qatar. Last year, trade volume between the two countries stood at $187mn compared to $102mn recorded in 2013. Al Kuwari pointed out that the growth in trade volume encourages businessmen from both the countries to look for profitable investment opportunities and establish trade alliances and joint ventures. (Gulf-Times.com) International UK’s consumer spending wilts in March under heavy snow – British consumer spending wilted under heavy snow in March,

- 4. Page 4 of 6 according to surveys that added to signs the economy probably slowed at the start of 2018. Barclaycard, the credit and debit card division of Barclays, stated annual consumer spending growth slowed to 2.0% in March from 3.8% in February, marking the weakest increase since April 2016. Business surveys last week showed the dominant services sector and the construction industries were hit badly by the poor weather, although manufacturers fared better. Separately, the British Retail Consortium (BRC) stated total retail sales values were up 2.3% in March compared with the same month a year ago, following 1.6% YoY increase in February. The growth reflected the fact that the Easter holiday sales took place in March this year rather than April like in 2017. Retail sales values on a like- for-like basis, which strips out changes in floor space, rose 1.4% in March after 0.6% rise in February. (Reuters) German exports post biggest drop since 2015 – German exports plunged unexpectedly in February, posting their biggest monthly drop in two and half years and narrowing the trade surplus, data showed, in a further sign that growth in Europe’s biggest economy could have reached its peak. Seasonally adjusted exports fell by 3.2% on the month, the steepest drop since August 2015, data from the Federal Statistics Office showed. Imports dropped by 1.3%. A Reuters poll had pointed to exports edging up by 0.2% on the month and imports rising by 0.3%. The seasonally adjusted trade surplus narrowed to 19.2bn Euros from 21.5bn Euros in January. The February reading compared with the Reuters consensus forecast of 21.4bn Euros and marked the lowest surplus since January 2017. Germany’s wider current account surplus, which measures the flow of goods, services and investments, edged up to 20.7bn Euros from 20.3bn Euros in January, unadjusted data showed. (Reuters) Moody’s revises Brazil outlook to ‘Stable’, citing spending cuts – Ratings agency Moody’s Investors Service (Moody’s) revised the outlook for Brazil’s sovereign rating from ‘Negative’ to ‘Stable’, in a vote of confidence that the winner of this year’s elections will deliver an unpopular agenda of cuts to government spending. Moody’s analysts said faster-than- expected economic growth was also likely to support austerity efforts, which have failed to bring the government’s debt metrics to levels consistent with similar-rated peers. Moody’s kept Brazil’s rating at ‘Ba2’, two notches below investment- grade status. Faster-than-expected fiscal changes could spur an upgrade, while a re-emergence of political dysfunction or stalled reform momentum may trigger a downgrade, Moody’s stated. (Reuters) Regional MENA merger deals 20% down in 1Q2018 – Mergers and acquisitions across the MENA region declined by 20% in 1Q2018, largely driven by factors such as geopolitics and volatile public policies, according to industry experts. Experts said improving business confidence is yet to reflect in M&A deal flows. Transaction Advisory Leader at EY MENA, Phil Gandier said, “Business confidence is improving in the region. Improvement in economic sentiment should reflect in the deal flows during the rest of the year, despite the subdued start.” (GulfBase.com) MENA’s Fintech to attract $2.5bn in deals by 2022 – The current MENA’s fintech market is estimated at $2bn and expected to witness an annual growth of $125mn until 2022, according to MENA Research Partners (MRP). Increasingly compelling business models of Fintech are expected to drive the market growth further. Going forward, MENA is anticipated to experience a new era of fast growth. Fintech funding has been rapidly gaining traction in the past five years, reflecting investors’ rising interest in the Fintech