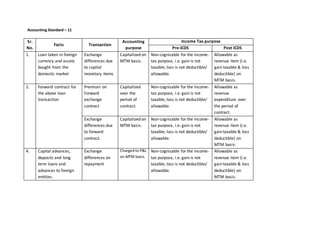

1. Accounting Standard – 11

Sr.

No.

Facts Transaction

Accounting

purpose

Income Tax purpose

Pre-ICDS Post ICDS

1. Loan taken in foreign

currency and assets

bought from the

domestic market

Exchange

differences due

to capital

monetary items

Capitalized on

MTM basis.

Non-cognizable for the income-

tax purpose, i.e. gain is not

taxable, loss is not deductible/

allowable.

Allowable as

revenue item (i.e.

gain taxable & loss

deductible) on

MTM basis.

2. Forward contract for

the above loan

transaction

Premium on

Forward

exchange

contract

Capitalized

over the

period of

contract.

Non-cognizable for the income-

tax purpose, i.e. gain is not

taxable, loss is not deductible/

allowable.

Allowable as

revenue

expenditure over

the period of

contract.

Exchange

differences due

to forward

contract.

Capitalized on

MTM basis.

Non-cognizable for the income-

tax purpose, i.e. gain is not

taxable, loss is not deductible/

allowable.

Allowable as

revenue item (i.e.

gain taxable & loss

deductible) on

MTM basis.

4. Capital advances,

deposits and long

term loans and

advances to foreign

entities.

Exchange

differences on

repayment

Chargedto P&L

on MTM basis.

Non-cognizable for the income-

tax purpose, i.e. gain is not

taxable, loss is not deductible/

allowable.

Allowable as

revenue item (i.e.

gain taxable & loss

deductible) on

MTM basis.