opportunity in MENA. This has supported the proliferation of new Fintech startups, with six startups founded in 2005; the figure is expected to reach 252 by 2020. (GulfBase.com) EU-Gulf trade exceeds $175bn – Two-way trade between the GCC countries and the European Union (EU) exceeded $175.5bn in recent times, according to sources. This makes the EU as the largest trading partner of the GCC, when counted as a single economy. Ewa Synowiec, Chief Advisor to the European Commission and the General Directorate of Trade, said foreign investment in the European Union amounts to 36% of GDP annually compared to 46% abroad. “EU-GCC trade has been steadily growing between 2007 and 2017; total trade increased by 54% in ten years. The EU remains the number one trading partner for the GCC,” Synowiec said. (GulfBase.com) Takaful industry sees strong growth prospects across new markets – The global Islamic insurance (Takaful) industry has strong growth prospects across relatively new markets in Africa and South-East Asia, with significant Muslim populations, as well as core markets such as the GCC, Malaysia and Turkey, according to analysts. In terms of global market share, the GCC region dominates the global Takaful industry, representing 77.2% of the world’s Takaful gross written premiums (GWP) in 2015, according to a recent report by Aplen Capital. At an estimated $11.5bn, the region’s Takaful market has grown at CAGR of 18% from 2012, and accounts for nearly 44% of the GCC insurance sector. Preference towards Shari’ah- compliant financial solutions and an expanding non-life market are the factors aiding growth. (GulfBase.com) SABIC eyes 70% output boost by 2025 and operational base in Houston – Saudi Basic Industries Corporation (SABIC) is planning to boost its production capacity 70% by 2025 as the Middle East’s dominant chemical maker works with new joint- venture partners and expands its footprint in the heart of the US shale boom. Increasing chemical production is crucial to Saudi Arabia’s Vision 2030 blueprint, which envisions creating higher-value products and jobs, SABIC’s CEO, Yousef Al Benyan said. (GulfBase.com) CMA approves the capital increase request for Saudi Automotive Services Company – Capital Market Authority (CMA) issued its resolution approving Saudi Automotive Services Company’s request to increase its capital from SR540mn to SR600mn through issuing one bonus share for every nine existing shares owned by the shareholders, increasing the company’s outstanding shares from 54mn shares to 60mn shares. (Tadawul) UAE’s total trade with EU hits 52.6bn Euros – Total trade in goods between the UAE and the European Union (EU) amounted to 52.6bn Euros. The most important goods in EU exports were machinery and transport equipment (more than half), manufactured goods and chemicals. The largest share in imports from the UAE to the EU market have mineral fuels,

- 5. Page 5 of 6 lubricants and other related materials, as well as manufactured goods. The EU-UAE trade in services amounts to almost 15bn Euros. (GulfBase.com) Dubai’s non-oil sector sees solid growth in March – Dubai’s non- oil private sector witnessed a significant improvement in business conditions during March, with sharp growth in both output and new work contributing to the latest expansion, according to Emirates NBD Dubai Economy Tracker. That said, employment slipped into contraction for the first time since February last year. The seasonally adjusted Emirates NBD Dubai Economy Tracker Index was at 55.3, down from 55.8 in February. Scoring well above the neutral 50.0 threshold, the figure indicated a marked expansion that was in line with the historical average, albeit the lowest for three months. Growth was recorded across all three monitored sub-sectors in March, led by travel & tourism (56.7), followed by wholesale & retail (56.3) and construction (53.2). (GulfBase.com) Dubai’s residential property rents down 5% in 1Q2018– Residential property prices across Dubai registered a 12-month decline of 2% on average while rents were down by up to 5% in some key areas of the Emirate, noted a report by leading property consultants Cavendish Maxwell. During 1Q2018, residential property rents declined at a more pronounced rate than sales prices, resulting in yield compression in most communities, stated the report. The pressure on housing allowances has also impacted rental market performance and the pool of tenants at the higher end of the spectrum continues to shrink, it added. (GulfBase.com) Amanat Holdings seeks new opportunities beyond GCC – Amanat Holdings is aiming for investment opportunity in health care and education sectors outside GCC markets. Amanat Holdings stated that the company’s refreshed investment strategy is built on investing in healthcare and education sectors, complementary geographic markets, active investing style. (Reuters) ADNOC Distribution approves AED735mn dividend payment – Shareholders of ADNOC Distribution approved AED735mn (5.88 Fils per share) dividend payment, at the company’s first annual general meeting (AGM). The dividend was approved following a report of the company’s performance, which highlighted the significant achievements the company made in 2017. (GulfBase.com) National Bank of Kuwait's net profit rises to KD93.6mn in 1Q2018 – National Bank of Kuwait recorded net profit of KD93.6mn in 1Q2018 as compared to KD85.4mn in 1Q2017. Net operating profit came in at KD148.9mn as compared to KD133.9mn in 1Q2017. Total operating revenue came in at KD213.4mn as compared to KD195.4mn in 1Q2017. Total assets stood at KD26.78bn at the end of March 31, 2018 as compared to KD24.85bn at the end of March 31, 2017. EPS came in at KD0.015 in 1Q2018 as compared to KD0.014 in 1Q2017. (Boursa Kuwait) Saudi Arabia’s VAT experience has valuable insights for Oman – Saudi Arabia’s experience in implementing value added tax (VAT) should provide instructive insights on how Omani authorities and businesses should get their act together and avoid some of the pitfalls faced by their Saudi Arabian counterparts, a key expert pointed out. The Sultanate is expected to introduce VAT at the start of 2019. A report of Saudi Arabia’s experience over the first 60 days of VAT implementation has important takeaways for Oman as the Sultanate’s gears up to embrace this new levy in less than nine months. Published by multinational professional services EY, it collates the responses of around 500 business leaders who participated in a survey on VAT conducted by the company in the Kingdom. (GulfBase.com)

- 6. Contacts Saugata Sarkar, CFA, CAIA Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa Mohamed Abo Daff QNB Financial Services Co. W.L.L. Senior Research Analyst Contact Center: (+974) 4476 6666 Tel: (+974) 4476 6589 PO Box 24025 mohd.abodaff@qnbfs.com.qa Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. W.L.L. (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (Q.P.S.C.). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange. Qatar National Bank (Q.P.S.C.) is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 6 of 6 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns) 60.0 80.0 100.0 120.0 140.0 160.0 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 QSE Index S&P Pan Arab S&P GCC 0.1% 1.8% (0.4%) 0.2% 0.1% 1.4% 0.4% (0.5%) 0.0% 0.5% 1.0% 1.5% 2.0% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,336.35 0.2 0.2 2.6 MSCI World Index 2,061.19 0.4 0.4 (2.0) Silver/Ounce 16.49 0.6 0.6 (2.6) DJ Industrial 23,979.10 0.2 0.2 (3.0) Crude Oil (Brent)/Barrel (FM Future) 68.65 2.3 2.3 2.7 S&P 500 2,613.16 0.3 0.3 (2.3) Crude Oil (WTI)/Barrel (FM Future) 63.42 2.2 2.2 5.0 NASDAQ 100 6,950.34 0.5 0.5 0.7 Natural Gas (Henry Hub)/MMBtu 2.78 1.8 1.8 (21.5) STOXX 600 375.30 0.5 0.5 (1.2) LPG Propane (Arab Gulf)/Ton 76.00 2.0 2.0 (23.2) DAX 12,261.75 0.5 0.5 (2.7) LPG Butane (Arab Gulf)/Ton 78.25 2.3 2.3 (27.9) FTSE 100 7,194.75 0.5 0.5 (2.2) Euro 1.23 0.3 0.3 2.6 CAC 40 5,263.39 0.4 0.4 1.5 Yen 106.77 (0.1) (0.1) (5.3) Nikkei 21,678.26 0.7 0.7 0.2 GBP 1.41 0.3 0.3 4.6 MSCI EM 1,163.07 0.1 0.1 0.4 CHF 1.05 0.3 0.3 1.9 SHANGHAI SE Composite 3,138.29 0.2 0.2 (2.2) AUD 0.77 0.2 0.2 (1.4) HANG SENG 30,229.58 1.3 1.3 0.6 USD Index 89.84 (0.3) (0.3) (2.5) BSE SENSEX 33,788.54 0.6 0.6 (2.3) RUB 60.65 4.3 4.3 5.3 Bovespa 83,307.23 (3.0) (3.0) 5.8 BRL 0.29 (1.5) (1.5) (3.2) RTS 1,094.98 (11.4) (11.4) (5.1) 85.7 84.9 75.9